Instant ecoPayz Casino Deposits and UK Limits

The first time I watched a Payz deposit fail at a UK online casino, it was for a colleague who insisted everything was fine on his end. Funds in his Payz balance, account verified, casino licensed — every box ticked. The cashier still threw a soft decline, twice. We spent forty minutes tracing the rejection before we found it: the casino’s risk engine had flagged a mid-deposit currency switch that the player never noticed. Nine years of watching UK cashiers absorb new UKGC rules, I can tell you that more Payz deposits fail for reasons nobody explains than for reasons anyone publishes.

This walk-through is what I would hand a UK player who wants the Payz deposit flow demystified end to end. Not the marketing version — the cashier version. We will move through what you need before clicking deposit, the actual six-step sequence inside a UK-licensed casino, the maths on a £100 transfer, the limits that bite mid-session, the speed you can realistically expect, the five most common reasons a Payz deposit gets rejected, and the UK-specific rules that quietly shape every transaction in 2026.

Payz still runs on the same 256-bit SSL stack and PCI DSS-compliant infrastructure it inherited from the ecoPayz days, which means the security floor is high — but that floor is not the same thing as a smooth deposit. The smoothness comes from understanding the flow.

If you are looking to test a new platform with minimal risk, you can explore several £10 ecoPayz minimum deposit casinos available to British players.

Pre-Requisites for Using the Payz Casino Cashier

Skip a single prerequisite and you will spend the next twenty minutes wondering why a perfectly good wallet is being refused at a perfectly licensed casino. I have seen players blame the operator, blame Payz, blame the bank — when the root cause was usually a stale ID document or a name mismatch they had forgotten about.

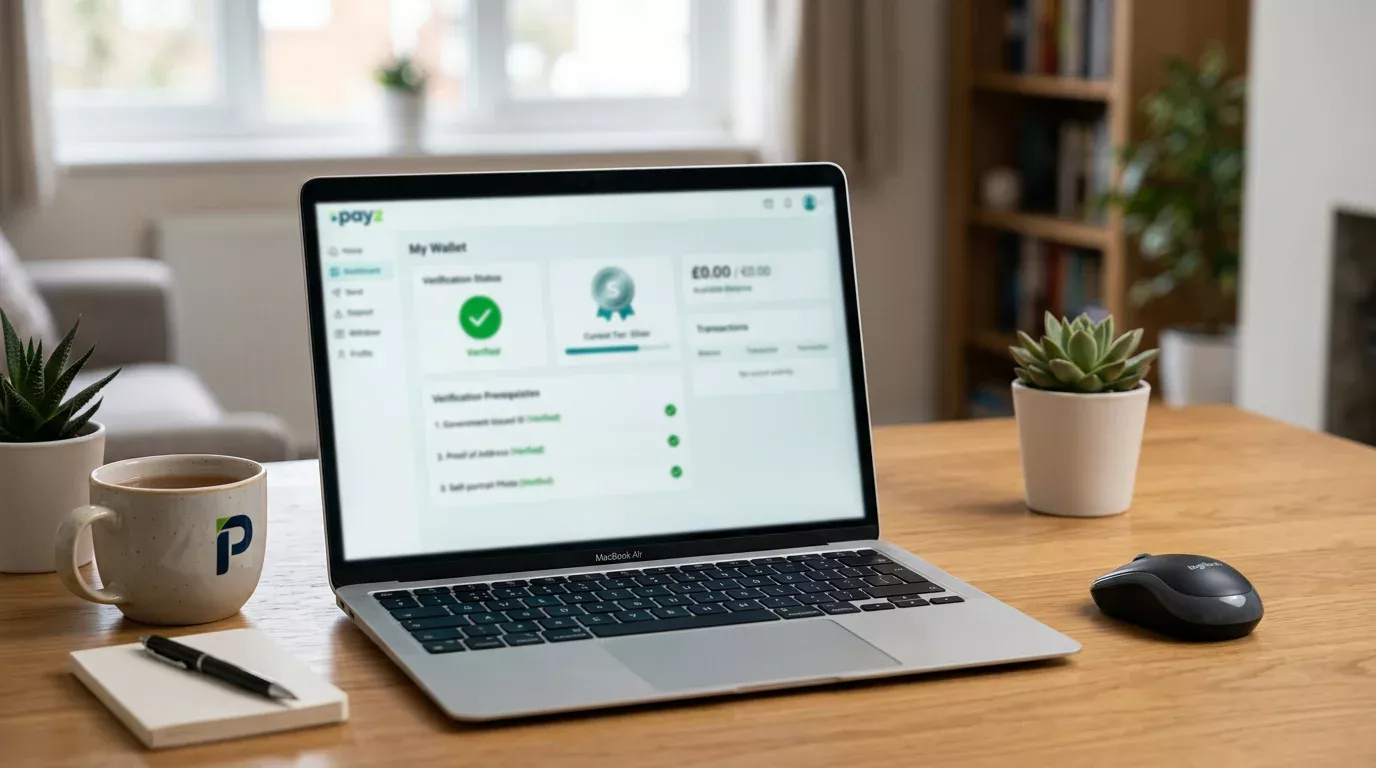

Before you load the cashier, four things need to be in working order. First, a fully verified Payz account at the tier you intend to use. Verification is not optional in the UK — PSI-Pay Ltd, the FCA-authorised entity that runs Payz, has to meet anti-money-laundering thresholds before it lets you move funds outbound, and a gambling operator counts as outbound. Second, a funded Payz balance in the currency the casino will actually charge. The cleanest setup is GBP-to-GBP — your Payz balance in pounds, the casino game in pounds. Anything else triggers a conversion, which I will come back to.

Third, a casino account that already passed the operator’s own KYC for at least one document. A first deposit on a brand-new account will trigger an extra layer of identity matching between Payz and the cashier; if the name on your Payz wallet differs by even a middle initial from the name on your casino registration, expect a manual review. Fourth — and this is the one nobody talks about — your casino account needs to be on a tier where Payz is a permitted method. Some UK operators restrict e-wallets on accounts under thirty days old, especially for first-time depositors. The cashier will silently grey out the Payz logo without explaining why.

If the wallet setup itself is what is holding you back, the end-to-end Payz casino sign-up flow covers the onboarding side in proper depth.

Six Steps From Cashier Click to Balance Update

Every UK Payz deposit I have ever traced — including the messy ones — fits inside the same six-step skeleton. The differences between operators are cosmetic. The differences between successful and failed deposits live in steps three and five.

Step one is selection. You open the casino cashier, switch to the deposit tab, and pick “Payz” from the methods grid. At many UK-licensed sites the label still reads “ecoPayz” or “ecoPayz/Payz” — the brand change in May 2023 did not force every operator to update their cashier graphics, and the underlying entity (PSI-Pay Ltd, FCA-regulated, present across 174 countries) has not changed. Treat both labels as the same rail.

Step two is amount entry. The cashier asks how much you want to deposit. This is where the operator may surface a minimum and a maximum specific to Payz, and these are almost never the same as the debit-card minimums. I will dig into the ranges in a moment; the point at step two is that you are committing to a figure before any wallet handshake has happened.

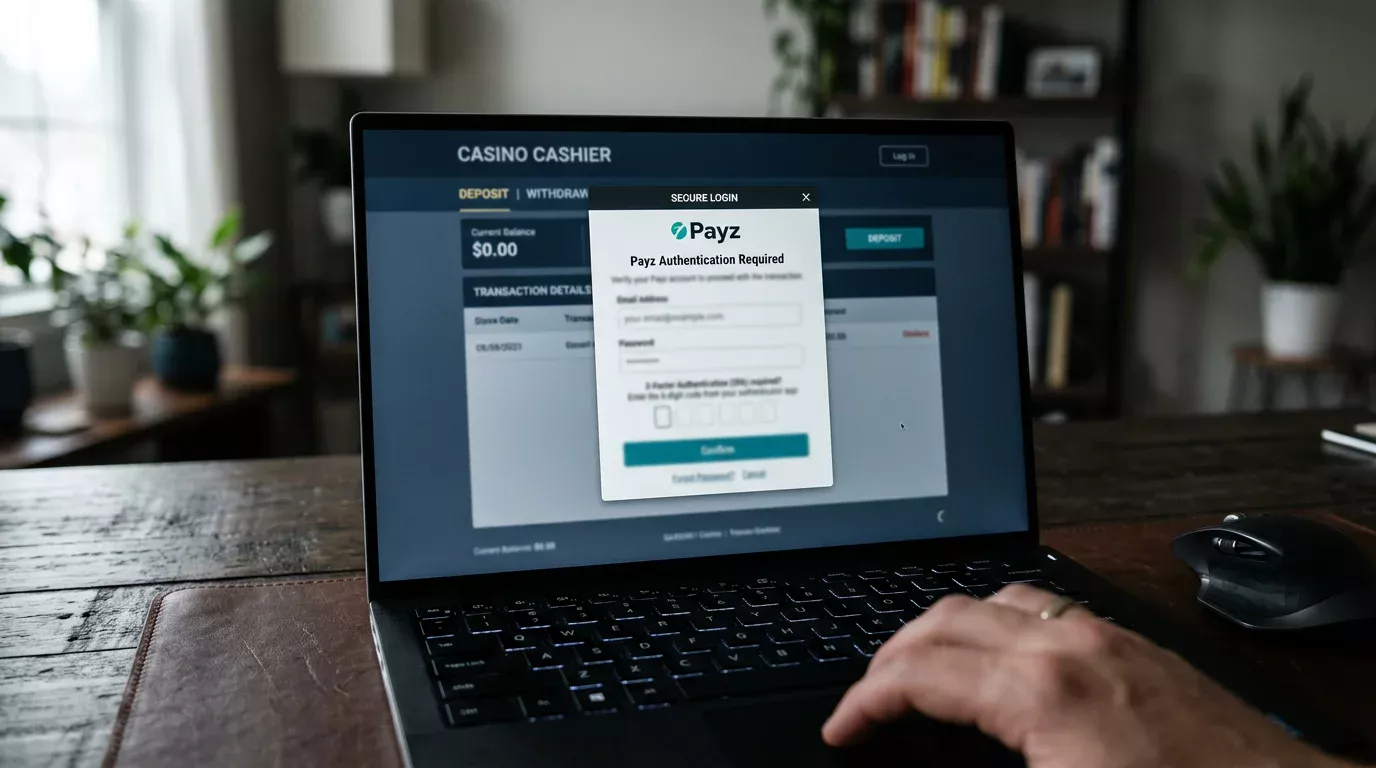

Step three is the handover. You click “Continue” or “Deposit” and the casino redirects you to the Payz authentication page or pops a Payz overlay. This is where Payz takes control. You enter your Payz email and password, complete 2FA if you have it enabled, and confirm the transaction against the merchant ID the cashier has provided. The 2FA prompt is the security floor I mentioned at the start — 256-bit SSL on the connection, PCI DSS on PSI-Pay’s side, plus your second factor on top. If anything is going to go wrong silently, it usually goes wrong here.

Step four is the Payz balance debit. The moment you confirm, Payz debits your wallet balance and creates a transaction reference. You will see it in your Payz transaction log immediately. The money is gone from your wallet — but it has not yet arrived at the casino.

Step five is the casino credit. Payz pushes a confirmation message back to the operator. The casino’s payment gateway receives it, validates the amount and reference against the request it logged in step two, and credits your playable balance. On a clean transaction this happens in under five seconds. On a flagged one, it can take minutes or hours.

Step six is the audit trail. The casino writes the deposit to its UKGC reporting log — the operator is required to retain transactional records for the Commission’s affordability and AML monitoring — and the funds become wagerable. Step six is invisible to you, but it is the step that converts a Payz transfer into a live casino balance you can actually stake.

£100 Deposit: What Actually Moves

Let me run a concrete £100 deposit through that flow so the abstractions land. Assume you are a UK player with a verified Silver-tier Payz account, GBP balance, depositing at a UKGC-licensed casino whose game lobby runs in GBP. No currency conversion. No bonus claim.

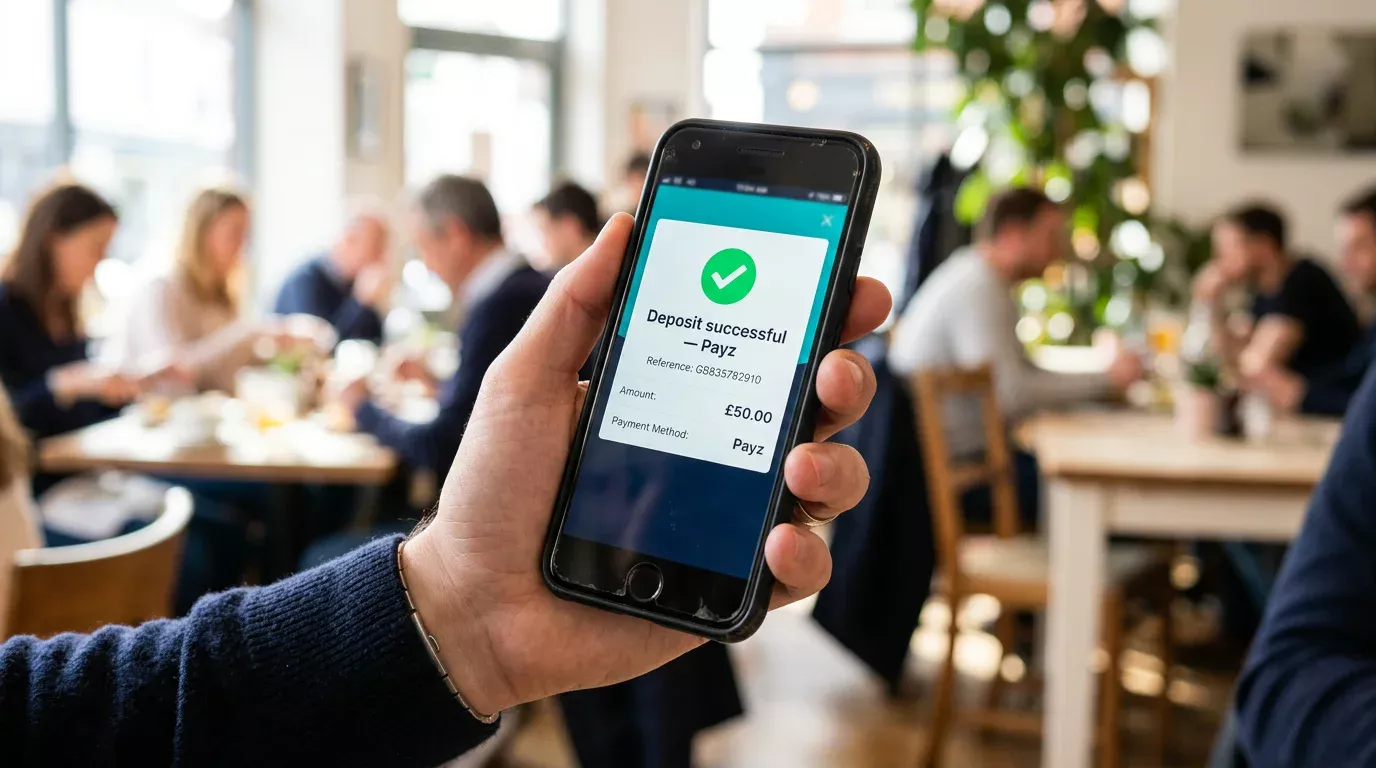

At step one you select Payz. At step two you enter £100 — well inside the typical UK Payz minimum of £10 and the typical maximum of around £5,000 per transaction. At step three the Payz overlay loads, you log in, and you approve. The transaction reference appears in your Payz log instantly: a debit of £100.00 GBP, merchant identifier matching the casino’s settlement entity, status “completed”.

At step four, your Payz wallet balance drops by exactly £100. There is no Payz-side fee on the deposit leg for UK-to-UK GBP transactions — Payz monetises mostly on currency conversion, on certain withdrawal routes, and on dormancy, not on standard inbound merchant payments. The £100 leaves your wallet whole.

At step five, the casino credits your playable balance with £100. The cashier confirmation reads “Deposit successful — Payz — £100.00”. Elapsed time from clicking “Deposit” to seeing the balance update: typically four to nine seconds on a clean transaction. Step six writes it to the operator’s UKGC log behind the scenes. You see nothing — that is the design.

The maths is clean precisely because the currency was clean. Slot a euro-denominated casino in the middle of that sequence and Payz adds a 2.99% conversion margin on top of the mid-market rate, and the same £100 becomes a smaller real number on the other side.

Deposit Ranges and Caps at UK Payz Cashiers

Operators publish their Payz minimums and maximums, but rarely in one place and almost never with an explanation. I have catalogued them across thirty-odd UK-licensed cashiers over the years, and the band is narrower than it looks.

On the minimum side, the modal figure I see at UKGC-licensed casinos is £10 for Payz deposits. Some operators run £5 minimums for everything except e-wallets — the deposit method affects the floor because the operator absorbs a small processing cost on each transaction, and e-wallets are not as cheap to process as a debit card. A handful of casinos push the Payz minimum to £20, usually older brands with simpler cashier engines.

On the maximum side, the picture is more elastic. Standard Payz per-transaction caps at UK casinos sit somewhere between £2,500 and £5,000, with the higher end common at brands targeting mid-roller play. For context, Skrill — the closest e-wallet competitor in the UK — publishes maximum casino deposits up to £20,000, which gives you a sense of how the bigger ecosystem is structured around mid-to-high spenders.

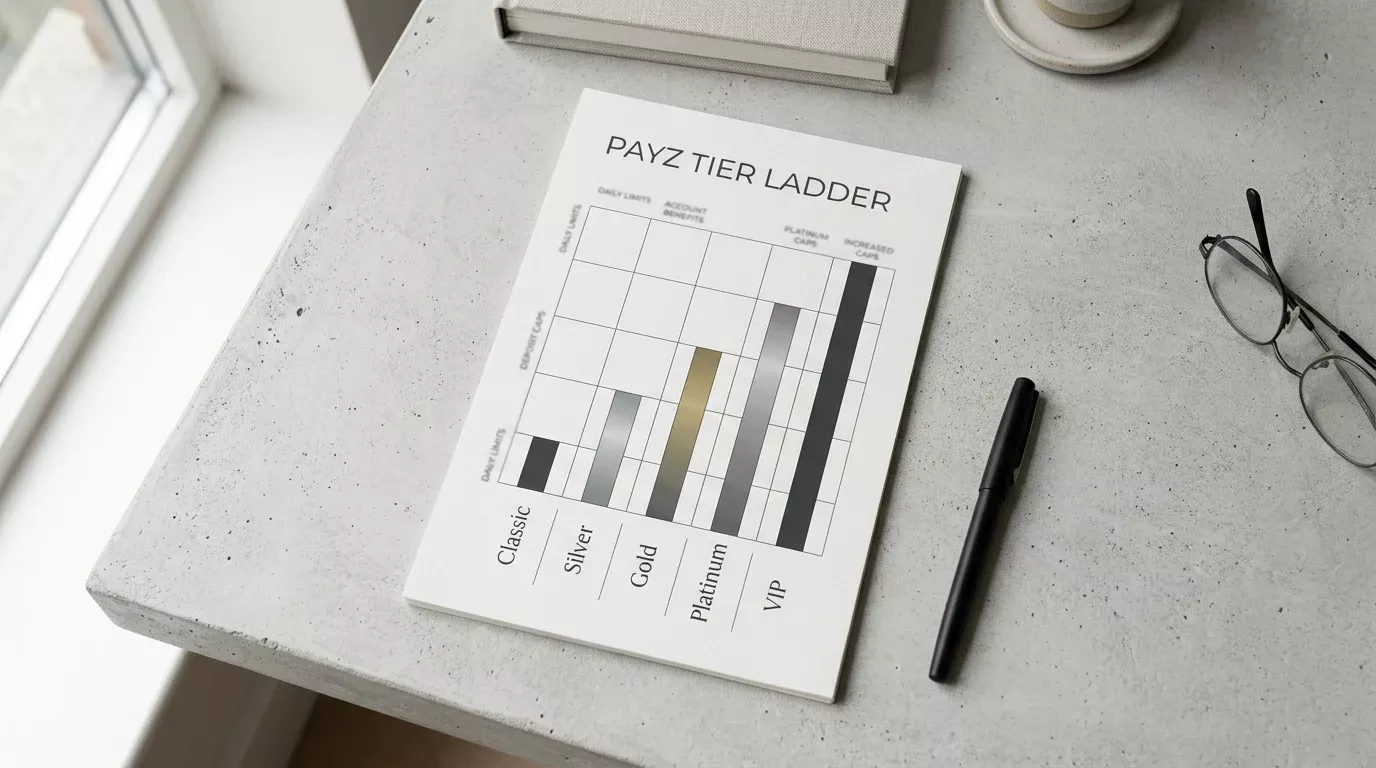

Payz’s own tier system layers another cap on top. A Classic-tier account has lower monthly throughput than a Gold or VIP tier; the casino’s per-transaction max is irrelevant if your wallet is throttling you at the source. If you regularly deposit above £1,000 a month and have not upgraded past Classic, the cap that bites first will be Payz’s, not the operator’s.

One quirk I always flag: some UK cashiers apply different caps to first deposits than to subsequent ones. The first Payz transaction on a new casino account is often capped at a few hundred pounds, lifted automatically after KYC and the first successful settlement. This is risk management, not a bug.

How Fast a Payz Deposit Lands: Instant vs Delayed

“Instant” is one of those words the gambling industry abuses until it means almost nothing. Payz deposits at UK casinos are usually fast, but the variability is wider than the marketing implies, and the slow ones are not always failures.

On a healthy transaction with a verified account at a UKGC-licensed cashier, the Payz balance debit and the casino balance credit happen within the same five-to-ten-second window. The handshake is API-level — Payz pushes a structured confirmation to the operator’s payment gateway, the gateway acknowledges, and the player’s playable balance updates. There is no clearing window because no clearing house is involved; the funds are e-money moving between two regulated entities.

What slows things down is everything happening around the handshake. A first deposit on a new casino account adds a name-match check, sometimes adds an enhanced KYC trigger, and often introduces a thirty-to-ninety second pending state while the operator’s risk engine looks at the transaction. A mid-session deposit on an established account is usually clean. A deposit just after you triggered a UKGC affordability check is not — and the broader market context here matters, because Apple Pay and Google Pay deposits at UK casinos have grown roughly 47% year on year, putting more competitive pressure on legacy e-wallets like Payz to keep their handshake times under five seconds.

The realistic expectation: under ten seconds end to end on a clean deposit, up to a minute or two if any flag fires, longer than that only if something needs human review.

When the Cashier Rejects a Payz Deposit: Five Common Causes

Five causes account for roughly nine in ten Payz deposit rejections I have seen at UK cashiers. Going through them in rough order of frequency saves time.

The first is funding-source contamination. UK law has banned gambling on credit cards since April 2020, including indirectly through e-wallets — and that “indirectly” is the operative word. If your Payz balance was topped up from a credit card, even partially, the cashier may refuse the deposit at the casino end as a precaution, because the operator does not want a single penny of credit-funded money landing on its game balance. The fix is to top your Payz wallet only from debit cards, bank transfers, or other non-credit rails.

The second is name and address mismatch. Payz holds one identity record; the casino holds another. If the two disagree on the spelling of your surname, on whether you have a middle name, on your registered address, or on your date of birth, the cashier’s risk engine throws a decline. The fix is administrative: update one side to match the other, and contact support to reconcile.

The third is the tier cap. Classic Payz accounts have lower monthly throughput than the upper tiers, and if you have hit your monthly outbound limit, the next deposit will simply fail at the Payz overlay with a generic error. The fix is to wait until the next billing cycle or upgrade your tier.

The fourth is the operator’s per-method first-deposit cap. As I mentioned earlier, many UK casinos cap the first Payz transaction at a few hundred pounds. You enter £1,000, the cashier accepts the input, hands over to Payz, and the casino-side gateway rejects on return. Confusing, because the rejection looks like a wallet failure but is actually an operator policy.

The fifth is an in-flight UKGC affordability flag. If your deposit pattern in the last thirty days has approached or crossed the £150 financial vulnerability threshold, the operator may pause the next deposit until you provide documentation. This is not a Payz problem — it is a casino-side regulatory gate, and it will fire regardless of which payment method you choose. I will come back to it.

UK-Specific Rules That Touch Every Payz Deposit

Three pieces of UK regulation now touch every Payz deposit at a UKGC-licensed casino, and not knowing about them is the most common reason players think their wallet is broken when it is actually behaving exactly as designed.

The first is the financial vulnerability check threshold, which dropped from £500 to £150 over any thirty-day rolling period on 28 February 2025. The Commission’s chief executive Andrew Rhodes put it in straightforward terms when he addressed the BGC AGM the day before the switch — tomorrow, he said, financial vulnerability thresholds fall to £150 per thirty-day rolling period, and the pilot for full Financial Risk Assessments is well advanced. What that means in practice: if your cumulative deposits across a UKGC-licensed casino approach £150 within thirty days, the operator’s risk engine starts looking for public-data signals that you can afford the spending, and on cleared customers 97% of those checks now run frictionlessly. The remaining 3% involve a request for documentation. Payz cannot bypass this — the check is operator-side and method-agnostic.

The second is the slot stake limit. From 9 April 2025 the maximum stake per spin on an online slot for adults is £5, and from 21 May 2025 it dropped to £2 for players aged 18 to 24. The stake limit is not a deposit limit, and the distinction matters. You can deposit £200 via Payz and that £200 sits in your playable balance untouched — but you cannot spin a single slot at more than £5 per spin, regardless of how the balance got there. Players sometimes assume the cashier should be smaller because the per-spin cap is smaller. It should not. The deposit is independent.

The third is the legacy credit-card ban from April 2020. Players still occasionally try to fund Payz from a credit card and then deposit at a casino through Payz; the cashier-side controls catch this. The Commission has been clear, including in Rhodes’s framing of the balance between protecting people and respecting adult freedom — the rules exist, they are enforced, and the e-wallet rail is not a workaround.

Before funding your account, always compare the terms offered by the top Payz casino sites to find the best match for your bankroll.

Deposit-Side Takeaways for UK Payz Users

Three years of UK regulatory tightening has changed what a “normal” Payz deposit looks like at a UKGC-licensed casino. The wallet itself is largely the same — same FCA-authorised entity, same 256-bit SSL floor, same six-step flow from cashier click to balance update — but the operator-side gates that sit around the transaction have become busier, more frequent and harder to ignore.

The practical implication for any UK player is that the smooth deposits are the ones where the prep work happened off the cashier screen. Verified Payz account at the correct tier. GBP balance funded from a non-credit source. Casino account that already cleared at least one KYC step. Currency aligned with the operator’s lobby. Awareness that the £150 vulnerability threshold and the £5 slot stake limit live in the background of every session and will surface on cue, not on convenience.

The Payz rail is genuinely fast when those pieces are in order, and genuinely opaque when they are not. The opacity is not an accident — it is the same regulatory architecture that protects you from credit-funded losses and from undetected affordability drift, just experienced from the wrong side of the cashier. Treat the gates as features, not faults, and the deposit experience evens out.

Created by the "Paylobby" editorial team.