Mobile Wallet Comparison: ecoPayz vs Apple Pay

A reader asked me last spring which payment method I would choose if I could only pick one for UK casino play. I gave him the answer I should give him — “it depends what you are optimising for” — and then he pushed back with the answer he was actually looking for, which was a recommendation. I declined to recommend, but I did walk him through the trade-offs between Payz and Apple Pay, and that conversation has shaped how I think about the comparison every time it comes up since. The two payment methods solve different problems with different architectures, and the right pick is the one that matches the problem the player actually has.

Apple Pay has grown into a serious force at UK online casinos over the past two years. Around 30% of UK online casinos now support Apple Pay, and Apple Pay and Google Pay combined have grown at roughly 47% year on year in UK casino payment volumes. Payz comes from a different lineage — a standalone e-money wallet rather than a tokenisation layer over a debit card — and the difference shapes every aspect of how each performs in the cashier.

Core Infrastructure and Network Differences

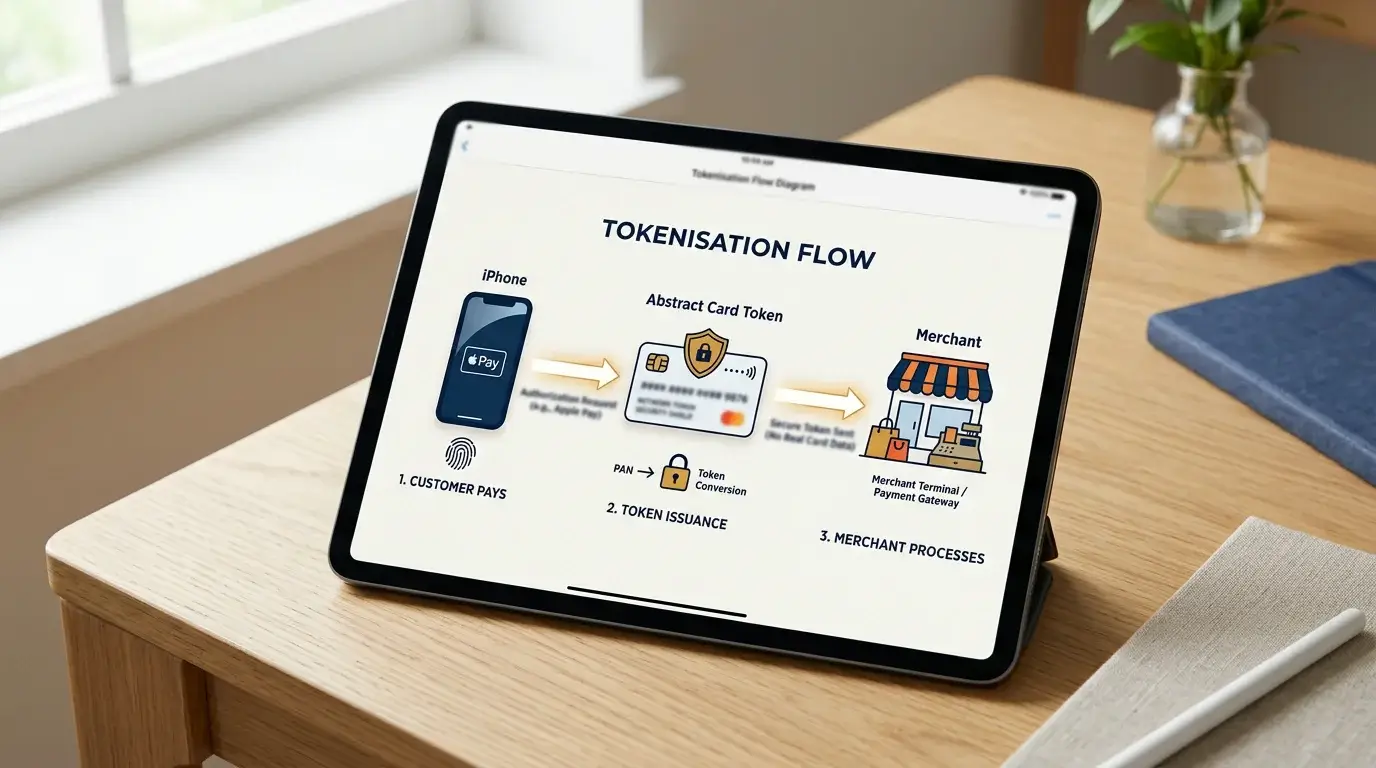

The single most important thing to understand about Apple Pay is that it is not a payment method in the sense Payz is. Apple Pay is a tokenisation and authentication layer that sits on top of an underlying debit or credit card. When you pay with Apple Pay at a casino, the casino does not see “Apple Pay” as a funding source — it sees a tokenised card transaction processed through the Visa or Mastercard network, with Apple Pay handling the device-side authentication and the token generation. The card behind the wallet is doing the actual paying.

Payz, by contrast, is a standalone e-money account at PSI-Pay Ltd, FCA-supervised and operating across 174 countries. The wallet holds its own balance, settles transactions on its own infrastructure, and is not a layer over anything else. When you pay with Payz, the casino sees an e-money transfer from PSI-Pay, not a tokenised card.

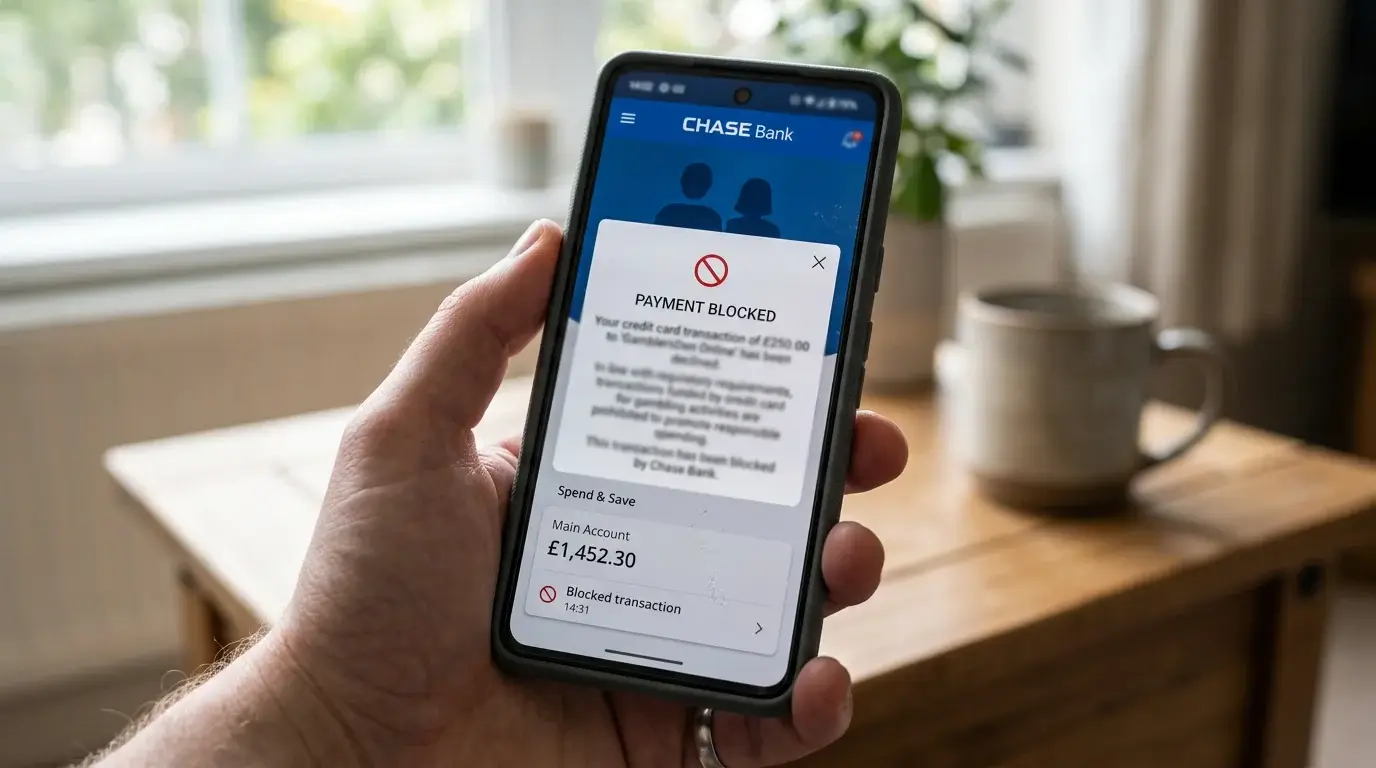

This difference matters in every direction. UK regulatory features that apply to the underlying card — including the credit card gambling ban that prohibits credit card funding of gambling — apply to Apple Pay if the underlying card is a credit card. Payz is unaffected by that ban directly because it is not a card transaction at the casino’s end, although Payz itself enforces credit-source restrictions on its own balance to comply with the same regulatory intent.

Speed at the Cashier

Both methods process near-instantly on deposits. Apple Pay benefits from device-resident authentication — biometric verification on the iPhone confirms the transaction in seconds, and the cashier sees the result almost immediately. The mobile-wallet population in the UK reached 42% of adults registered with a mobile wallet by the end of 2023, with 34% making contactless mobile payments monthly; that scale means Apple Pay deposit flows are highly optimised on operator-side.

Payz deposits process at comparable speed once authenticated. The wallet’s authentication step (typically a password and 2FA on a new device or new merchant) adds a few seconds compared to Apple Pay’s biometric flow, but the difference is friction rather than wait time. On established Payz-casino relationships, the cashier shows the deposit cleared almost immediately.

The withdrawal direction is where the two diverge. Apple Pay does not support withdrawals as such — funds returning from a casino route back to the underlying card via the standard card-rail refund process, which often takes several working days to settle. Payz withdrawals land in the wallet typically within 24 to 72 hours and become spendable immediately on landing, with onward routing to a bank or other destination as a separate user-initiated step. For players who care about withdrawal speed and want funds usable promptly, this matters.

Privacy and Statement Visibility

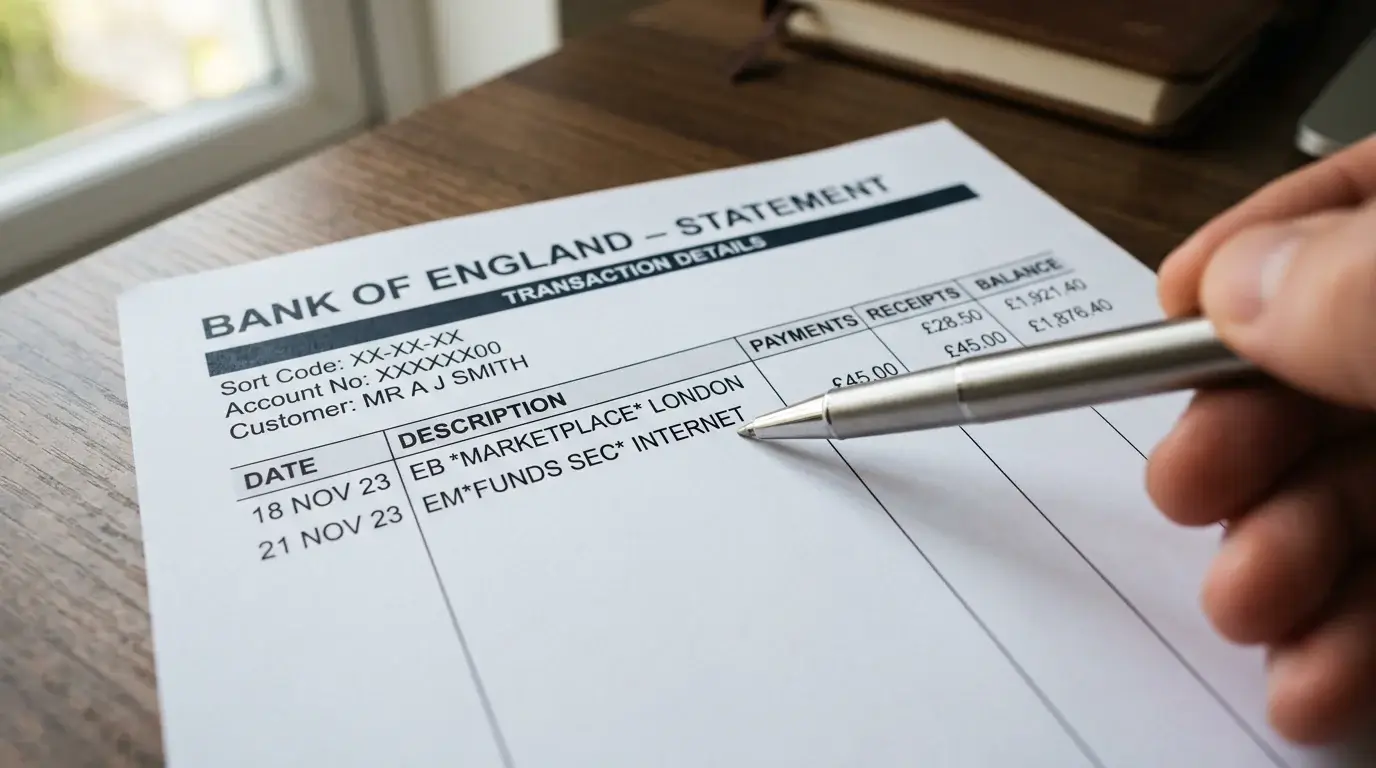

Apple Pay deposits at a UK casino appear on the cardholder’s bank or card statement with the casino’s merchant descriptor — usually the operator’s trading name and a gambling merchant category code. Apple Pay does not obscure the destination. The privacy story of Apple Pay is about the card number not being exposed to the merchant (tokenisation handles that), not about the casino being invisible on the statement.

Payz deposits show as transfers to PSI-Pay Ltd on the bank statement, with an e-money services merchant category code. The casino is not identifiable from the descriptor. This is the descriptor-level privacy I have written about elsewhere — it is genuine for the limited purpose of keeping casual statement readers unaware of casino activity, and it is honestly inadequate for any structural attempt to hide gambling from regulators, lenders, or anyone with audit authority.

The wallet wins this dimension if descriptor privacy is what you want. Apple Pay wins if you do not care about the descriptor and prefer the operational simplicity of biometric-authenticated card payments.

Coverage at UK Casinos

Roughly 30% of UK online casinos support Apple Pay, and the share is rising. Payz support is broader — close to universal at UK-licensed operators, partly because the wallet has been in the market longer and partly because e-money support is easier for operators to integrate than mobile-OS-specific payment methods. If you walk into a UK-licensed cashier expecting to find a payment method, Payz will be there at almost every operator; Apple Pay will be there at a strong minority and a growing one.

The CMA’s July 2025 designation of Apple and Google as having “strategic market status” under the Digital Markets Regulation will push toward broader interoperability and lower app-store charges, and this is likely to accelerate Apple Pay’s spread at UK operators over the next two years. The economics of supporting Apple Pay get cleaner for operators as the regulatory weight on the tech platforms increases.

The coverage advantage sits with Payz, particularly at smaller or specialist UK operators that have not yet invested in Apple Pay integration.

Fees and FX

Apple Pay itself charges no consumer-side fee — the cost sits in the merchant fees paid by the casino to the card network and to Apple. For UK GBP-to-GBP transactions, the cardholder sees no direct cost. If the underlying card is in a different currency, the card issuer’s FX margin applies; Apple Pay is currency-agnostic and just routes whatever the card does.

Payz charges its own fee structure depending on tier and direction. Currency conversion attracts a margin of around 2.99% above mid-market for retail conversions, with tighter spreads at higher tiers. Deposit fees are usually waived at Classic and above; withdrawal fees apply at certain thresholds; dormancy fees apply on inactive accounts. The full cost picture depends on activity volume and tier, and the wallet earns its place primarily on functions other than headline price.

For pure cost on GBP-to-GBP UK casino activity, Apple Pay (over a GBP debit card) is usually cheaper than Payz at the routine level. The wallet’s value proposition is not cost-minimisation; it is the bundle of descriptor privacy, withdrawal handling, and broad coverage.

When Each One Wins

Apple Pay wins when the player is on an Apple device, has a debit card they are happy to use directly with casinos, does not care about statement-level descriptor privacy, and wants the fastest possible deposit flow. The biometric authentication, the optimised mobile UX, and the cleanly-integrated experience all favour Apple Pay for the iOS-native casual user.

Payz wins when the player wants descriptor privacy on bank statements, values fast and clean withdrawals that land in a separate balance, uses operators that may not support Apple Pay, or needs cross-currency flexibility that a single underlying card cannot provide. The wallet earns its place for users who treat their casino activity as a distinct financial silo rather than as an extension of their everyday card spending.

For the player using both an iOS device and Payz, neither method excludes the other. Many readers I correspond with use Apple Pay for routine smaller deposits and Payz for larger transactions where withdrawal handling and privacy matter more. The two are complements, not substitutes.

I have written separately about how the equivalent comparison runs for Android users via Google Pay — the architectural points are similar but the platform-specific UX and the Android wallet’s integration with the broader Google ecosystem produce different practical trade-offs.

The Credit Card Ban Dimension

One specific architectural point matters for any player considering Apple Pay over a credit card: the 2020 UK credit card gambling ban applies to Apple Pay if the underlying card is a credit card. The Apple Pay token still presents as a card transaction, and the casino’s gambling-merchant code triggers the credit card block on the underlying card if applicable. Players sometimes assume Apple Pay sidesteps the ban; it does not.

Payz applies an equivalent restriction internally — the wallet does not knowingly fund gambling activity from credit card top-ups, and the same regulatory intent flows through. The architectural route is different but the outcome at the player level is similar: credit card funding of UK gambling is blocked regardless of which intermediation layer is in use.

The Pragmatic Settled View

Apple Pay and Payz are not interchangeable. They solve different problems, fit different player profiles, and earn different positions in a UK casino-funding setup. Apple Pay is the elegant default for iOS users with debit cards and no specific privacy or withdrawal-speed concerns; Payz is the structural choice for players whose requirements extend beyond the card-tokenisation model that Apple Pay provides.

The pick depends on what you actually need. Cost-minimisers on GBP card spending will land on Apple Pay. Withdrawal-sensitive or privacy-conscious users will land on Payz. Many players will use both, picking by context. The two payment methods have grown into a healthy coexistence in the UK market rather than into a winner-takes-all comparison, and the player who understands both can extract the value of each as their situation requires.

Prepared by the Paylobby editorial staff.