Approved Funding for ecoPayz Casino Wallets Under UK Rules

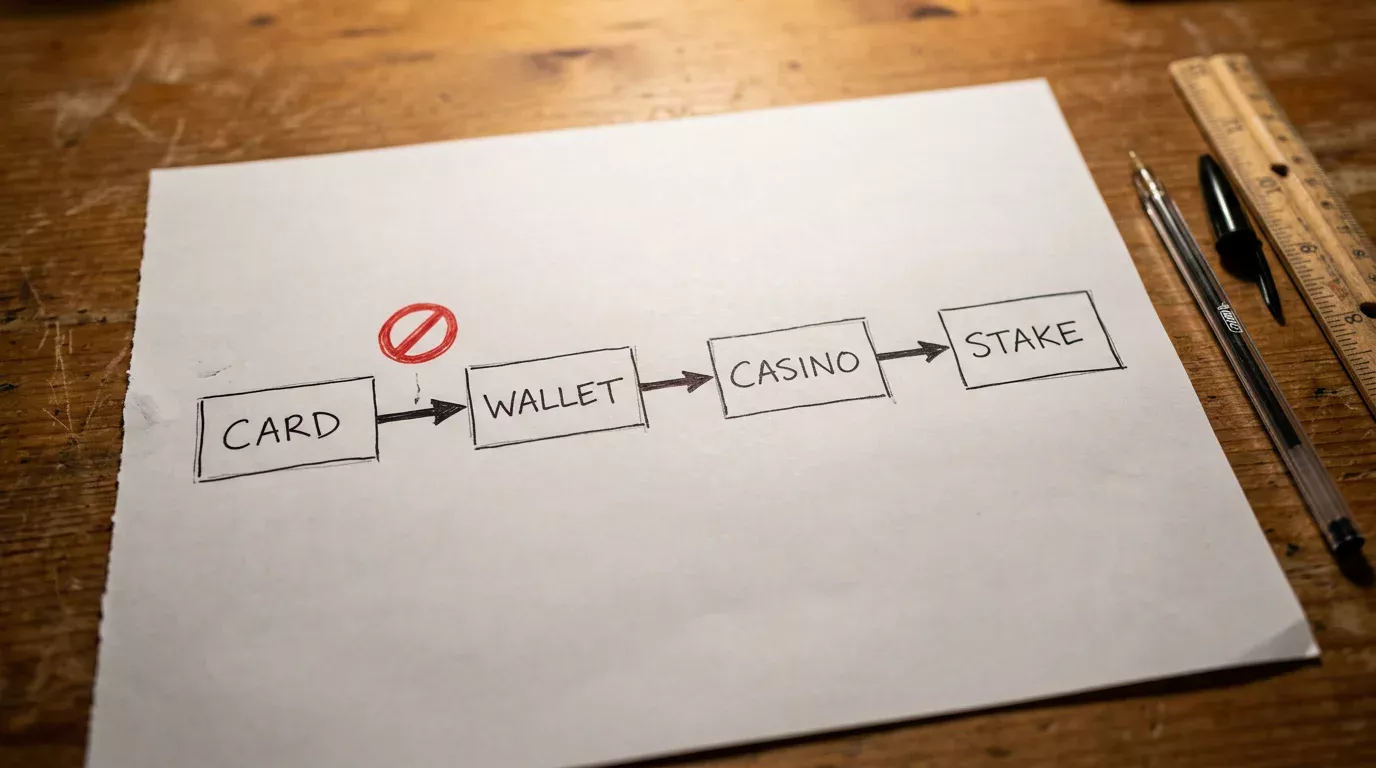

The 2020 UK credit card gambling ban is one of those regulatory changes that everyone references and almost no one fully understands. Readers regularly ask me whether they can top up a Payz wallet from a credit card and then deposit at a casino, on the assumption that the ban only catches direct card-to-casino transactions. The honest answer is “no, and the regulator was deliberate about closing that loophole”. The ban applies to the chain of funding, not just the final hop.

What I want to do is map the rule cleanly. The ban itself is short and the principles behind it are not complicated, but the e-wallet wrapper creates an intermediate layer where players sometimes assume the ban does not reach. It does. The chain matters. Let me walk through how the rule applies, why it exists, and what funding paths remain legitimate for a UK Payz user.

Scope and Parameters of the April 2020 UKGC Ban

The UK Gambling Commission’s ban on credit card gambling took effect on 14 April 2020. It prohibits operators from accepting credit card payments for gambling activities. The ban covers direct credit card deposits to a casino, sports betting account, or any other UKGC-licensed gambling product. It also covers indirect credit card funding routed through electronic money institutions like PSI-Pay — what the regulator calls “credit card use via e-wallets”.

The motivation was harm reduction. Before the ban, 5.7% of all UK online gambling deposits were funded by credit card, and within that group, 22% of credit card gamblers were classified as problem gamblers. That figure was substantially higher than the population average and pointed to a strong correlation between credit-funded play and gambling harm. As Andrew Rhodes, CEO of the UKGC, has put the regulatory philosophy: “We have to get the balance right between protecting people from the potentially life-ruining effects of gambling-related harm and respecting the freedom of adults.” The credit card ban was the largest single intervention that came out of that balancing exercise.

The ban does not affect non-gambling use of credit cards. You can still use a credit card to pay for groceries, to top up a Payz wallet that you do not use for gambling, or to fund a wide range of non-gambling merchants. What changes is that the chain leading to a UK gambling deposit must not include a credit card at any link.

The enforcement falls on operators and on the wallet provider. UKGC-licensed casinos have a licence condition obliging them to reject credit-funded deposits. PSI-Pay, as an FCA-regulated electronic money institution, has its own obligations to apply customer due diligence to the funding source. Both layers run checks, and either can decline a transaction that fails the credit-source test.

Funding a Payz Wallet From a Credit Card

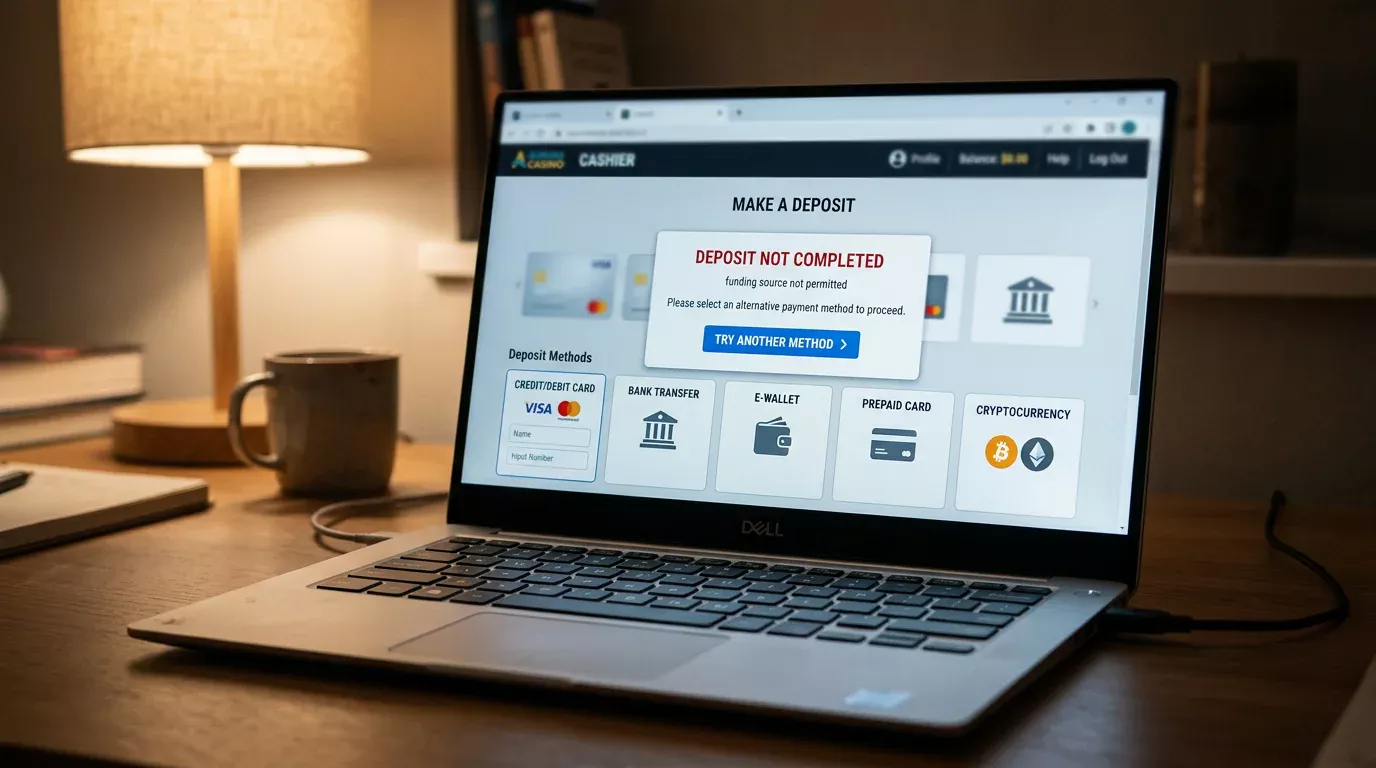

You technically can top up a Payz wallet from a UK-issued credit card. PSI-Pay’s wallet onboarding accepts credit cards as a funding instrument for non-gambling use. But the moment you intend to spend that balance on UK gambling — at any UKGC-licensed operator — the chain creates a problem.

The operator’s risk engine looks at the funding chain when a Payz deposit lands. The operator does not see your raw funding source directly; what they see is a transaction from PSI-Pay Ltd. But the wallet itself knows the original funding source, and several operators have integration arrangements where the wallet flags transactions originating from credit-funded balances. Even where the flag is not automatic, the wallet’s internal AML processes can decline a casino transaction sourced from a credit balance.

This means the chain “credit card → Payz wallet → UK casino” can fail at any of three points. PSI-Pay can decline the casino transaction. The operator can decline the deposit even after PSI-Pay processes it. Or the transaction can clear and then be flagged for retroactive review, with the deposit eventually reversed.

The retroactive scenario is the worst from a player perspective. You deposit, you play, you win or lose, and weeks later the operator reverses the deposit on the basis that it traced to credit. Winnings are forfeited; losses are not refunded because the transaction was the deposit, not the wagers. The operator is acting within its licence condition; the player carries the loss.

PSI-Pay’s Internal Policy on Credit Card Use

PSI-Pay’s published policy on credit card use for UK gambling has tightened since 2020. The wallet’s terms allow credit card top-ups in general but reserve the right to decline gambling-related transactions sourced from credit balances. In practice, PSI-Pay maintains internal flags on funding sources and applies them at the merchant level — gambling merchants get the credit-source check; non-gambling merchants do not.

The wallet’s interface does not always make this visible. You can fund the wallet from credit, see the balance increase, and only discover the problem when a casino transaction fails. The error message at the cashier is often generic (“transaction declined”) rather than specifically pointing at the credit source as the cause. The player diagnoses a Payz problem or a casino problem when the cause is actually the funding chain.

One nuance worth knowing. A Payz balance that has at any point been funded from credit can carry “credit taint” until the credit-sourced portion has been spent on non-gambling activities or withdrawn from the wallet. The accounting is at the balance level, not at the per-transaction level — you cannot earmark £20 of credit-funded balance for shopping and £30 of debit-funded balance for casino play. The wallet’s internal accounting treats the funding chain as commingled.

Safer Funding Paths for UK Casino Use

The clean paths are short and easy to describe. Use them and the credit card ban becomes irrelevant to your casino activity.

Path one: UK debit card. Most UK current accounts come with a debit card that can fund a Payz wallet, and debit cards are unambiguously outside the credit card ban. The top-up clears within minutes, the balance is available immediately, and casino transactions from that balance carry no credit taint. This is the default for most UK Payz users.

Path two: UK bank transfer. A direct transfer from a UK bank account to your Payz wallet is permitted and avoids the card-rail entirely. The transfer takes longer to settle — typically one business day, occasionally two — but the resulting balance is unambiguously not credit-sourced. For larger top-ups this is often the more economical option.

Path three: incoming casino withdrawals or other Payz transfers. Balance arriving from a casino withdrawal, from another Payz user, or from any non-credit source is, by definition, not credit-sourced. Players who recycle winnings from one casino to another via Payz are operating entirely within the rules.

What is not a safer path: routing credit through an intermediate non-Payz wallet and then into Payz. Some readers ask whether they can fund a Skrill wallet from credit, transfer to Payz, and then deposit at a casino. The answer remains no — the chain still contains a credit link, and the operator or the wallets in the chain may flag the transaction at any point. The ban applies to the chain, not just to the wallet of last resort.

The eco-Virtualcard generated from a Payz wallet is also worth mentioning here. The card is prepaid in structure, but if the underlying Payz balance carries credit taint, the eco-Virtualcard inherits it. A clean eco-Virtualcard requires a debit- or bank-funded Payz balance — anything else creates the same regulatory question the credit card ban set out to address. For a fuller treatment of the eco-Virtualcard at UK casinos, see my walk-through of the one-time prepaid card via Payz.

One regulatory direction worth watching. The post-2026 environment, with the Remote Gaming Duty rising and the financial vulnerability checks at £150, is pushing the regulator and operators toward more aggressive funding-source scrutiny. The credit card ban was the first move in that direction; further tightening of e-money funding chains is plausible. Keep your funding paths clean now and you will not have to reorganise later.

Created by the "Paylobby" editorial team.