Real ecoPayz Casino Fees and UK Limits

If you ask a Payz user how much the wallet costs them at a UK casino, you will get the wrong number. Almost universally. After nine years of decomposing actual transaction logs, I can tell you that what players think they paid is usually two or three pounds less than what they actually paid — because the cost of an e-wallet is spread across five layers, and only one of those layers shows up as a labelled fee at the cashier.

The five layers matter more in 2026 than they did three years ago. UK digital wallet spending is on a trajectory from £269 billion in 2025 to a projected £453 billion by 2030 — a 68% increase that is reshaping the economics of the wallet sector. As volume grows, the price per transaction is under pressure to fall on the visible legs and migrate onto the less visible ones. Payz, like every other e-wallet on the UK iGaming circuit, has been quietly restructuring its fee architecture along those lines.

This breakdown walks through every layer of cost on a Payz casino transaction in 2026 — the five-layer anatomy of the total cost, the deposit-leg fees that Payz charges and the ones the operator absorbs, the withdrawal fees by account tier, the 2.99% currency conversion margin and where it does and does not apply, the dormancy and ancillary charges, the daily and monthly limits at each tier, and the tax-side change that arrives in April 2026 and will reshape how operators price the cashier from the operator side. No promotional framing, no league tables of “cheap” versus “expensive” operators. Just the numbers.

It is crucial to understand how the ecoPayz currency conversion fee applies if your casino account operates in a different currency than your wallet.

Five Transaction Cost Layers for Payz Users

The five layers that make up the true cost of a Payz casino transaction are not all charged to you, and not all of them are visible. Working through them is the only way to understand why the figure at the cashier is rarely the figure that hits your bank balance.

Layer one is the cashier-side fee. The operator may charge a per-deposit or per-withdrawal fee, especially on smaller amounts or on the e-wallet rail specifically. Most UK casinos waive this layer entirely on Payz deposits, and a meaningful minority charge a small fixed fee — typically 1% to 2% — on withdrawals. The fee is set by the operator, varies between brands, and is published in the cashier’s payment-methods page.

The other four layers sit on the Payz side and cover the infrastructure cost of running an FCA-authorised electronic money institution. Maintaining the 256-bit SSL encryption stack, the PCI DSS-compliant payment infrastructure, the 2FA layer and the AML compliance team is not cheap, and the costs filter into the fee structure through several routes rather than as a single line item.

Layer two is the funding fee. Topping up your Payz wallet from a debit card or bank account is generally free, but funding from certain rails — international wire transfers, some prepaid cards, occasional cryptocurrency on-ramps where available — carries a charge of between 1% and 3% on the inbound. The casino does not see this layer, but it has already cost you before you opened the cashier.

Layer three is the withdrawal-leg fee on the Payz side. Moving funds from your Payz wallet back to a bank account, a debit card or another destination carries a fee that scales by tier and by destination type. Classic-tier users pay the most; Gold and above pay less; VIP often pays nothing on standard destinations.

Layer four is currency conversion. Any movement across currencies — depositing in EUR to a GBP casino, withdrawing in GBP from a EUR casino, even holding a multi-currency balance and converting internally — incurs the 2.99% margin over the mid-market rate. This is the layer that quietly costs the most over a long-term play history.

Layer five is dormancy and ancillary charges. An inactive account, a maintenance ID document refresh on a paid tier, an account closure with funds remaining — these all trigger fee events that are documented but rarely mentioned at deposit time. They are small individually, but they add up.

Deposit Fees: What Payz Charges, What the Operator Absorbs

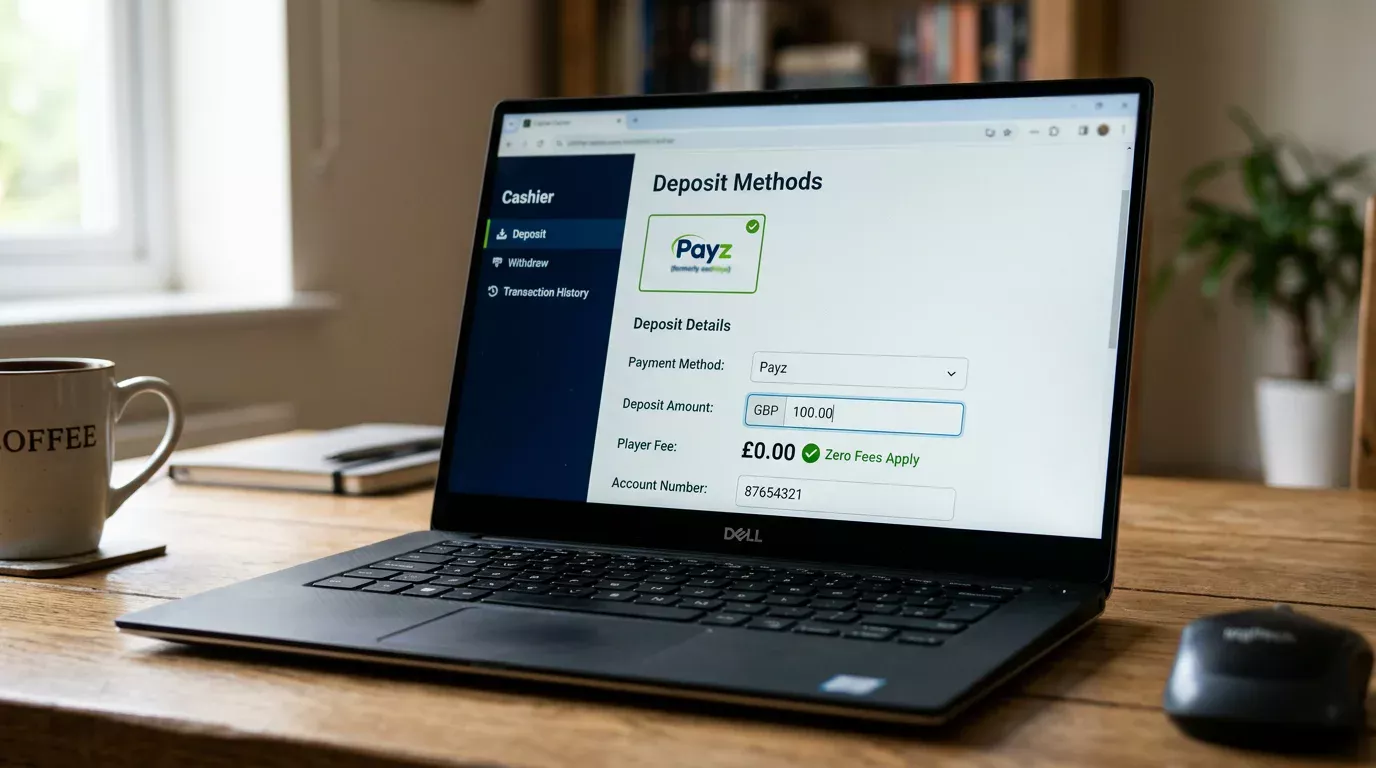

The deposit leg is the cheapest part of a Payz casino transaction in absolute terms, and the part that surprises players the most when they finally read the underlying numbers. Most UK casinos absorb the entire deposit-side cost, which means the player pays nothing visible and Payz still gets paid through a separate channel.

Payz does not charge the player a percentage or fixed fee on standard inbound merchant payments in GBP at UK casinos. The wallet’s revenue from the deposit leg comes from the merchant side — the casino pays Payz a small per-transaction settlement fee, somewhere in the 0.5% to 1.5% range depending on volume and contract terms. The operator builds this into its overall payment-processing cost and either absorbs it or passes it on indirectly through its margin.

The pattern is consistent with how the broader e-wallet sector monetises. Skrill’s 2025 revenue was $2.1 billion, up 16% year on year, and 67% of that revenue came from transaction fees rather than wallet float, advertising or merchant subscriptions. That fee-led model means specialist e-wallets compete hardest for player-side optics — making the visible cost on deposit as close to zero as possible — and recover their economics on the merchant settlement leg and on the withdrawal leg.

The practical implication for any UK player: on a standard GBP-to-GBP Payz deposit at a UKGC-licensed casino, expect zero fee on the player side. If the cashier shows a deposit fee, it is the operator’s charge, not Payz’s. Compare it against other operators’ fee structures before assuming it is normal.

Withdrawal Fees by Payz Account Tier

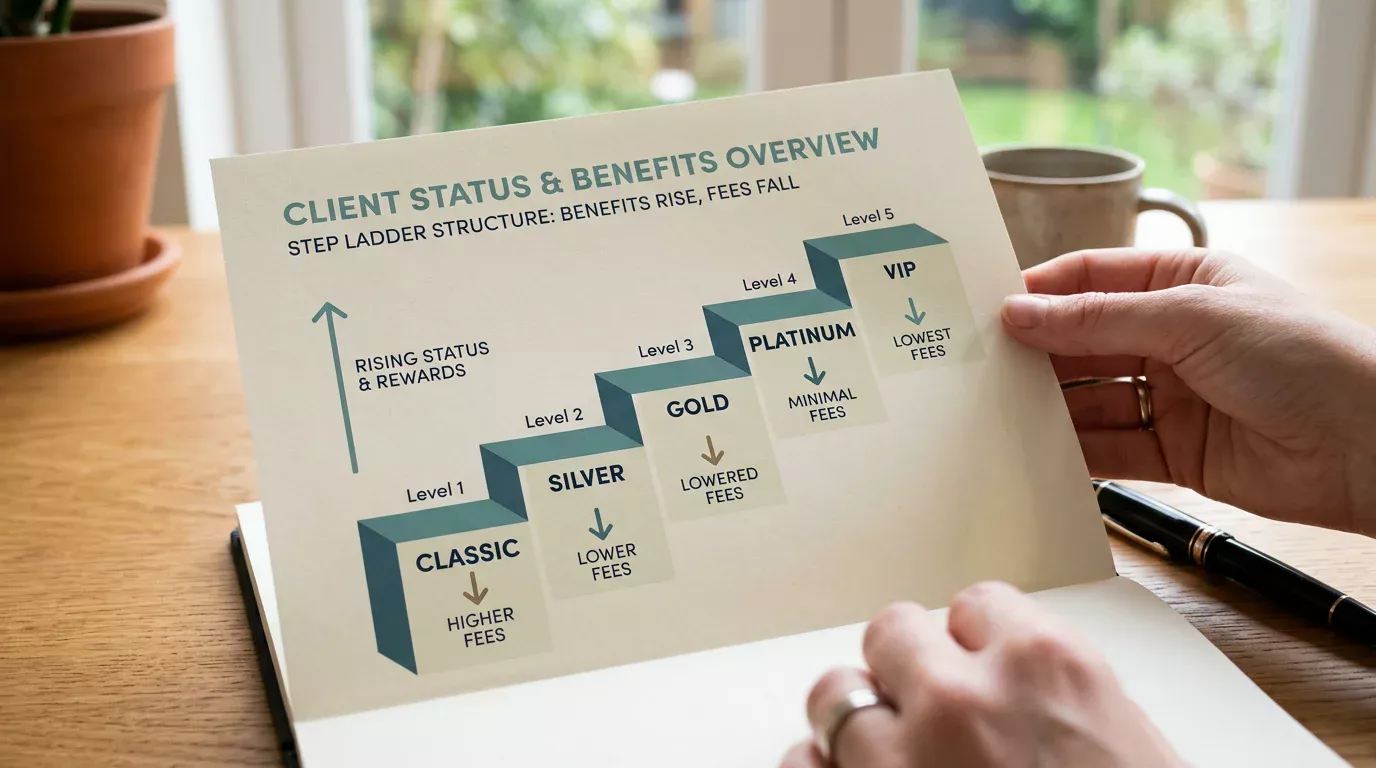

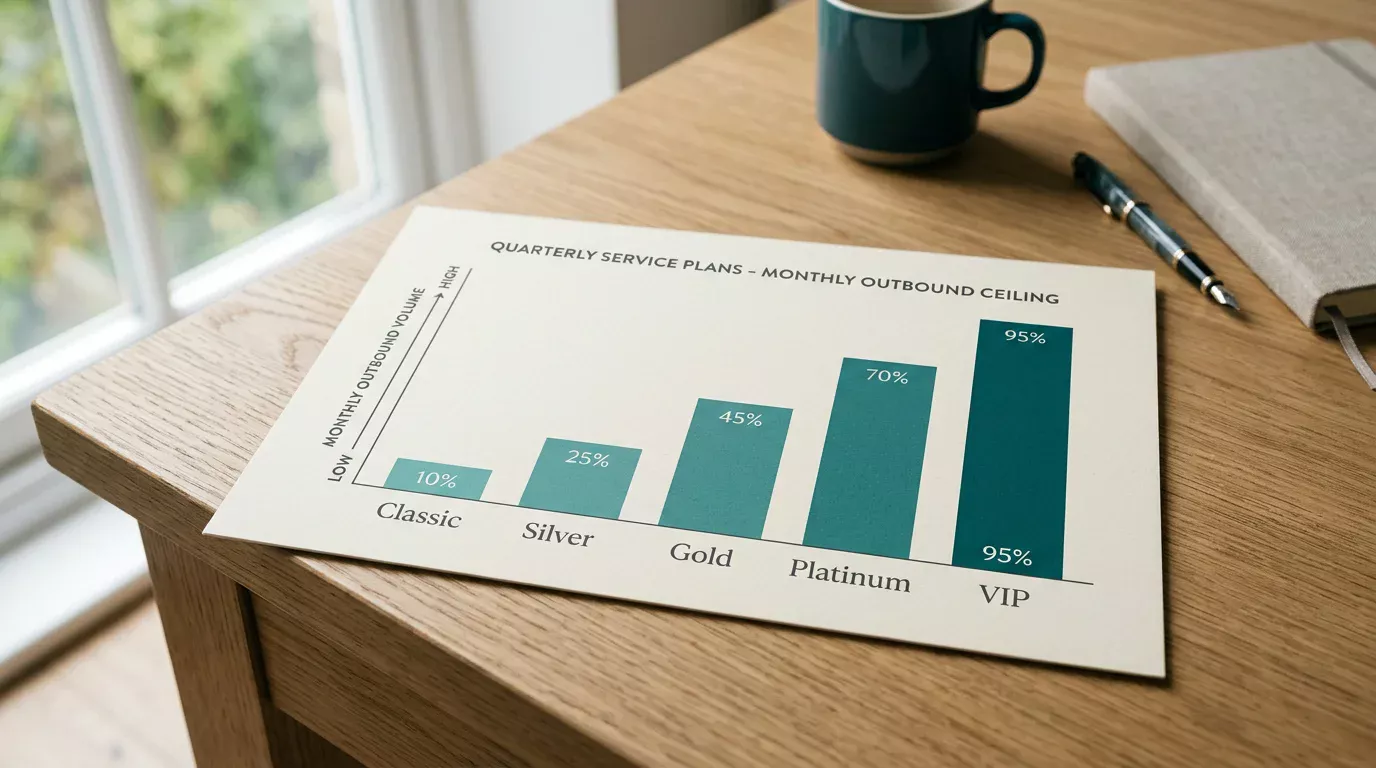

The withdrawal leg is where Payz’s tier structure starts to matter visibly, and where the cost gap between Classic-tier and upper-tier users shows up in real money. PSI-Pay Ltd operates Payz across 174 countries with the same five-tier ladder — Classic, Silver, Gold, Platinum and VIP — and each step changes both the fee profile and the access to faster or more flexible withdrawal routes.

Classic is the entry tier and carries the highest fees on standard withdrawals from the Payz wallet to external destinations. The published Payz fee schedule has historically set Classic-tier withdrawals to bank accounts at a few pounds per transaction, with debit card and other destinations carrying their own per-route charges. The published amounts have shifted occasionally over the years as PSI-Pay has restructured its pricing, but the broad shape — Classic pays most — has stayed consistent.

Silver brings down the per-transaction fees and unlocks higher monthly outbound ceilings. Gold reduces the fees further. Platinum reduces them again. VIP, the highest tier, typically waives standard withdrawal fees on common destinations entirely, though access to the VIP tier is restricted by activity and account standing and is not something you can buy outright.

The casino does not see your Payz tier, and the casino’s cashier does not charge differently based on it — but the after-cost amount that lands in your bank account does depend on your tier. A £1,000 withdrawal at Classic tier might net you a few pounds less than the same withdrawal at Gold tier, and across a year of regular play the gap can become material.

The cost-rationalisation move for active players is to monitor your monthly outbound volume and decide whether to consolidate activity through Payz at a higher tier or split between Payz and another wallet. For most UK players who deposit and withdraw a few hundred pounds a month, Classic-tier fees are tolerable. For anyone above that, the tier upgrade pays for itself.

The 2.99% FX Margin and Where It Actually Applies

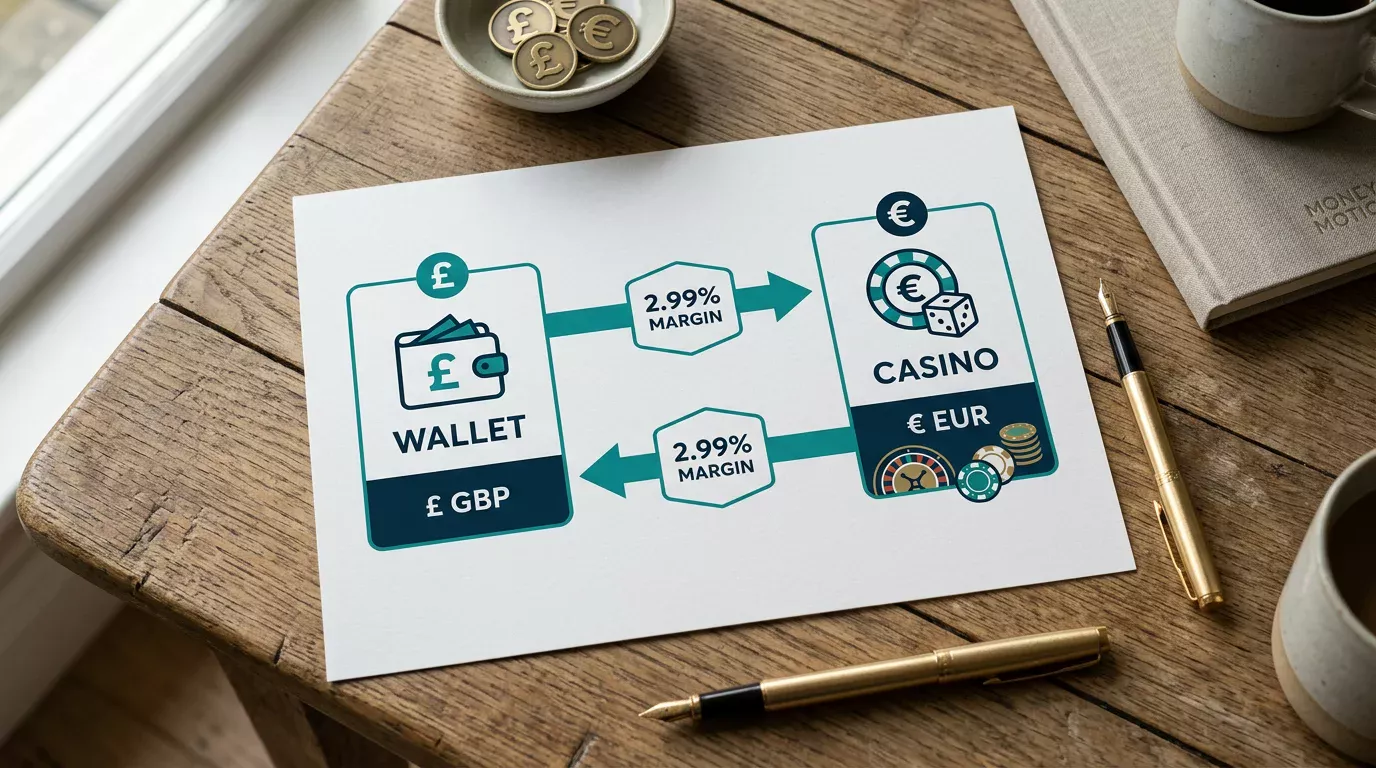

The 2.99% currency conversion margin is the most expensive part of Payz for any player whose pattern crosses currencies, and the most misunderstood. It is not a fee in the conventional sense — it is a margin layered on top of the mid-market exchange rate that PSI-Pay sources from the interbank market.

Where it applies is more specific than most players realise. A GBP balance deposited at a GBP-denominated casino lobby triggers no conversion and no margin. A GBP balance deposited at a casino whose game lobby runs in EUR triggers conversion at the cashier, and the 2.99% applies on the way in. A withdrawal from that same EUR-denominated casino back to a GBP Payz balance triggers conversion again — and the 2.99% applies on the way out, charged on the new direction. A round trip across currencies pays the margin twice.

It also applies on intra-wallet conversions. If you hold a multi-currency Payz balance — say GBP and EUR pockets — and you manually convert from one to the other inside the wallet, the 2.99% applies on the converted amount. There is no internal-transfer exemption.

What it does not apply to: GBP-to-GBP transactions at any stage, including the deposit leg, the wallet hold and the withdrawal leg. If you can keep the entire flow in pounds end to end, you pay no FX margin at all.

Dormancy Fees and Other Charges UK Casinos Will Not Mention

The fees nobody mentions at deposit time are the ones that bite long after the casino session is forgotten. Two categories matter for any Payz user who is not depositing weekly.

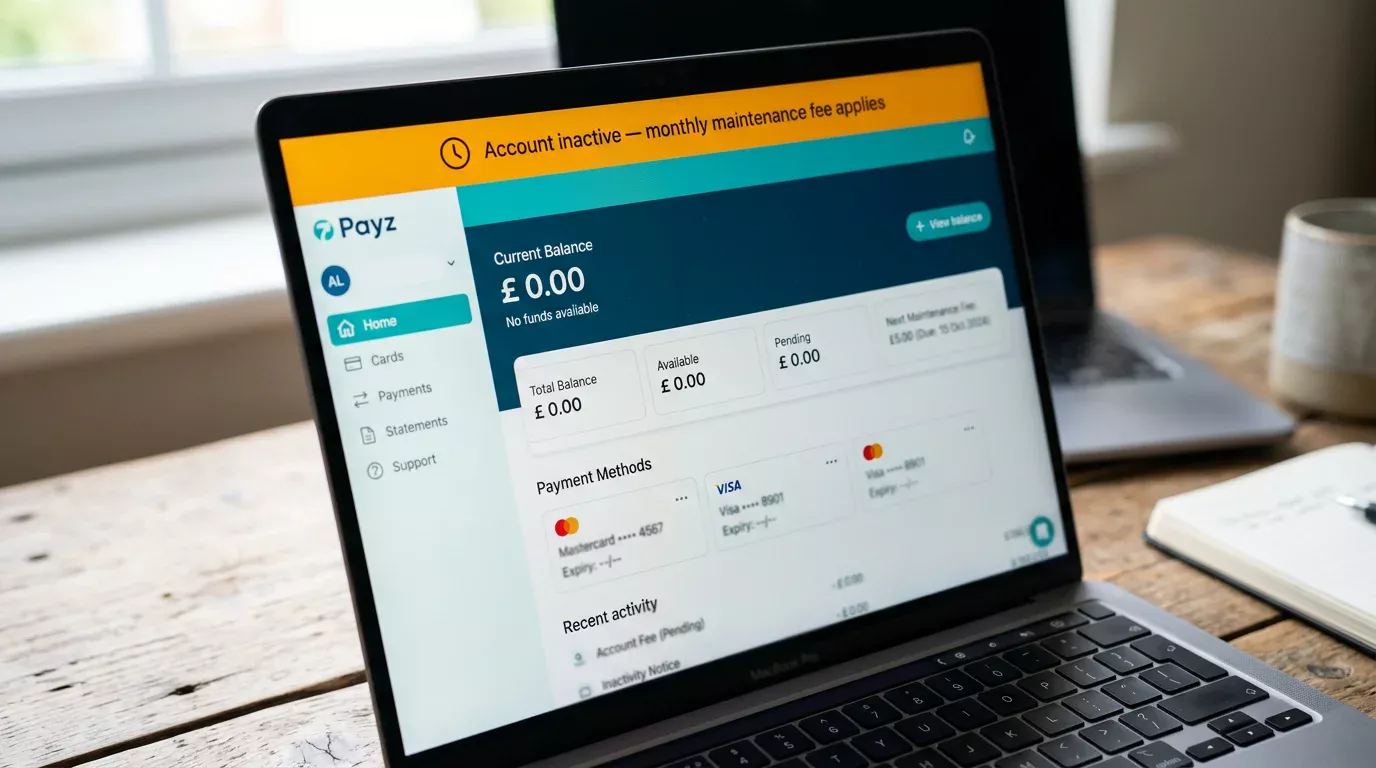

Dormancy fees are the first. Payz, like most FCA-authorised e-money institutions, applies a small monthly maintenance charge on accounts that have been inactive for an extended period — typically twelve consecutive months without a customer-initiated transaction. The charge is documented in the Payz terms and is a fixed monthly amount in the wallet’s holding currency. It is not large in any single month, but on an inactive account it accumulates until either the balance is exhausted or the account is reactivated. The fix is straightforward: log in and complete at least one transaction every twelve months, even if just an internal currency conversion or a balance transfer.

Maintenance and ancillary charges are the second. These cover document-refresh requirements on certain tiers, replacement of physical instruments where applicable, certain customer-service requests, and account-closure operations with balance still on the wallet. None of these is large individually. All of them are documented in the wallet’s terms. Almost none of them are mentioned at the casino cashier.

The pattern UK casinos genuinely do not mention is the chained dormancy risk on a multi-wallet user. If you maintain Payz alongside Skrill and Neteller and let one of them go inactive — say, after switching most of your activity to a different wallet — the inactive wallet starts accumulating dormancy fees. Over two or three years, an abandoned wallet with a small residual balance can be quietly drained by these charges.

The administrative discipline that saves you money here is to either consolidate your activity to one wallet you actually use, or to close wallets you have stopped using rather than leaving them with a residual balance.

Daily, Monthly and Annual Limits at Each Payz Tier

Limits at each Payz tier work on three time bands — daily, monthly and annual — and they apply to inbound and outbound flow separately. The tier ladder lifts the ceilings progressively, but the ceilings are not linear, and the gap between Classic and VIP is larger than the gap between Silver and Gold.

At the Classic tier, daily inbound is capped at a few thousand pounds, monthly inbound in the low five figures, and annual inbound similarly capped. The outbound side is tighter, with daily withdrawal caps in the low thousands and monthly caps that bite for anyone trying to move serious volume through the wallet. The exact figures shift occasionally; PSI-Pay publishes the current numbers in its terms and conditions and updates them as part of normal compliance maintenance.

Silver lifts each band by roughly half, Gold by another step, Platinum more, and VIP brings the ceilings high enough that the operator’s per-transaction limit usually bites first. For external reference, Skrill’s published UK casino deposit ceiling reaches £20,000 per transaction at the upper end of the Paysafe-family tier structure, with withdrawals up to £10,000. The shape of the high-tier ceilings on Payz is comparable; the precise numbers vary, but the same architecture applies — higher tier, higher ceiling, fewer practical constraints.

The constraint that matters in practice is the monthly outbound cap, because that is the one that throttles withdrawals across a busy month. If you withdraw £2,000 in week one of a month from a Classic-tier wallet, you may find your week-three withdrawal bouncing because the cumulative monthly cap has been reached. The cashier will not warn you in advance.

The pragmatic move for any UK player whose typical monthly withdrawal volume approaches the Classic ceiling is to either upgrade or split activity. PSI-Pay considers tier upgrades on a documented combination of account age, KYC level and activity history; an upgrade is not instant but the qualifying criteria are stable and predictable.

How the April 2026 Remote Gaming Duty Rise Leaks Into Payz Cashier Behaviour

April 2026 is the date every UK casino operator has been planning around for months, and it is also the date that quietly changes the cost calculus on every Payz transaction at a UK cashier — not because of any change at the wallet, but because of a change in the tax the operator pays.

From April 2026, Remote Gaming Duty — the tax operators pay on online casino gross gambling yield — rises from 21% to 40%. The general betting duty on online sports betting rises from 15% to 25% from April 2027. The change was announced in the Autumn Budget 2025, and the Chancellor Rachel Reeves was direct about the framing — remote gaming, she said, is associated with the highest levels of harm, and so the duty on remote gaming rises to 40% with online betting duty up to 25%. The Office for Budget Responsibility forecast the change will raise £810 million in 2026/27, growing to £1.16 billion by 2030/31.

The duty is paid by the operator, not by the player. But duty rises at this scale do not stay confined to the operator’s P&L — they leak into the cashier in a handful of predictable ways. The first is bonus compression. Operators facing a 19-percentage-point hit on their post-tax margin look for compensating savings, and the welcome offer is the most visible line they can prune. Smaller bonuses, higher wagering requirements, more aggressive e-wallet exclusions.

The second is payment-method pricing. The settlement fees operators pay to wallets like Payz are negotiated; in a duty-pressured environment, operators push back on costs across the cashier. Some of that pressure shows up as new player-side fees on certain rails, particularly on smaller deposits where the operator’s margin is already thin.

The third is throughput optimisation. Operators in a higher-duty environment have more incentive to keep average bet sizes up and bonus exploitation down, which tends to shift cashier policies in less player-friendly directions — tighter affordability gates triggering on slightly smaller cumulative deposits, more aggressive enforcement of stake limits, more rigorous KYC at lower thresholds.

None of this is Payz-specific. All four major e-wallets, plus debit cards and the mobile wallets, sit inside the same operator economics. But the player who plans to stay on the same Payz pattern through 2026 should expect the cashier experience to evolve — and not in the direction of cheaper, friendlier or more generous.

The Honest Cost Reading for UK Payz Users

The headline reading on Payz costs is misleading because the headline only shows you one of five layers. The accurate reading requires looking at the deposit leg, the withdrawal leg, the FX margin, the dormancy charges, and the tier-driven differential — and totalling them across a realistic six-to-twelve-month play horizon rather than a single transaction.

By managing your account tiers effectively, you can reduce costs while enjoying games at the best ecoPayz casinos on the market.

For a UK player on a GBP-only pattern, depositing and withdrawing a few hundred pounds a month at a UKGC-licensed casino, Payz at Classic tier is competitive with the rest of the e-wallet field — a small per-withdrawal fee on the outbound leg, zero on the deposit leg, no FX margin. The visible cost over a year is small.

For a player whose pattern crosses currencies, the FX margin becomes the dominant cost line and Payz is not categorically cheaper than its competitors. The discipline that controls this cost is to keep your wallet currency aligned with your casino lobby currency, and to avoid round-trip conversions inside the wallet.

For any UK Payz user looking at 2026, the variable that will move most is not the wallet’s fee schedule — it is the cashier environment shaped by the April duty rise. Bonuses will get smaller, gates will get tighter, and the value proposition of the e-wallet rail will shift around it. The wallet itself stays the same shape. The water around it does not.

Published by the Paylobby team.