Gaming Anonymity: ecoPayz Casino Privacy and Statements

A reader emailed me last winter with an oddly specific question: would the word “casino” appear on his bank statement if his wife pulled it up during their joint finances review the next month? He was not hiding gambling — they had agreed a monthly spend together — but he did not want the line items to broadcast which operator. I sent him the same answer I send everyone who asks this question. The Payz wallet, when used between your bank and a casino, breaks the visible chain. Your statement shows a transfer to a regulated e-money institution. It does not show the destination.

Privacy in this context is not about secrecy from regulators or from spouses who matter; it is about the difference between sensitive transactional detail and routine financial activity. Card-direct payments to casinos appear on statements with merchant descriptors that include the operator’s brand. Wallet-routed payments do not. This is a structural property of how the payments network labels transactions, not a privacy feature designed for any particular reason, and understanding it precisely matters more than reading marketing copy that promises “anonymous” play.

Transaction Descriptions Appearing on Bank Statements

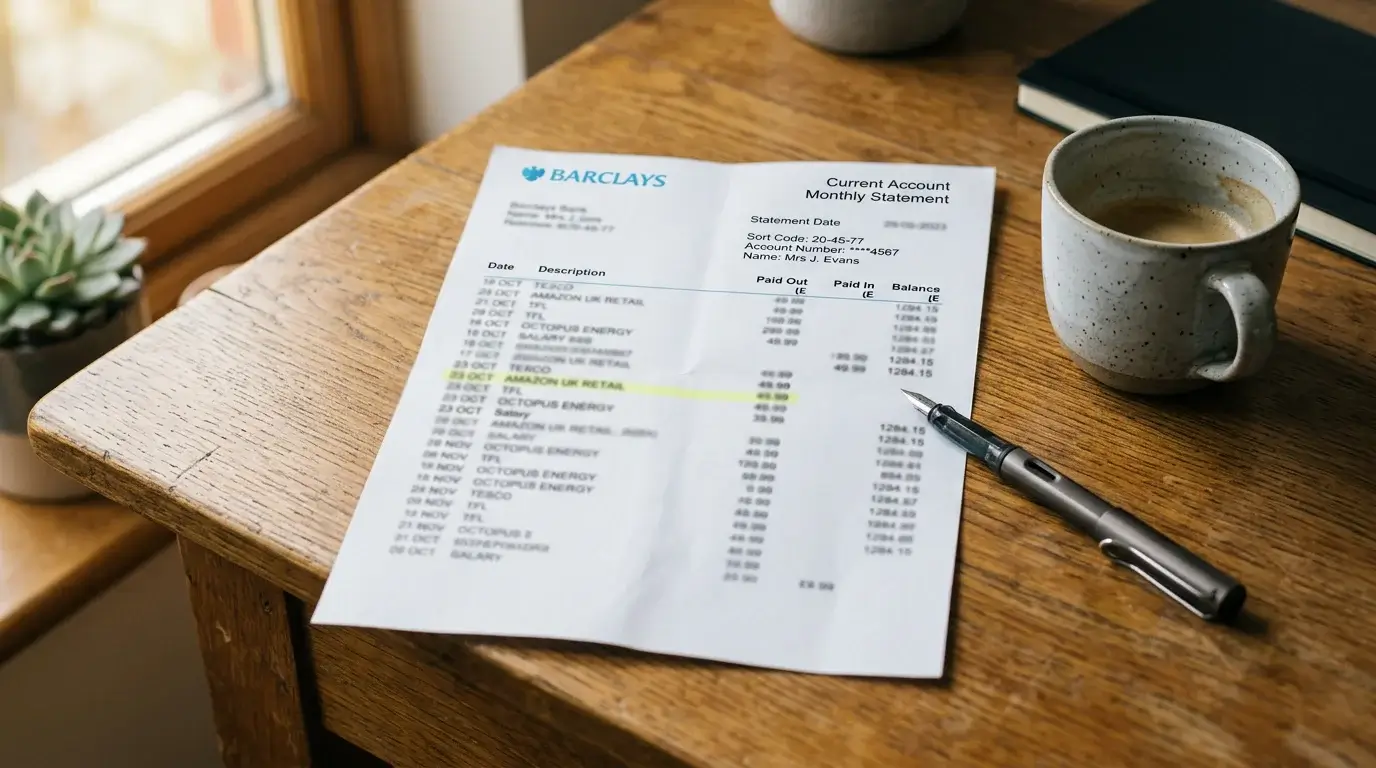

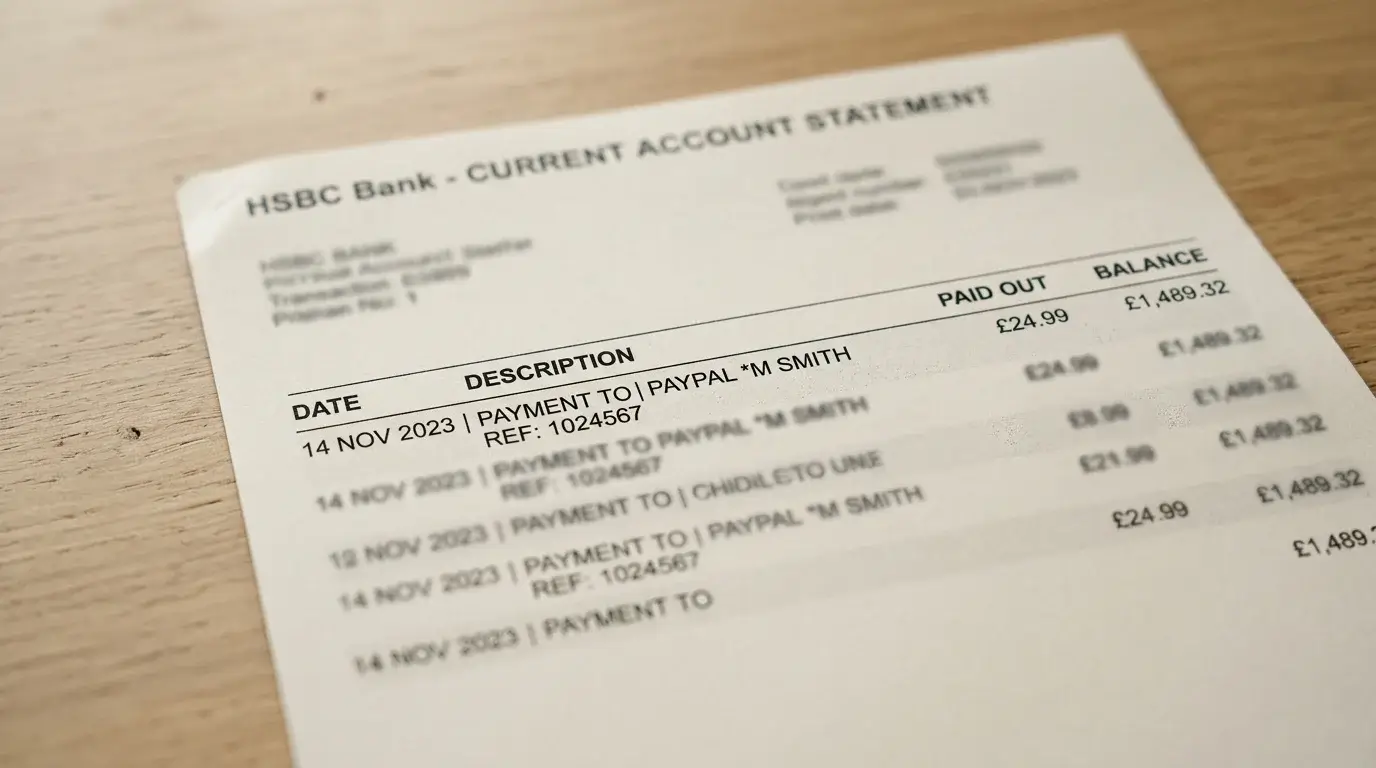

A direct debit card deposit to a UK-licensed casino typically shows on a statement with a descriptor that includes the operator’s trading name and a merchant category code identifying gambling. Banks render the descriptor differently — some abbreviate, some show the full corporate name — but the casino is identifiable. Anyone reviewing the statement can see where the money went.

A top-up to a Payz wallet from the same bank account shows differently. The descriptor identifies PSI-Pay Ltd or a related processing entity. The merchant category code is for e-money services, not for gambling. The line item reads as a transfer to a regulated payments institution. To a casual reader of the statement — or an algorithmic credit-scoring engine running over historical statements — the line item carries no gambling signal. PSI-Pay Ltd is FCA-supervised and operates across 174 countries; it is a well-understood e-money entity, and its descriptors look like routine payments activity.

What this does not mean: it does not mean the activity is hidden from anyone who is supposed to see it. Banks running affordability checks for mortgage applications can request transaction-level detail that goes beyond statement-line descriptors and can see the wallet inflow. Credit-reference agencies do not directly see gambling activity, but lenders running enhanced due diligence on a borrower can request the same detail. The wallet creates a layer of casual privacy, not a structural barrier to legitimate financial inspection.

What Payz Itself Sees

Inside the wallet, the picture is the opposite. Payz logs every transaction with its full counterparty detail. A £50 deposit to a specific casino is recorded as a £50 transfer to that casino’s payment account, with timestamp, transaction ID, and currency. The wallet’s transaction history is internally granular even where its external descriptors are generic.

This is part of the regulatory structure for an e-money institution. PSI-Pay operates under FCA authorisation and maintains AML obligations that require it to know who is sending money to whom. The wallet’s encryption — 256-bit SSL on transactions, PCI DSS compliance on the infrastructure — protects this data in transit and at rest, but the data exists. Privacy from regulators is not what the wallet provides. Privacy from the bank’s automatic descriptor labelling is.

The same Payz wallet that breaks the visible chain on your bank statement also generates a complete audit trail inside its own system. If you request a transaction history export, the wallet provides everything. If a regulator requests data under proper authority, the wallet has the data to provide. The user-facing privacy is one layer; the systemic visibility is another.

What the Casino Receives Back

The casino’s view of you is also worth understanding. When you deposit via Payz, the casino sees a payment from a Payz wallet, with the wallet’s unique identifier and the player’s account on the operator side. The casino does not see your underlying bank account. It does not see other transactions in your Payz wallet. It does not see how the wallet was funded. From the operator’s perspective, you are a verified Payz customer making a deposit; the deposit is what it cares about and the rest is none of its business.

This works in both directions. Withdrawals from the casino to the wallet are settled to the Payz infrastructure, not to your bank. The wallet then handles onward routing within itself if you choose to move funds. The chain of custody on funds from casino → wallet → bank involves three discrete legs, each with its own visibility, and the casino only sees the first.

The implication for player privacy is significant. Casinos cannot — and do not — correlate your activity at their site with your activity at competitors. They cannot see your aggregate spend across the wallet. They cannot infer what other operators you use. The wallet creates information silos that the operators on the other end cannot bridge.

The Privacy Versus Secrecy Line

Where this becomes uncomfortable is the distinction between legitimate privacy and attempted secrecy from people who should reasonably be in the loop. A few signposts I have learned to give readers.

Legitimate privacy: not wanting routine gambling activity to be visible to anyone scrolling through a statement for unrelated reasons. The wallet handles this well; the bank descriptor does not identify a casino.

Compliance privacy: not wanting gambling activity to feature in credit-decision processes that should not see it directly. The wallet handles this partially — credit-reference agencies do not see your casino activity through the wallet — but lenders running enhanced affordability checks on a mortgage application can ask for source-of-funds documentation that can reveal it.

Secrecy that is not privacy: hiding gambling from a spouse who is materially affected by household finances, or hiding activity from a self-exclusion register the player has signed up for. The wallet is not a tool for either of these. GAMSTOP exclusion applies at UK-licensed operators regardless of funding instrument. Spousal financial transparency is its own conversation and not something a wallet’s descriptor handling resolves.

The line between “I don’t want this casually visible” and “I am trying to evade a system I voluntarily joined” matters. The wallet works for the first; it does not and should not work for the second. Players who want to layer additional security around routine wallet use should consider two-factor authentication for ecoPayz casino logins as the more meaningful protection — securing the account itself is a higher-value privacy intervention than securing the bank descriptor.

The Data Payz Shares With Operators and Regulators

Payz, like any FCA-authorised e-money institution, has obligations to share data with the regulator on request and with operators to facilitate transactions. The wallet shares with the casino only what the transaction requires — the wallet identifier, the amount, the timestamp. It does not push promotional data, identity documents, or aggregate spend information to operators.

What the wallet shares with the UKGC, FCA, or HMRC under formal request is more comprehensive. The 256-bit SSL and PCI DSS protections cover ordinary operational security, not legal-process disclosure. A reader who asks “does Payz tell the UKGC about my gambling” is asking the wrong question. The UKGC has its own information channels and works with operators directly on player-protection issues. Payz is not a primary data source for player-protection decisions in the way the casino itself is.

The privacy contract, then, is between the player and the wallet for ordinary operational data; between the wallet and regulators for compliance data; and between the casino and the player (separately) for gambling-specific data. The three sit alongside each other rather than as a single chain.

What Good Privacy Hygiene Looks Like

For UK players who care about transactional privacy in the legitimate sense, the practical setup looks like this. Use Payz between your bank and the casino — the wallet breaks the visible chain on your statement without creating any compliance issue. Keep wallet 2FA active. Treat the wallet’s own transaction history as part of your personal financial record, retrievable on request but private to you. Do not use the wallet’s descriptor structure to obscure activity from people who reasonably should know about it.

For high-volume players, the privacy story is broadly the same but the visibility threshold matters more. A £50,000 a year transfer pattern to PSI-Pay Ltd, even with generic descriptors, will draw attention from any thorough financial review. The descriptor only conceals the destination, not the volume. Privacy from casual scanning is one thing; privacy from a careful auditor is another.

The Pragmatic Settled View

Privacy at the casino-wallet-bank junction is not what marketing copy makes it sound like. It is not anonymity. It is not invisibility to regulators. It is descriptor-level discretion — the routine kind of privacy that means a casual reader of your statement does not see “Casino X” rendered in bold next to a £50 line item. That is genuinely useful for the legitimate reasons people care about it, and it is honestly inadequate for any purpose the legitimate reasons do not cover.

The wallet does its job here well. It does not pretend to do more, and the marketing literature from PSI-Pay has historically been honest about what an e-money institution can and cannot provide. Privacy as a feature is real; privacy as a way around obligations is not. Readers who internalise the difference get the value of the structure without expecting it to do work it cannot do.

Created by the "Paylobby" editorial team.