Wallet Comparison: ecoPayz vs Skrill, Neteller, PayPal

The honest version of the “which e-wallet is best for UK casinos” question is that there is no single winner — and the people most insistent that there is one are usually selling something. After nine years of watching UK cashiers tilt between Payz, Skrill, Neteller and PayPal, I can tell you that each rail has a specific shape that fits a specific player profile, and the gap between them is narrower than the marketing wants you to believe.

What has actually changed in 2026 is the surrounding environment, not the rails themselves. UK digital wallet spending is on a trajectory from £269 billion in 2025 to a projected £453 billion by 2030, a 68% rise that is reshaping how operators design their cashier. The newer Apple Pay and Google Pay options have eaten into the old e-wallet majority. Operators are juggling more methods than they used to, with proportionally less attention going to any single one. That makes the Payz-versus-the-rest question more interesting, not less.

This comparison cuts across seven angles: who actually owns each rail and what licences they hold, how widely each one is accepted at UKGC-licensed casinos, the fee structures side by side, the speed and limit profile, the bonus-eligibility patterns, the safety track record, and where Trustly, Apple Pay and Paysafecard fit when they appear alongside the e-wallet big four. I will name the rails directly but I will not name specific operators — operator-by-operator coverage is what comparison tables get wrong.

When evaluating modern payment methods, comparing ecoPayz vs Trustly Pay N Play reveals significant differences in how open banking and e-wallets handle your data.

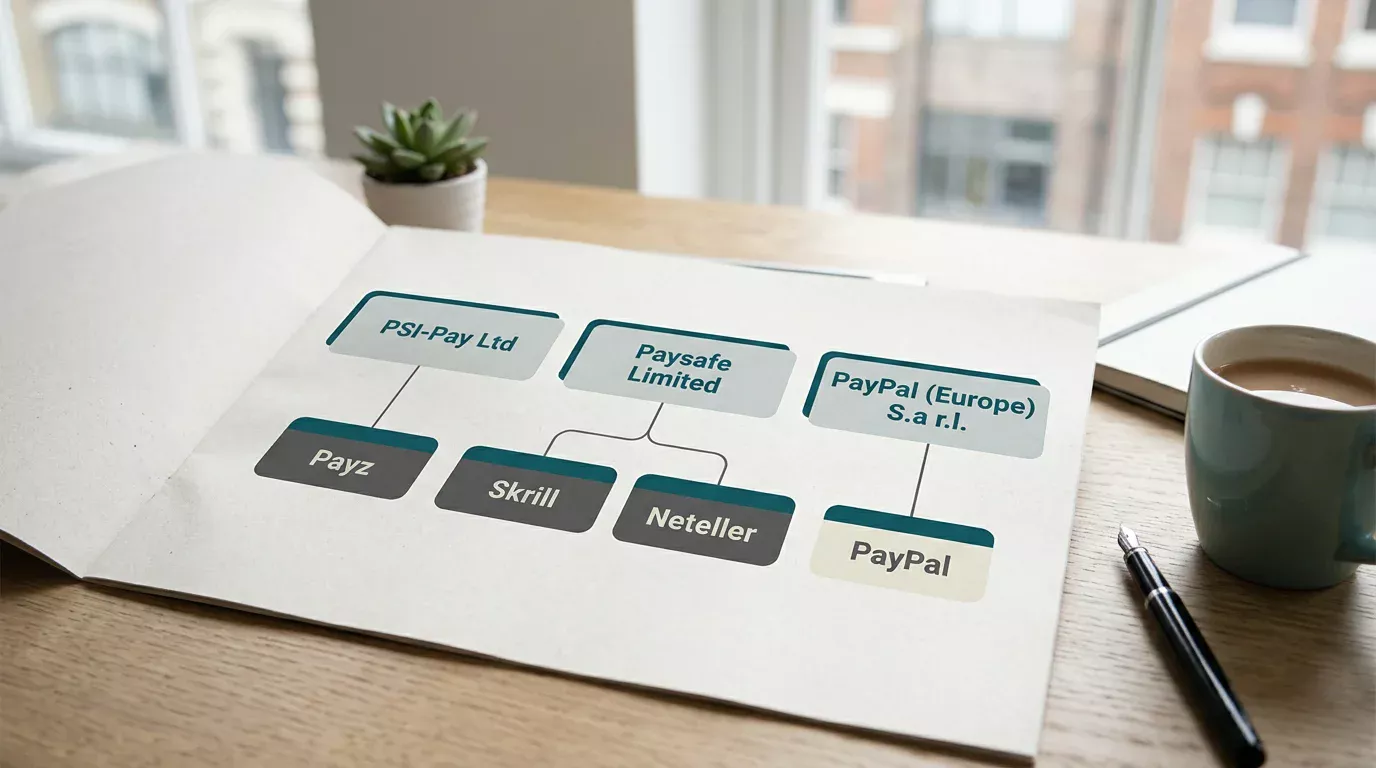

PSI-Pay, Paysafe, and PayPal Ownership Structures

Half the confusion about these four e-wallets comes from the fact that nobody at a casino cashier ever tells you what corporate entity is actually moving your money. The brand on the logo and the legal entity behind it diverge in three of the four cases.

Payz is run by PSI-Pay Ltd, an FCA-authorised UK electronic money institution that has held its licence for over fifteen years and operates across 174 countries. PSI-Pay is dual-regulated — the FCA at home and the Central Bank of Cyprus for the wider European footprint — and the regulatory architecture is what makes Payz a genuine alternative to debit cards rather than a fintech overlay. The May 2023 rebrand from ecoPayz to Payz was cosmetic; the underlying entity, the licence number, and the operating stack did not change.

Skrill and Neteller are both owned by Paysafe Limited, a US-listed payments group. In the UK, the regulated operating entity is Skrill Limited, registered with the FCA under reference 900001 — one of the longest-held e-money licences in the country. Neteller is essentially Skrill’s sibling brand on the same regulatory and technical stack, marketed to a different segment. The shared parentage means a UK player using both wallets is effectively trusting one corporate group with two relationships, which has implications I will come back to under safety.

PayPal in the UK is run by PayPal (Europe) S.à r.l. et Cie SCA, the Luxembourg-incorporated group entity, with FCA permission for its UK operations. PayPal is structurally different from the other three — it is a payments platform that happens to support some gambling merchants, not a specialist e-wallet built around the iGaming ecosystem. UK casino acceptance of PayPal exists, but it is patchier, more restrictive, and more conditional on the operator’s own arrangement with PayPal Europe.

Which Is Most Widely Accepted at UKGC Casinos in 2026

Cashier coverage in 2026 is shifting fast enough that any snapshot is dated within months, but the rough hierarchy is stable. Skrill is the most widely accepted of the four at UKGC-licensed casinos, with the broadest operator footprint and the highest probability of appearing on a typical UK cashier. Neteller comes second, partly because operators who carry one Paysafe brand usually carry the other. Payz sits third, with respectable but narrower coverage. PayPal is fourth and the only one of the four where you genuinely cannot assume the cashier will offer it.

The underlying market data is consistent with this hierarchy. Around 60% of UK online casino players still default to debit cards, with e-wallets making up a growing but smaller share. Inside that growing share, Apple Pay and Google Pay deposits at UK casinos have grown around 47% year on year, and Apple Pay alone is now supported at roughly 30% of UK online casinos. The newer mobile-native rails are eating into territory that was historically e-wallet ground, which means the coverage gap between Skrill and Payz matters less than it did three years ago — both are losing relative share to the mobile wallets.

What matters more for a player choosing between the four is which one is offered at the specific casinos you actually use. Payz coverage tends to be deeper at brands targeting international and high-roller traffic, where its multi-currency strength is a real advantage. Skrill coverage is broadest at mass-market UK brands. Neteller often appears where Skrill does, with similar terms. PayPal coverage is concentrated at a handful of large, established UK operators — outside that core group, you should expect not to find it.

The practical takeaway: do not pick a wallet on theoretical coverage. Pick it on coverage at the specific casino you plan to use, and confirm by checking the cashier methods list before opening an account.

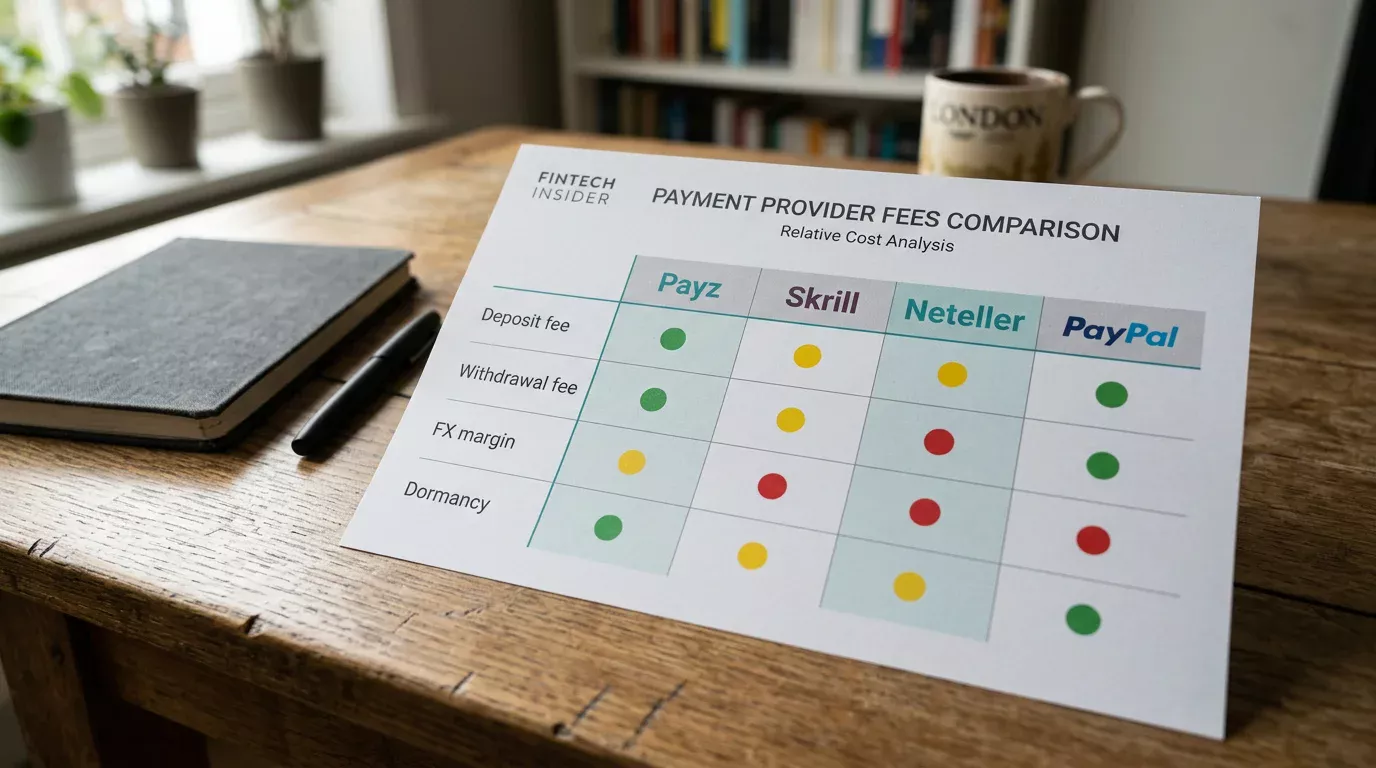

Deposit, Withdrawal and FX Fees: A Side-By-Side Reading

Fee structures across the four wallets are different enough that a player who picks the wrong one for their pattern can leak a meaningful percentage of their bankroll to friction. The headline charges are usually visible, but the secondary ones are where the rails diverge.

For inbound merchant payments — the casino crediting your wallet at withdrawal, or you funding the wallet from an external source — all four wallets are nominally low or zero fee on the e-money leg in GBP. The friction lives elsewhere. Payz applies a 2.99% currency conversion margin over the mid-market rate whenever your transaction crosses a currency, which at a GBP-denominated UK casino is rare for the deposit itself but common if you ever route money through a euro-balance intermediate step. Skrill and Neteller’s conversion margin is structurally similar — they sit in the same Paysafe family with comparable FX layering — and the practical cost on a typical cross-currency transaction is broadly equivalent. PayPal’s conversion margin is generally higher than the specialist e-wallets, often 3.5% or more depending on the corridor, which makes PayPal the most expensive of the four on any non-GBP route.

For outbound transfers from the wallet to a bank account or card, all four charge — but the structures differ. Payz tier-based outbound fees scale from a few pounds for Classic-tier users to lower or waived fees at Gold and above. Skrill and Neteller publish fixed-percentage withdrawal fees on certain destinations, with rate variation across rails. PayPal’s outbound fees to UK debit cards are well-documented as a fixed percentage on the transferred amount, though within the UK the standard bank-transfer route is typically free.

The Skrill business mix tells you a lot about where the e-wallet sector actually makes its money. Skrill’s 2025 revenue of $2.1 billion was up 16% year on year, with 67% of that revenue coming from transaction fees rather than wallet float or merchant subscriptions. That fee dependency is the same shape across Paysafe-family wallets, and Payz’s underlying economics are not radically different. UK corporate customers make up around 25.32% of Skrill’s business clients, which gives you a sense of how UK-centric the broader Paysafe footprint is — and why their UK casino acceptance is the broadest.

The reading I would give a UK player on fees: for GBP-only play at a GBP-denominated cashier, the four wallets are largely equivalent on deposit. On withdrawal, Payz Gold-tier and above is the cheapest specialist option. On any cross-currency play, Payz and Skrill are roughly tied, both cheaper than PayPal. On exotic destination payouts, check the published rate card before assuming.

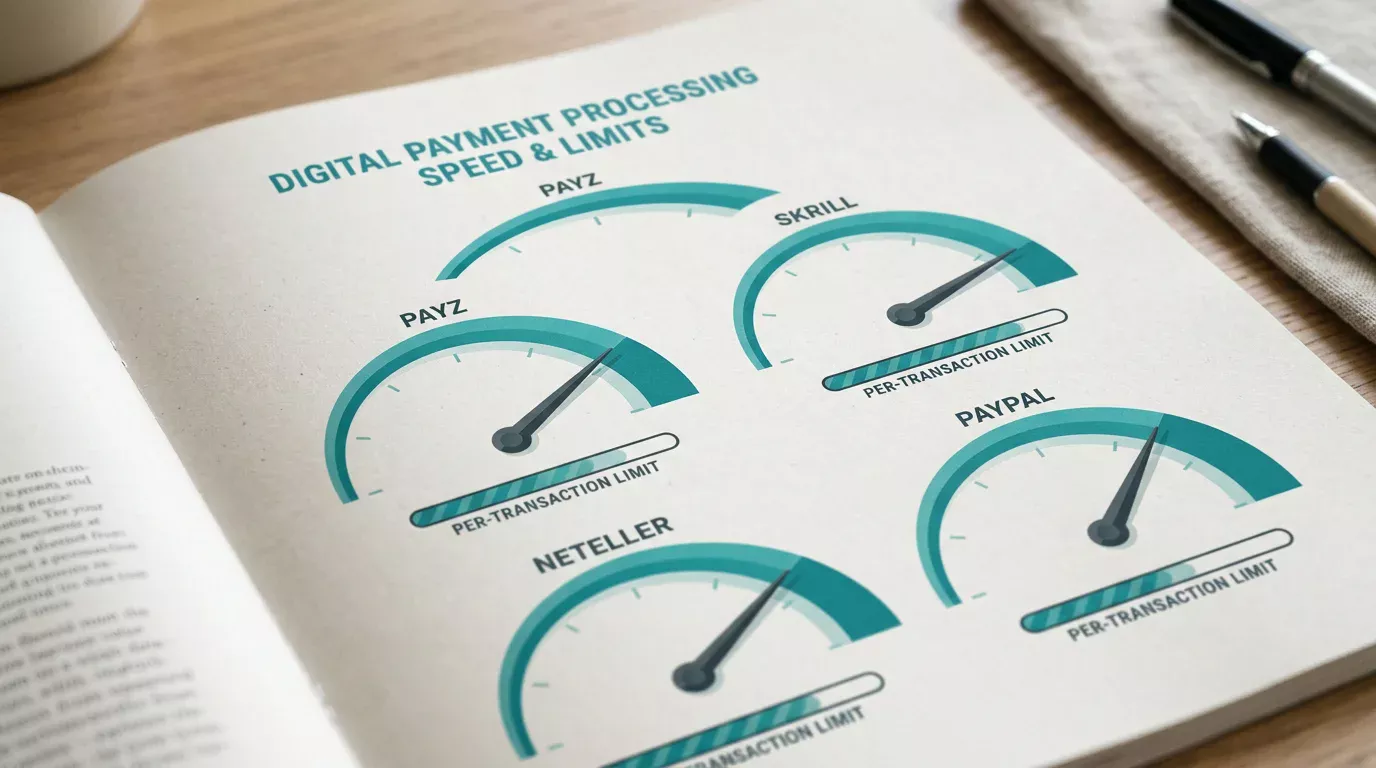

Speed and Limits: Where Payz Lags and Where It Wins

All four wallets are fast on the deposit leg. The handshake is API-level e-money, the funds move between regulated entities, and on a clean transaction every one of them will credit your casino balance in under ten seconds. Speed on deposit is not where these rails diverge.

Withdrawal speed is where the differences emerge, and they are mostly structural rather than technical. Skrill has a published UK casino deposit ceiling of up to £20,000 per transaction and withdrawal ceilings up to £10,000, with Neteller offering broadly similar headroom. These are upper bounds, not typical operator limits, but they tell you the Paysafe-family wallets are built to handle high-value transactions without architectural friction. Payz’s per-transaction casino caps tend to sit lower in practice, with the binding constraint being your tier ceiling rather than the operator’s. PayPal’s casino limits are usually capped tighter than the others, partly because PayPal Europe is more conservative about gambling exposure on its platform.

On time-to-funds-cleared in the wallet, the four are similar on healthy transactions and diverge on flagged ones. Skrill and Neteller’s compliance team operates inside the same Paysafe risk framework, which means flagged withdrawals to those wallets follow predictable timelines. Payz’s PSI-Pay handles flagged reviews independently, often slightly faster on mid-range amounts and slightly slower on very large ones where additional source-of-funds work is needed. PayPal’s flagged-review timelines are the most variable of the four because PayPal is the least specialised in iGaming and so its risk model is less tuned to casino-specific patterns.

For a player profile reading: high-roller play favours Skrill or Neteller on raw limits; mid-range play with regular cross-currency activity favours Payz; small-stake play with maximum brand recognition still favours PayPal at the handful of operators that carry it, despite the fee disadvantage.

Which E-Wallets Trigger Bonus Exclusions More Often

Anyone who has tried to claim a welcome offer at a UK casino while paying through an e-wallet has hit the same wall — the small print that excludes e-wallet deposits from the bonus. The exclusion is not arbitrary, and it applies unevenly across the four rails.

The exclusion logic is straightforward from the operator’s side. E-wallet deposits historically correlated with higher rates of bonus abuse — players moving money through multiple accounts, multiple wallets, and multiple operator brands to maximise welcome offers. Operators responded by carving e-wallet deposits out of bonus eligibility, particularly the larger first-deposit offers. Skrill and Neteller are the most commonly excluded of the four, because they have the longest history with the iGaming sector and so the longest history of being identified as a vehicle for abuse. PayPal is excluded slightly less often, because PayPal users are a less fluid population — fewer multi-accounters, more mainstream players.

Payz sits in a curious middle position. It is excluded from welcome bonuses at a meaningful share of UK casinos — though slightly less consistently than Skrill or Neteller, because some operators put the Paysafe-family wallets on a stricter list than the rest. On no-deposit and registration-trigger bonuses, Payz is generally treated the same as other methods, since those bonuses do not require a funding event.

The pragmatic implication: if a welcome offer is a meaningful part of your decision to deposit at a casino, check the bonus terms before choosing the rail, not after. The exclusion is almost always written in the bonus T&Cs in unambiguous language; the cashier will not warn you at deposit time.

Safety Track Record: Regulators, Breaches and Chargebacks

“Safety” at this level is not a single metric. It is a layered question: who regulates the entity, whether your balance is protected if the entity fails, what happens when a transaction is disputed, and whether the broader payments environment is being eroded by unregulated competitors.

On regulation, all four wallets are authorised under their respective FCA permissions for UK operations. PSI-Pay for Payz, Skrill Limited for Skrill, the same group for Neteller, and PayPal Europe S.à r.l. for PayPal. The FCA framework is the same across the board: capital requirements, safeguarding of customer funds in segregated accounts, anti-money-laundering obligations. No single one of these wallets is “more authorised” than the others.

On segregation of funds — what happens to your balance if the wallet operator fails — the picture is also uniform. All four hold UK customer funds in segregated accounts under FCA safeguarding rules. None of them are covered by the Financial Services Compensation Scheme in the same way bank deposits are; this is a structural difference between e-money institutions and banks, not specific to any one wallet.

On chargebacks, e-wallets occupy an awkward space. None of the four offer a true Visa or Mastercard scheme-rule chargeback in the way a debit card transaction would, because the wallet sits between the player and the operator and is not the underlying payment instrument. What you get instead is wallet-side dispute handling, which is materially weaker in your favour than card chargebacks but stronger than nothing.

The broader environmental risk is the one that concerns me most in 2026. The Gaming Compliance International data put global unregulated online gambling wagering at $5.9 trillion in 2025, with regulated operators making up only 22% of global online gross gaming revenue. Matt Holt, the GCI chief executive, framed the scale plainly — at $5.9 trillion in wagering value, unregulated online gambling is one of the largest economic systems in the world, and regulators are not facing a marginal challenge but a dominant one. Any of these wallets, used outside UKGC-licensed estates, loses the protection layer the regulator provides. The wallet is safe — but the cashier you fund with it has to be safe too.

Beyond the Big Three: Where Trustly, Apple Pay and Paysafecard Fit

Anyone comparing only Payz, Skrill, Neteller and PayPal in 2026 is fighting yesterday’s war. The three rails that have grown into the picture meaningfully — Trustly, Apple Pay and Paysafecard — sit alongside the classic e-wallets at most cashiers and serve different player needs.

Apple Pay and Google Pay are tokenisation layers over debit and credit cards rather than wallets in their own right. The token replaces the card number at the cashier, but the underlying card remains the funding instrument, including its own banking-level protections. Apple Pay’s UK casino footprint reached around 30% of operators by 2025, with year-on-year growth of around 47% across the Apple Pay and Google Pay combined volume — fast enough that the e-wallet incumbents are losing share at the margin.

Paysafecard is the odd one out — a prepaid voucher purchased with cash and redeemed online with a 16-digit PIN. No stored online balance, no withdrawal route, no recurring funding. It serves a specific player profile: those who want to play without linking any bank account at all.

Which Wallet for Which Player Profile

Spending nine years inside this category has convinced me that the “best e-wallet” framing is a category error. The four rails are different shapes for different player profiles, and the only sensible way to pick is to match the wallet’s strengths to your own pattern.

Payz is the strongest choice for players whose pattern includes regular cross-currency activity, mid-range deposits and withdrawals, and a preference for a tier-based loyalty model that rewards higher activity with better terms. The 174-country footprint and the FCA-authorised PSI-Pay infrastructure make it a genuine international rail, which matters when your casino lobby occasionally runs in a non-GBP currency.

Ultimately, the choice of wallet depends on which of the leading UK online casinos you prefer to play at regularly.

Skrill and Neteller are the strongest choices for players whose pattern is high-volume, high-limit, mass-market UK casino traffic. The Paysafe-family wallets carry the deepest UKGC operator footprint and the highest published per-transaction ceilings, which makes them the default choice for mid-roller and high-roller play within a single GBP corridor.

PayPal is the strongest choice for the narrow segment of players who already use it for everything else in their financial life, who play primarily at the handful of large UK operators that carry it, and who do not need the multi-currency flexibility of the specialist e-wallets. The brand recognition matters more than the rail mechanics for this profile.

None of the four is a wrong choice in absolute terms. All four is, on the other hand, almost always too many — fragmenting your activity across multiple wallets dilutes your tier benefits and increases administrative friction without adding meaningful protection.

Written by the editors at Paylobby.