UK Casino Banking: ecoPayz vs Trustly open flows

Trustly entered my reader correspondence about three years ago when a friend mentioned that he had stopped using his old e-wallet at his preferred operator and switched to “that bank-login thing” instead. He was describing Trustly’s Pay N Play product, which lets a player fund a casino account by authenticating directly with their bank through open banking rather than storing balance in an intermediate wallet. The conversation that followed shaped how I think about the two approaches — they are not really competing for the same role, and treating them as direct substitutes misses what each is actually for.

Pay N Play and the Payz wallet sit on different rails entirely. Payz holds a stored balance at an FCA-supervised e-money institution, with the player topping up and drawing down from that balance over time. Trustly pulls funds directly from the player’s bank account via open banking authentication, with no stored balance and no intermediate account at all. Both end up routing money from the player to the casino, but the mechanics, friction profile, and use-case fit diverge sharply once you look at the details.

Underlying Transaction Frameworks

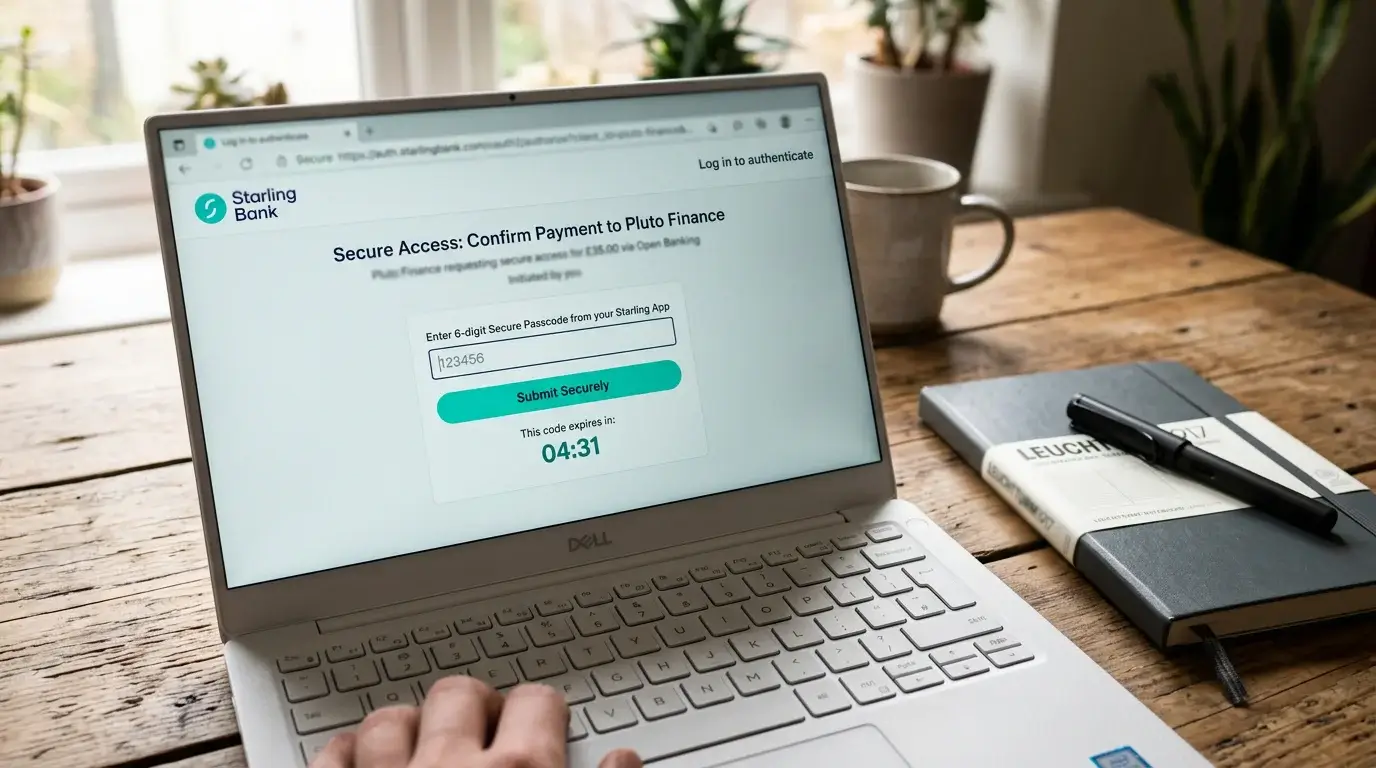

Trustly’s open banking integration uses the PSD2 framework to initiate a payment directly from the player’s bank account on the player’s authenticated instruction. The player logs into their bank during checkout via Trustly’s secure flow, confirms the payment, and the funds move from the bank account to the casino on the standard Faster Payments rail or its equivalent. No card network is involved. No e-money intermediate. The transaction is a direct bank-to-casino transfer with Trustly acting as the initiator.

Payz, in contrast, is a stored-value e-money account. You top up the wallet from your bank (or card, subject to the credit card ban applying), the wallet holds the balance as an e-money claim, and you deploy that balance into casino activity at your own pace. The deeper context here is the broader shift in UK digital payment behaviour — digital wallet spending in the UK is projected to grow from £269 billion in 2025 to £453 billion by 2030, and within that growth both stored-value wallets and open-banking-initiated payments are gaining share against legacy card payments. They are growing in parallel rather than competing for the same slot.

The architectural consequence is that Pay N Play has no account-creation step at the casino. The casino accepts the deposit, identifies the player from the bank-authenticated details, and creates the account on the fly. Payz requires both a wallet account and a casino account, with each maintained separately. Trustly skips registration friction; Payz adds account-management friction in exchange for the stored-balance flexibility.

Setup Friction

The Pay N Play story leans hard on this difference. A first-time visitor to a Trustly-enabled casino can deposit, play, and (in some implementations) withdraw without ever filling out a registration form. The bank authentication carries identity verification because the player’s identity is bound to the bank account. KYC happens through the open banking flow rather than as a separate step.

Payz first-time setup requires creating a wallet account (typically with ID verification at registration), funding the wallet, creating a casino account, and linking the two through the casino’s payment-method selection. The total time investment is perhaps 30 minutes spread across a couple of sessions. After that initial setup, both methods are similar in friction — Trustly authenticates per session via the bank, Payz authenticates via wallet password and 2FA — but the upfront friction profile is meaningfully different.

For players who use one or two specific operators consistently, the Payz setup amortises across many sessions and becomes invisible. For players who like to try new operators frequently — and the UK casino market structure encourages exploration, with the wider gambling sector serving 24.4 million active accounts on the most recent annual measurement — the Trustly model removes the per-operator setup cost entirely, and that advantage compounds across exploratory play patterns.

Speed and Fees in the Routine Case

Deposits process near-instantly through both methods. Trustly’s bank-to-casino transfer settles on the Faster Payments rail (or equivalent) and typically reflects in the casino balance within seconds of the bank authentication. Payz’s wallet-to-casino transfer is similarly fast. There is no meaningful speed difference at the deposit step.

Withdrawals diverge by implementation. Trustly’s withdrawal flow returns funds to the originating bank account directly, with timing dependent on the bank’s incoming-credit handling — often near-instant on Faster Payments. Payz’s withdrawal lands in the wallet first, with onward routing to a bank account as a separate user-initiated step. The two-step structure adds friction but also adds optionality: the funds sit in the wallet between the casino and the bank, and the player can spend them from the wallet, hold them, or move them onward at their discretion.

For pure speed of getting winnings back to a bank account, Trustly’s direct route is usually faster than Payz’s two-step route. For optionality of what to do with winnings once they leave the casino, Payz’s wallet-as-staging-area structure is more flexible.

On fees, Trustly itself charges no consumer-side fee on routine GBP transactions — the cost sits with the operator and the bank. Payz’s tier-dependent fee structure applies as discussed elsewhere, with the 2.99%-ish FX margin being the most relevant cost component for any non-GBP-native activity.

KYC and Privacy

Trustly’s KYC is inherited from the bank’s verification of the account holder. The casino does not run separate ID verification because the bank-authenticated identity satisfies the operator’s regulatory obligation. For UK players this is generally efficient — the bank has already done the work — but it does mean the operator sees identity information from the bank that a Payz-funded operator would not see directly.

Payz, as discussed, maintains its own KYC for wallet access and shares only minimal identity data with the operator when funding transactions. The casino runs its own KYC separately on the operator account, and the two verification chains are independent. This produces more administrative work upfront and more separation between the player’s identity at the wallet and the operator levels.

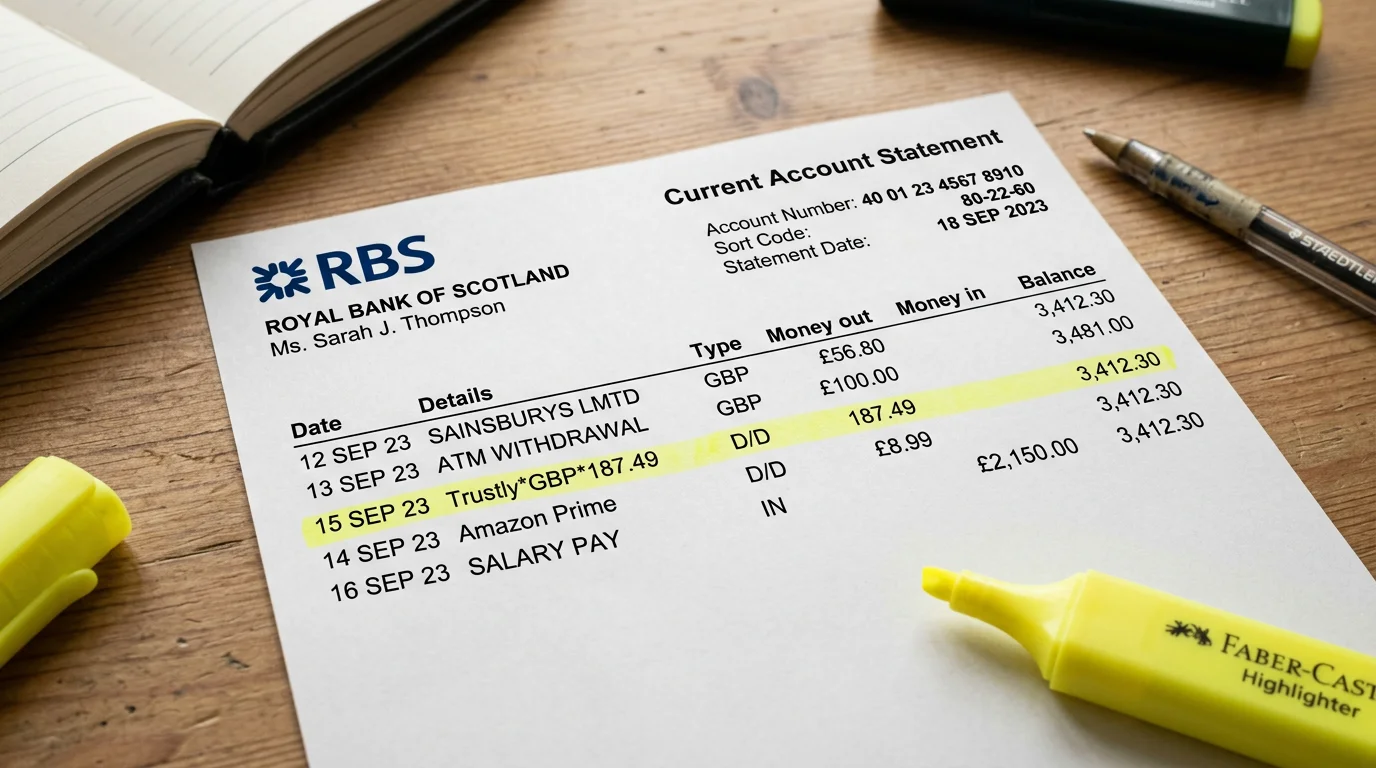

The bank statement story also diverges. Trustly transfers show on a bank statement with a Trustly-related descriptor and, depending on implementation, sometimes with the operator name visible in the line-item detail. Around 60% of UK online casino players still prefer debit cards for funding, partly because that descriptor visibility is familiar territory; open-banking-initiated transfers are less ambiguous on a statement than card payments are. Payz keeps the casino out of the statement descriptor entirely, with transfers showing as PSI-Pay e-money transactions. For descriptor privacy, Payz remains the cleaner option.

Where Each One Fits

Trustly Pay N Play wins for players who want minimal account-management overhead, value bank-to-bank speed on both directions, and play at a defined set of UK operators that support the integration. The setup friction is minimal, the flow is efficient, and the bank-rail withdrawal is genuinely fast. Players who treat casino payments as occasional rather than continuous benefit most from the no-account model.

Payz wins for players who value stored balance as a feature, want descriptor privacy on bank statements, use operators that may not support Trustly, or treat casino activity as a distinct financial silo that benefits from a separate account structure. The wallet’s role is broader than payment routing — it is a place to hold funds, manage cross-currency activity, and isolate gambling from everyday banking.

Many players I correspond with use both. Trustly for routine deposits at their primary operator where the bank-direct route is fastest; Payz for everything else — secondary operators, larger transactions where the wallet’s intermediate balance is useful, withdrawals where the wallet’s staging role matters. The two are complements rather than substitutes for players who want both efficiency and flexibility.

UK Coverage and Operator Support

Trustly’s UK casino coverage is narrower than Payz’s. Pay N Play is a specific integration that operators choose to implement, and adoption has concentrated at certain operators rather than spreading across the whole market. Payz support is near-universal at UK-licensed operators. For players who like to move between operators, Payz’s broader coverage matters; for players settled at one or two specific brands that support Trustly, the coverage gap may be irrelevant.

The coverage picture is changing slowly. Operators that have invested in open banking integration generally maintain Trustly alongside other payment methods; new operators in 2026 are increasingly launching with Trustly or equivalent open-banking-initiated options as part of their standard set. The gap between the two methods’ coverage at UK casinos is narrowing, but Payz retains the lead at smaller and specialist operators.

The Cashless-Payment Continuum

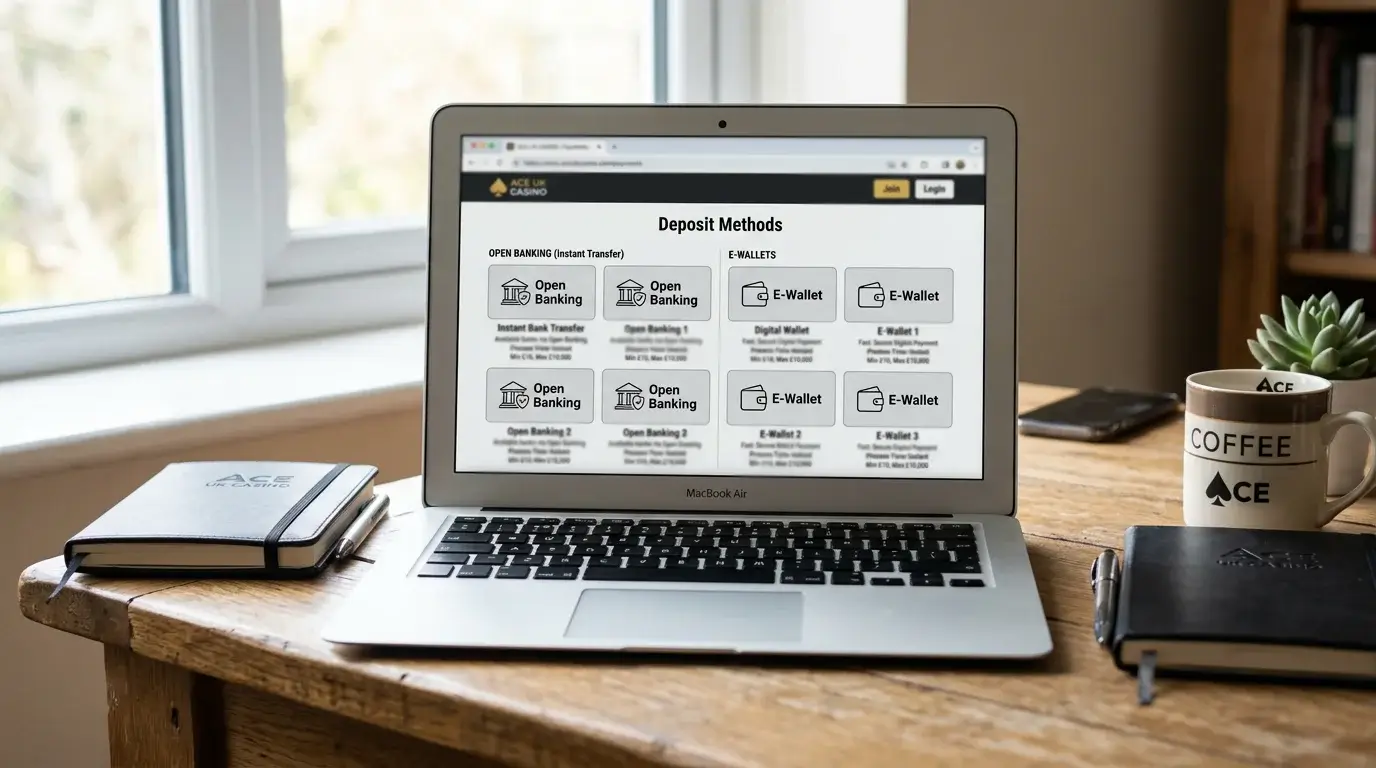

One useful framing: think of the UK casino payment landscape as a continuum from card-based instruments (debit card direct, Apple Pay, Google Pay) through stored-value e-money (Payz, Skrill, Neteller) to open-banking-initiated transfers (Trustly Pay N Play) to direct bank rail (Faster Payments at some operators). Each has its own friction profile, speed characteristics, privacy story, and operator coverage. Players who understand the continuum can pick deliberately for their situation rather than defaulting to whatever is on the operator’s payment-method dropdown.

The voucher-based end of the same continuum has its own dynamics. The comparison with Paysafecard covers the prepaid-voucher route in detail, which has yet another set of trade-offs (cash funding, no withdrawal, one-time use) that complement rather than directly compete with the other methods.

The Pragmatic Settled View

Trustly and Payz are not really competitors in the sense the comparison framing suggests. Trustly is a payment-initiation service that gives players a low-friction route from their bank to a casino. Payz is a stored-value wallet that gives players a managed account between their bank and any number of casinos. The two perform different functions, and the right pick depends on what the player wants the payment instrument to do — not on which one is generally “better”.

For UK players who care about both flexibility and efficiency, using both is the natural answer. For players who only need one and want a simple model, the choice falls out of how they think about their casino activity. Treat it as routine bank spending and Trustly fits. Treat it as a distinct financial silo and Payz fits. The architecture of each is honest about what it does, and the practical experience of UK casino play under each is genuinely different in ways that matter for the right players.

Prepared by the Paylobby editorial staff.