Troubleshooting ecoPayz Casino Deposit Errors in the UK

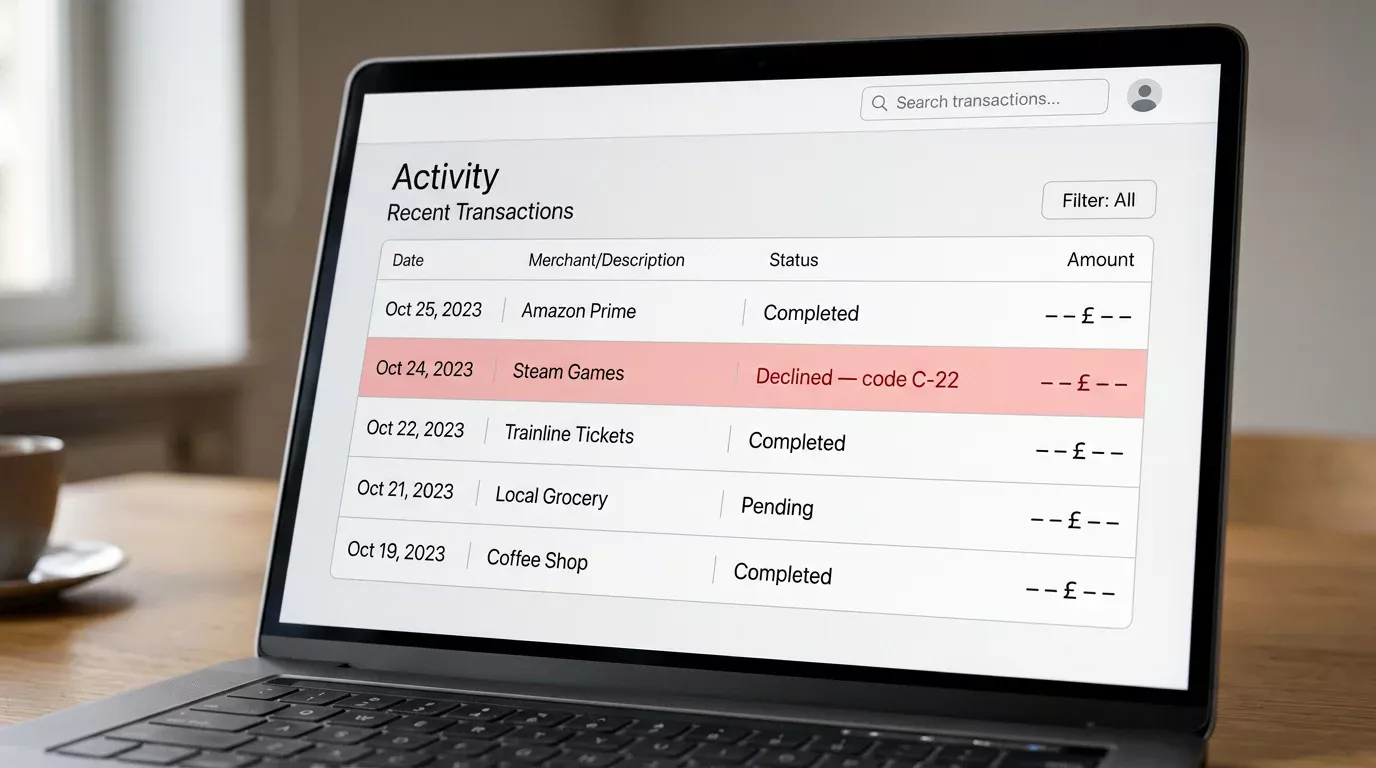

A declined Payz deposit at a UK casino has the same disorienting quality as a card decline at a supermarket till. The transaction looks fine, the balance is there, you clicked the right buttons, and yet the cashier returns a generic error that gives you no useful information about what went wrong. The cashier’s error message is almost never the actual reason — it is a sanitised string covering one of perhaps a dozen distinct failure modes, each with its own remedy.

I have been categorising these failures by underlying cause for years, and the pattern is consistent. About a third of declines originate on the Payz side, about half on the casino side, and the rest in the handshake between the two. The good news is that the cause can usually be diagnosed from a few details visible to the player; the bad news is that the cashier is rarely helpful in surfacing them. Let me walk through the decline categories and the decision tree I use.

Five Predominant Error Classifications for Payz Transactions

Category one: insufficient funds in the wallet. Trivial in principle, common in practice. You deposit £50 at a casino, your wallet shows £50, the transaction declines. The cause is usually that the wallet balance includes some amount reserved against another pending transaction — an eco-Virtualcard generation, a pending withdrawal that has not yet finalised, or a hold from a different merchant. The headline balance and the available balance are not always the same number. Check the wallet’s transaction history for any “pending” line items before re-attempting.

Category two: per-transaction caps. Your tier sets a per-transaction limit that the deposit exceeds. Classic tier users hit this most often, particularly on weekend high-stakes attempts. The cashier sees the decline come back from PSI-Pay but does not surface the cap as the reason. Diagnostic: try the same merchant with a substantially smaller deposit. If the smaller amount clears, the cap is the cause.

Category three: funding source restrictions. If the wallet’s balance traces to a credit card top-up — even partially — the casino transaction may be declined on credit-source grounds under the 2020 UK credit card gambling ban. The structural background here is important: before the ban, 5.7% of UK online gambling deposits ran on credit cards, with 22% of credit-funded gamblers classified as problem gamblers, and the regulator closed that channel deliberately. Diagnostic: review your recent wallet top-up history. Any credit card line item in the funding chain is a candidate cause.

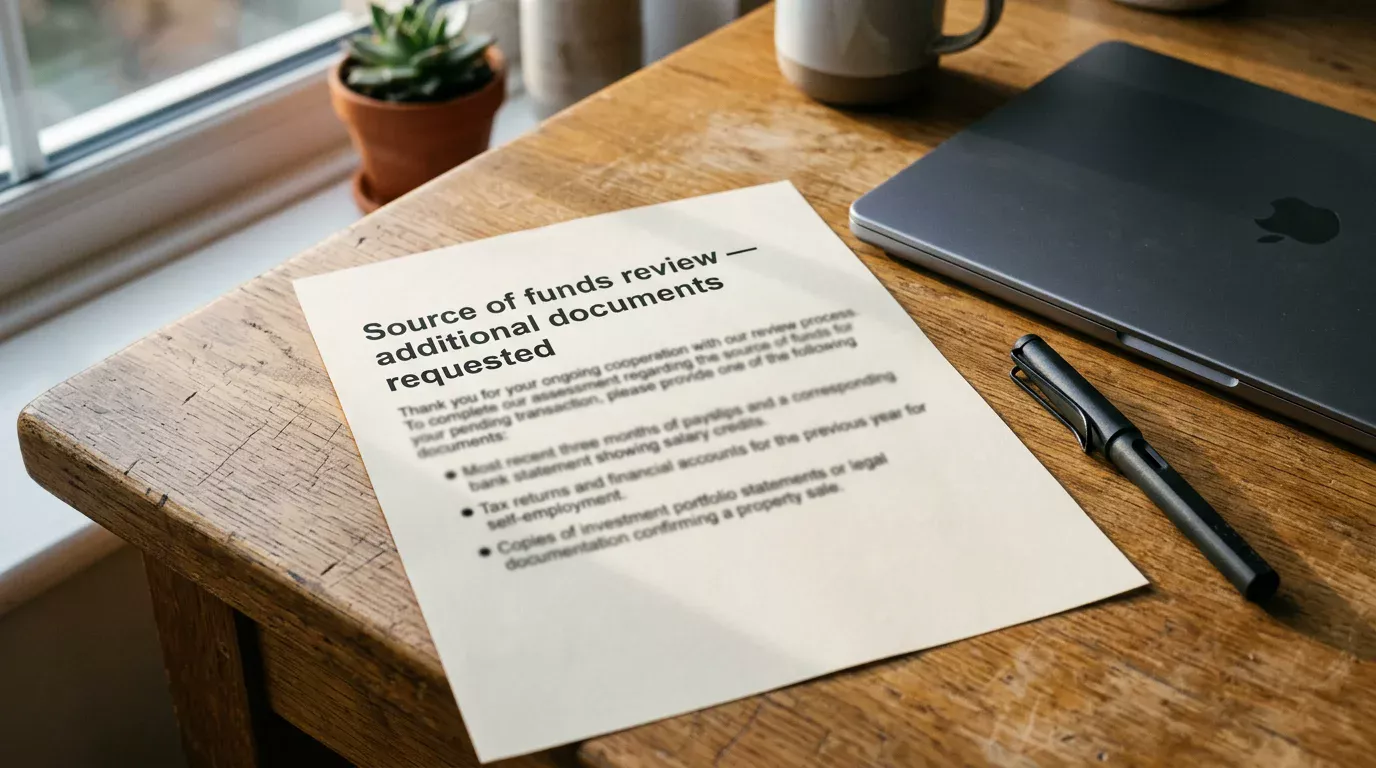

Category four: KYC or verification gates. The casino is waiting for an identity document, a proof of address, or a source-of-funds declaration before allowing further deposits. The decline is the operator’s way of flagging that further action is needed. Diagnostic: check your casino account for any pending verification requests. UK operators are obligated to surface these, but the messages sometimes land in account notifications rather than at the cashier.

Category five: risk-engine flags on the operator side. The deposit hit a pattern the operator’s risk engine considers suspicious — too rapid succession of deposits, deposit from an unfamiliar geography, deposit shortly after registration on an unverified account, or a deposit pattern consistent with affordability concerns. Diagnostic: time. Wait an hour, contact support, and provide whatever additional context the operator requests. Re-attempting immediately rarely clears a risk-engine decline.

AML and Affordability Declines, in More Detail

The affordability and AML category deserves more space because it is the one where players misinterpret what is happening. The £150 financial vulnerability threshold that came into force on 28 February 2025 triggers public-data affordability checks at most UK casinos. Operators report that 97% of these checks complete frictionlessly — they run in the background, return a “no concern” signal, and the player never knows. The remaining 3% surface as enhanced due diligence requests, and a small fraction of those result in declined transactions.

The decline in this category is not punitive. It is the operator pausing the transaction while it gathers enough information to satisfy its licence condition. The fastest way through is to respond to the operator’s information request promptly and accurately. Providing payslips, bank statements, or other source-of-funds documentation usually resolves the issue within a few days; refusing or delaying the response extends it indefinitely.

Two patterns I see consistently in this category. The first is the “burst” deposit pattern — several substantial deposits within a short period, often after a paycheck or after a previous loss. The risk engine flags this as a potential affordability concern, even when the player can comfortably afford the spend. Spreading deposits more evenly across a month avoids the pattern.

The second is the cross-operator pattern. UK operators share certain risk signals through industry-level mechanisms, and a player flagged at one operator may face escalated checks at others. This is rare but worth knowing — declines that “appear out of nowhere” at a new casino can sometimes trace to historical patterns at a previous operator.

One regulatory note. The frictionless rate is rising as the data infrastructure improves, and the policy direction is toward making affordability checks invisible to the vast majority of players. Most checks are routine. If yours becomes non-routine, the request for information is part of the operator’s compliance obligation, not a sign of personal scrutiny.

Telling Payz-Side Declines From Casino-Side Declines

This is the single most useful diagnostic skill. Each side leaves different fingerprints, and recognising them speeds resolution dramatically.

Payz-side decline indicators. The wallet’s transaction history shows the attempted transaction with a “declined” status, and the failure timestamp is essentially identical to your cashier-side attempt timestamp. The amount appears in your wallet’s pending transactions briefly before being released. The error message in the cashier is short and generic — often “transaction declined” with no additional code. Calling Payz support gives you an answer; calling the casino does not.

Casino-side decline indicators. Your wallet shows no record of the transaction at all, or shows a successful debit followed by an immediate refund. The cashier’s error message is more specific, sometimes including an error code or a pointer to a verification step. Your casino account profile may show a notification or a flagged status. Calling the casino gives you an answer; calling Payz does not.

Handshake declines are rarer and harder to diagnose. The wallet completes the transaction successfully, the casino’s records show the deposit as failed, and neither side acknowledges the other side’s view. These cases usually trace to a timeout in the communication between the cashier and PSI-Pay’s API, and the money is in transit but not yet attributed. Wait 24 hours before opening a support ticket; most handshake declines self-resolve.

How to Resolve a Payz Casino Decline

The decision tree I run when a reader sends me a screenshot has four steps, in this order.

Step one: confirm the wallet balance is sufficient and unreserved. Open the Payz app, check the available balance not just the total balance. Resolve any unintended holds before retrying.

Step two: try a substantially smaller deposit. £10 instead of £100. If the £10 clears, the cause was tier caps, risk-engine flags on the larger amount, or affordability scrutiny. If the £10 also declines, the cause is structural and a smaller amount will not fix it.

Step three: check both accounts for verification requests. Log into the casino, check notifications. Log into Payz, check the account messages. Pending verification is the single most common cause of “out of nowhere” declines and the one with the cleanest remedy.

Step four: contact support — the right side. If your wallet history shows a declined transaction, contact Payz. If your wallet history shows no transaction, contact the casino. Provide the timestamp, the amount, and any error codes you saw. Avoid demanding immediate refunds in the opening message; the support agent’s first job is to identify what happened, and you accelerate that by giving them clean information.

One scenario worth flagging. A declined transaction is not always recoverable as winnings if the underlying issue is structural — for example, a credit-funding chain that traces back several months. In those cases, the path is usually to clean the funding chain rather than to dispute the decline. If you find yourself disputing decline after decline at the same operator, the issue is not the decline; it is something upstream in your account profile. For the broader picture on disputes and the limited chargeback options that an e-wallet offers, my walk-through of ecoPayz casino disputes covers the realistic dispute routes.

The slow path through resolution is usually the only path. The cashier rarely accepts an angry follow-up call as a substitute for the documentation it has requested. Submit what is asked, wait the stated turnaround, and the issue usually resolves within a few business days. Players who escalate before providing requested information typically wait longer, not shorter.

Prepared by the Paylobby editorial staff.