UK Tax Updates: Remote Gaming Duty 40% and Payz Offers

The morning of 27 November 2025, I had three reader emails open at once. All three asked variations of the same question: my favourite casino just trimmed its welcome bonus, why? They had read the Autumn Budget headlines the previous evening but had not yet connected the dots between Treasury announcements and a 30% smaller bonus showing up at their casino the next morning. The dots were short. Remote Gaming Duty was going from 21% to 40% in April 2026, the operator’s margin model was about to compress significantly, and the bonus budget was the first lever they pulled in anticipation.

The duty change is the largest single structural shift in the UK regulated gambling market in years. It does not apply to players or to wallets directly. It applies to operators’ gross gambling yield. But the way operators absorb a 19-percentage-point duty rise inevitably reshapes the cashier experience for the player at the other end, and Payz-funded customers — disproportionately concentrated in the more bonus-aware end of the market — are likely to notice the changes first.

Direct Operational Implications of the RGD Adjustment

From April 2026, Remote Gaming Duty rises from 21% to 40%, and the new general betting duty of 25% follows in April 2027. The Office for Budget Responsibility estimates the package will raise £810 million in 2026-27, building to £1.16 billion by 2030-31. The duty applies to operator gross gambling yield — broadly, stakes received minus prizes paid out — so it sits directly on the operator’s revenue line before they pay any of their own costs.

Chancellor Rachel Reeves framed the rationale plainly in her Autumn Budget speech: “Remote gaming is associated with the highest levels of harm and so I am increasing remote gaming duty from 21% to 40%, with duty on online betting increasing from 15% to 25%.” The harm-cost link is the policy justification; the revenue is the practical motivation. A nearly doubled duty rate on remote gaming is a fiscal intervention of a scale that operators cannot absorb without changing their economic model.

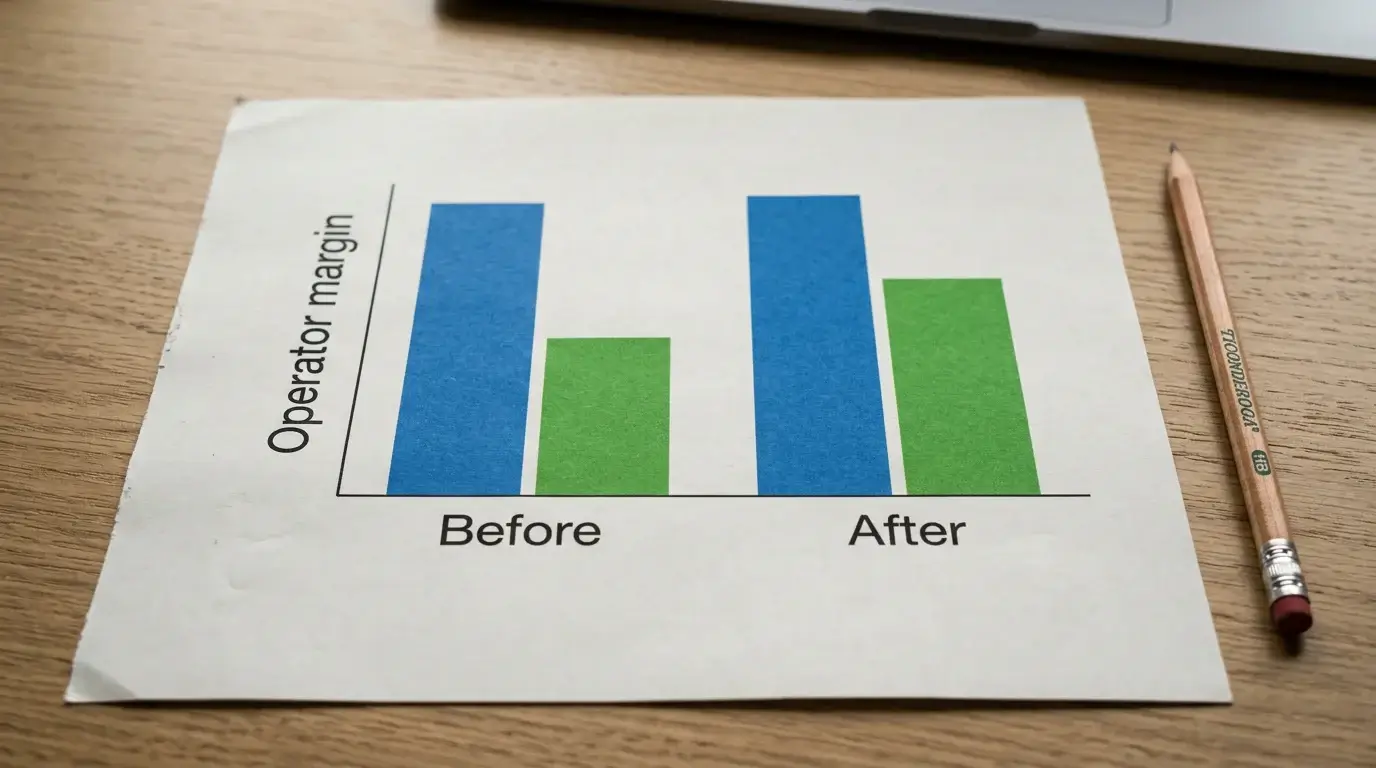

The duty applies per operator regardless of how the customer funded their account. A £100 deposit via Payz that becomes £100 of stakes and £85 of payouts creates £15 of gross gambling yield. Under the old 21% rate, the operator paid £3.15 in RGD; under the 40% rate, the same £15 of yield generates £6 in duty. The operator’s net margin compresses, and every pound less of margin has to come from somewhere downstream.

How Operators Pass the Cost Through to the Cashier

Operators have four broad levers to absorb a duty increase: reduce promotional spending, tighten game RTPs where regulatorily permitted, raise customer-acquisition friction, or accept lower margins. Industry signalling so far points to the first two as the dominant responses, with the second largely off-limits in slot products because RTPs are typically published.

John O’Reilly, CEO of Rank Group, put the industry view bluntly on the day of the Budget announcement: “The announced increase in remote gaming duty in the UK budget represents a very significant blow to the regulated betting and gaming industry in the UK.” The framing matters — operators are signalling that they cannot absorb the duty cleanly, which means players will see consequences in cashier terms over the months following implementation.

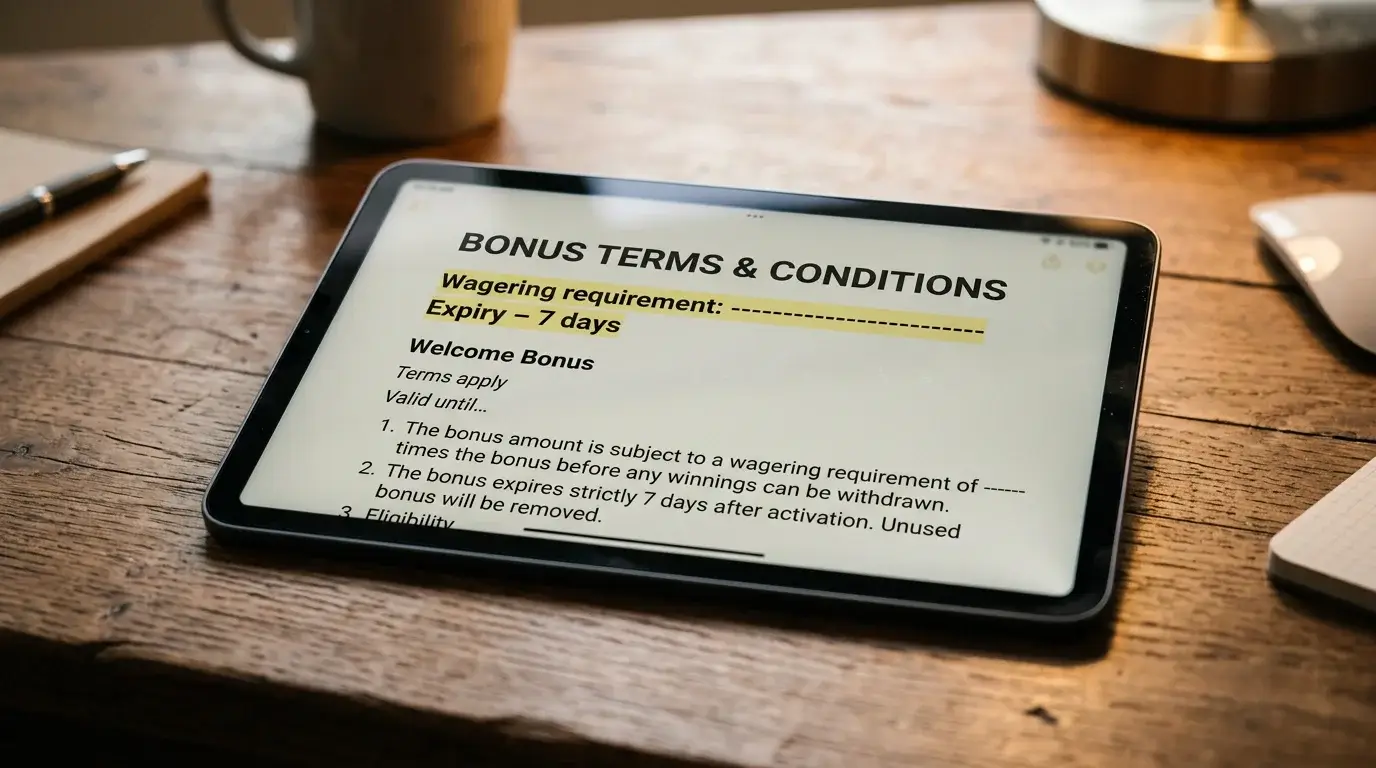

The most visible early changes have been on the promotional side. Welcome offers have been trimmed in both headline value and underlying terms. A bonus that previously came with 30x wagering requirements now arrives with 40x or 45x. Free spin counts have shrunk, max bet caps during wagering have tightened, and time windows to clear bonus play have shortened. None of these changes are illegal or unusual — operators retain full discretion over bonus design — but the direction is consistent and the underlying cause is the duty pass-through.

What Changes for the Payz-Funded Customer Specifically

Payz users sit disproportionately in the bonus-aware segment of the UK casino market. The wallet’s appeal includes its handling of bonus eligibility (separate from card-funded deposit rules that some operators apply), and players who chose wallet funding partly for bonus reasons are more sensitive to the bonus structure than the average customer. The trimmed bonus environment hits this segment harder.

Concretely, expect the following changes through 2026. Headline welcome offers shrinking by 20-40% in advertised value. Wagering requirements rising by 5-10 multiples. Bonus expiry windows narrowing from typical 30-day terms toward 14- or 21-day terms. Free-spin counts on slot promotions dropping by similar percentages to the cash bonus component. None of this is destructive to bonus availability — bonuses still exist and still clear with normal play — but the value-to-effort ratio has shifted against the player meaningfully.

I have updated my standard advice to readers about how Payz bonus eligibility works at UK casinos to reflect the post-RGD reality. The mechanics of qualifying for and clearing bonuses have not changed; the economics of whether the bonus is worth pursuing has. Players need to read terms more carefully than they used to, because the gap between a generous bonus and a punitive one has widened.

What Is Not Affected

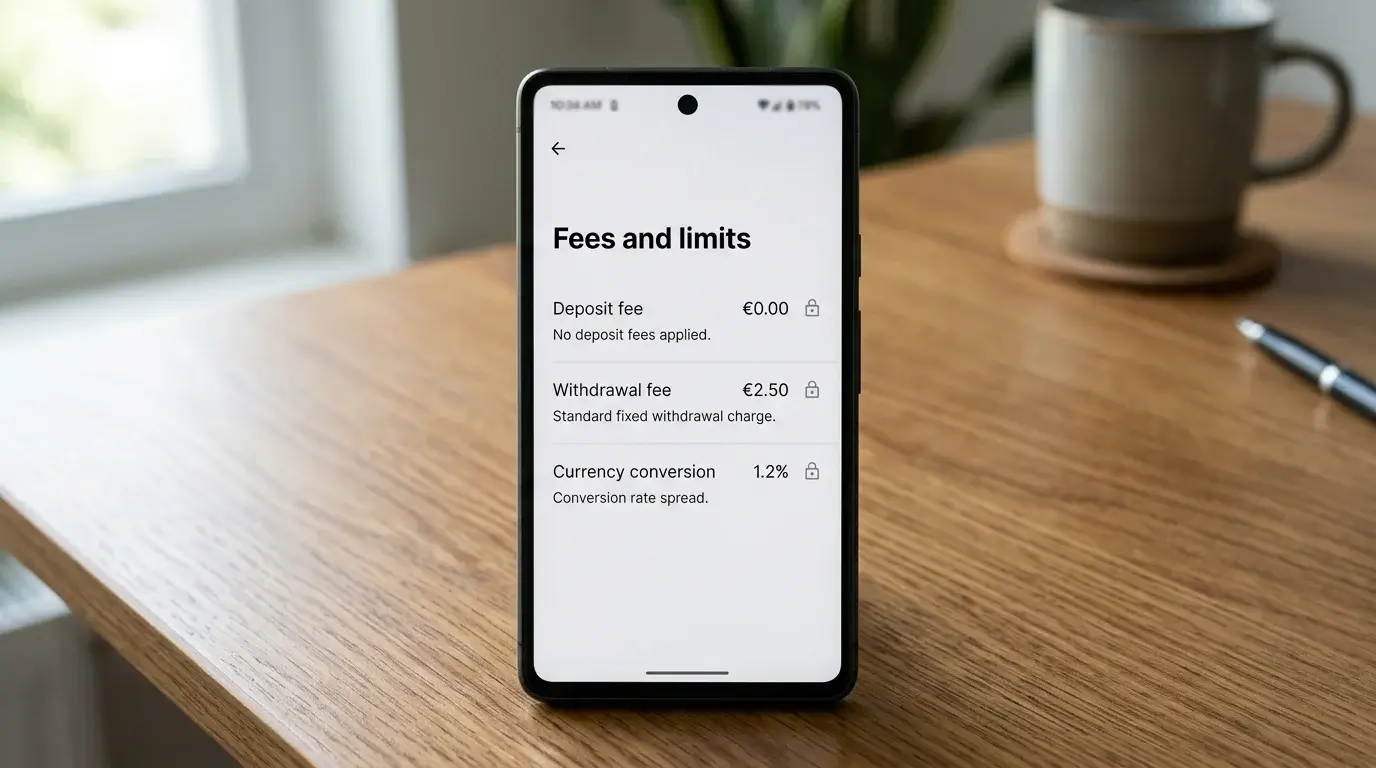

The duty change does not affect the wallet itself in any direct way. Payz fees, tier structures, deposit limits, and withdrawal timelines are set by PSI-Pay and the wallet’s own economic model. They are unrelated to UK gambling duty. Players sometimes ask whether Payz will raise its own fees in response to RGD; the question conflates two different markets. The wallet’s economics depend on its own revenue model, not on the regulatory cost burden of one customer segment.

The duty also does not change deposit minimums, withdrawal mechanics, or KYC requirements. The regulatory framework around the player-operator relationship is set by the UKGC and applies regardless of duty rate. A £10 minimum deposit at a UK casino in March 2026 is still a £10 minimum deposit in May 2026. The £150 vulnerability check threshold continues to apply unchanged. The £5 per-spin stake limit is unaffected.

What changes is downstream of those rules — the offers and incentive structures operators build on top of the regulatory floor.

The Competitive Asymmetry the Duty Creates

One under-discussed effect of the duty change is its impact on the regulated-versus-unregulated market split. UK channelisation — the share of UK player activity that runs through licensed operators — has slipped from 97% in 2019 to 92% in 2025, and a meaningful duty increase concentrated on regulated operators creates further pricing pressure that the unregulated market can exploit. Unlicensed offshore operators do not pay UK RGD; they can offer headline terms that regulated operators cannot match.

This is the part of the policy debate that has played out most vocally since the Budget. Operator bodies argue that doubling duty on the regulated sector while not increasing enforcement against the unregulated market shifts customers offshore. Regulators argue that channelisation is being defended through other means (UKGC cease-and-desist notices, search-engine cooperation, payment-blocking). The duty change is not happening in isolation — it sits alongside ongoing enforcement work — but the net effect on channelisation will be a 2026-2027 story to watch.

For Payz-funded players specifically, the risk is the temptation to follow more aggressive offers offshore. The wallet works at unlicensed operators in some jurisdictions, but the player protections available at UK-licensed operators (deposit limits, self-exclusion via GAMSTOP, ADR routes, FOS access) do not transfer. The £150 vulnerability check exists at UK-licensed sites and not at offshore ones. The Financial Ombudsman covers disputes with FCA-regulated entities and not with offshore operators. The decision to follow offers offshore is a decision to step out of the UK regulatory protection envelope, and the cost of that decision usually only becomes visible when something goes wrong.

The Realistic Player Adjustment

If you are a regular Payz-funded UK casino player, the practical adjustment for 2026 is modest in mechanics and significant in psychology. The mechanics: read bonus terms more carefully than you used to, particularly wagering requirements, max bet caps during wagering, and expiry windows. The psychology: recalibrate what counts as a “good” offer. What counted as an average offer in 2025 reads as a strong offer in 2026. What counted as a strong 2025 offer may not exist in 2026 at all.

For non-bonus play — straight deposit, play, withdraw — almost nothing has changed. The duty hits operator margins on yield, not on cashflow direction. Withdrawals still work. Deposits still clear. KYC still runs frictionlessly. The shift is in the promotional layer that surrounds the core product, and players who do not chase promotions barely notice the change at all.

The longer-term question is whether the duty rate at 40% holds. Industry groups will lobby for partial reversal. The Treasury will measure the revenue against the OBR forecast and adjust if the numbers diverge significantly. The £810 million figure for 2026-27 is the baseline against which the policy will be judged; if duty revenue undershoots that, the case for revision strengthens. None of this is settled, and the next 18 months will reveal how the market adjusts and how regulators respond.

The Settled View From the Cashier

From the player’s seat, RGD at 40% is a quieter change than the headlines suggested. Bonuses are leaner. Wagering is heavier. The everyday experience of depositing through Payz, playing through bonus or non-bonus balance, and withdrawing winnings is structurally the same. The cost of being a regulated-market customer has gone up, paid mostly through reduced promotional generosity rather than higher upfront costs. Whether that trade-off is worth it for any individual player depends on how much value they extracted from the more generous pre-2026 promotional environment in the first place.

For most readers I correspond with, the answer has been: not enough to chase the alternative. The regulated UK environment is leaner now than it was. It is still the better environment to play in. The duty change is real, the cashier consequences are real, and the right response is to recalibrate expectations rather than to take risks elsewhere.

Prepared by the Paylobby editorial staff.