Safe ecoPayz Casino Platforms and FCA Rules

“Is Payz safe?” is the question I get asked most often, and it is the question with the worst standard answer. Every review you will read says yes, gives you a paragraph about SSL encryption, mentions PSI-Pay’s FCA registration once, and stops. Nine years of working through this layer has convinced me that the standard answer is technically true and practically useless, because it answers the wrong question. The right question is not whether the wallet is safe. The right question is what “safe” means at each layer of the stack — and where the protection genuinely stops.

The honest version has four layers. The wallet itself, sitting under PSI-Pay’s FCA authorisation. The technical floor of 256-bit SSL encryption, PCI DSS compliance and 2FA that protects the payment instructions in transit. The UKGC layer that sits on top of the operator side of the transaction. And the broader environmental risk of using any wallet, including Payz, outside a UKGC-licensed estate.

This is not a reassurance piece. It is an audit. I walk through each protection layer in turn, with the regulatory references behind it, the limits of what it covers, and the gaps where players still get hurt — including the gap that has been widening fastest in 2026, which is the gap between regulated and unregulated operators using the same wallet brand. Nothing in this article is meant to scare anyone away from Payz. It is meant to give you an accurate map of where the protection actually sits.

For an added layer of security against unauthorized access, setting up ecoPayz 2FA is highly recommended before making large transactions.

FCA Mandates and PSI-Pay Ltd Regulatory Scope

Authorisation language is where every Payz safety claim either earns its keep or quietly overstates its case. The substance is real, but the substance is more specific than the marketing makes it sound.

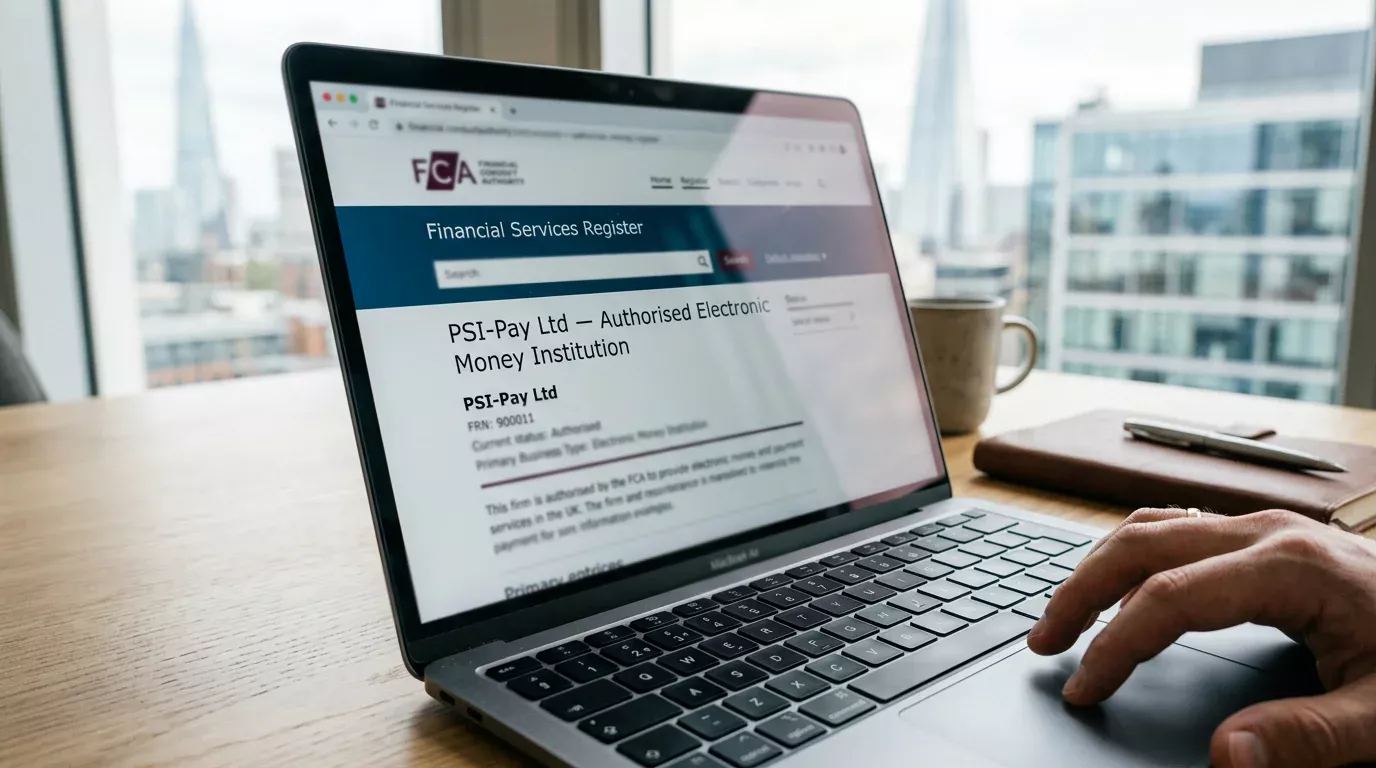

PSI-Pay Ltd is the legal entity behind Payz. It is authorised by the Financial Conduct Authority as an electronic money institution under the Electronic Money Regulations 2011, and dual-regulated by the Central Bank of Cyprus for its wider European footprint. PSI-Pay has held its regulatory permissions for over fifteen years and Payz operates across 174 countries — meaning the wallet sits inside one of the most established e-money frameworks available on the UK iGaming circuit.

What FCA authorisation covers is specific and worth knowing. It covers PSI-Pay’s permission to issue electronic money in the UK. It covers the company’s obligation to safeguard customer funds in segregated accounts. It covers ongoing capital adequacy. It covers anti-money-laundering duties including customer due diligence, transaction monitoring and suspicious-activity reporting. It covers complaints-handling standards and the right of UK customers to escalate disputes to the Financial Ombudsman Service.

What it does not cover is what people often assume it does. It does not cover the underlying casino transaction — that is the UKGC’s remit, not the FCA’s. It does not cover gambling losses; the wallet’s regulation says nothing about whether the money you transferred was wisely spent at the cashier. It does not entitle you to a chargeback in the Visa or Mastercard sense, because PSI-Pay is not a card scheme. And it does not extend to Financial Services Compensation Scheme cover for your wallet balance in the way bank deposits are covered, which I will come back to.

The takeaway: FCA authorisation gives you a regulated counterparty, a complaints route, and a safeguarding obligation on your funds. It does not give you bank-equivalent protection on every dimension of the relationship. Payz is genuinely regulated. It is not, however, a bank.

How Your Payz Balance Is Safeguarded If PSI-Pay Fails

The single question that determines whether your Payz balance survives a corporate failure is whether the wallet’s parent has properly safeguarded customer funds. The answer for PSI-Pay is yes — but the mechanism is different from what most players expect.

Under FCA rules for electronic money institutions, PSI-Pay must hold customer funds in segregated accounts at credit institutions or invest them in low-risk secure assets. The funds are legally ring-fenced from PSI-Pay’s own corporate assets, which means in the event of insolvency, customer balances are not part of the general pool available to creditors. They are returned to customers, subject to the administration process, ahead of unsecured creditor claims.

This is structurally different from the Financial Services Compensation Scheme that protects bank deposits up to £85,000. The FSCS does not cover e-money institutions in the same way it covers banks. If PSI-Pay failed tomorrow, the recovery process for your Payz balance would run through the safeguarding rules and the FCA’s wind-down framework, not through the FSCS. In practice this has worked: when other UK-authorised e-money institutions have failed in recent years, customer funds have been returned, though with delays measured in weeks or months rather than the FSCS’s typical days.

The practical implication for any UK Payz user is straightforward. Do not treat your Payz wallet as a substitute for a current account. Keep the balance you need for active casino play, and move funds back to a fully bank-deposit-protected account when you are not playing. The PSI-Pay infrastructure built around the wallet — the FCA authorisation, the segregated accounts, the 174-country operating footprint — is robust, but the protection model is not bank-equivalent, and a wallet is the wrong place to hold standby cash.

Encryption, 2FA and the Technical Floor for a Casino E-Wallet

The technical floor under Payz is good, and good in ways that are documented rather than asserted. The wallet runs on 256-bit SSL encryption for all data in transit, and PSI-Pay maintains PCI DSS compliance on the payment-card data infrastructure. Both standards are industry baselines for payments — not unusually strong, but unambiguously sufficient for the use case.

What 256-bit SSL covers is the conversation between your device and Payz’s servers. The session is encrypted such that even if traffic were intercepted in transit, the captured packets would not yield readable payment instructions. This is the same protection a bank’s online portal applies to its login session. It does not protect against compromise of your device itself — keystroke logging, screen scraping, browser-extension hijacking — only against interception in transit.

What PCI DSS covers is the handling of card data on PSI-Pay’s infrastructure. The standard specifies how card numbers are stored, who can access them, how the network is segmented, how logs are kept, and how the whole stack is audited annually by an independent assessor. PCI DSS is mandatory for any entity that handles card data at scale; PSI-Pay’s compliance is a precondition of operating, not a value-add.

The 2FA layer is where the user-controlled protection lives. Payz supports authenticator-app 2FA (TOTP codes), SMS-based 2FA, and push notification approval on the mobile app. The strength of these varies — authenticator apps are the most resistant to attack, SMS the weakest because of SIM-swap risk. The casino-side does not control which 2FA method you use; that is configured in your Payz account settings.

The Payz-specific configuration of 2FA, including how to enable it on a UK casino account and the recovery flow if your second factor is lost, sits in the dedicated walkthrough on setting up ecoPayz 2FA at online casinos.

Three Authentication Layers Between Payz and a UK Cashier

From the moment you click “Deposit” at a UK casino cashier to the moment your playable balance updates, three authentication layers sit between you and your money — and understanding them helps explain why “Payz security” is not a single thing.

The first layer is the casino’s own login. You authenticated to the operator before you reached the cashier; the session token in your browser confirms your identity to the casino’s payment gateway. The second layer is the Payz authentication that fires when the cashier hands over to the Payz overlay. You log into Payz directly, separately from the casino, and you confirm the transaction against a merchant ID that the cashier passed across. The third layer is the 2FA challenge — if you have it enabled — which adds a one-time code or push approval before the wallet releases funds.

All three layers can fail independently. A compromised casino account does not give an attacker access to your Payz wallet, because the Payz layer requires its own credentials. A compromised Payz account does not by itself drain funds if 2FA is enabled, because the third layer blocks the release. The redundancy is the protection.

Where UKGC Adds Protection on Top of FCA

FCA authorisation covers the wallet. UKGC licensing covers the casino. Both have to be in place for the protection model to function — and at a UKGC-licensed operator, the Commission adds layers the FCA does not.

The UKGC layer covers things FCA authorisation has nothing to do with: the integrity of the games themselves, the operator’s responsible-gambling obligations, the affordability and vulnerability checks that pause large or unusual deposit patterns, the right to use the GAMSTOP self-exclusion scheme, the complaints route through accredited Alternative Dispute Resolution providers, and the operator’s duty to retain transactional records for regulatory inspection. None of these are wallet functions. All of them rely on the operator being properly licensed.

The Commission has been busy on the enforcement side. The most recent reporting cycle saw 741 cease-and-desist notices issued to illegal operators, and around 398,000 illegal URLs passed to search engines, of which roughly 267,000 were removed from indexes. The Commission’s chief executive Andrew Rhodes has framed the broader regulatory mission in language that captures the balancing act — there is a responsibility, he has said, to get the balance right between protecting people from the potentially life-ruining effects of gambling-related harm and respecting the freedom of adults.

That balance is what the UKGC layer is built around. The £150 financial vulnerability threshold, the £5 stake limit on adult slots, the £2 stake limit for 18-to-24-year-olds, the ban on reverse withdrawals, the prohibition on credit-card-funded deposits including via e-wallets — all of these are operator-side rules the wallet itself cannot enforce or bypass.

The practical implication is the most important sentence in this article: a Payz wallet at a UKGC-licensed casino is protected by both regulatory frameworks. A Payz wallet at an unlicensed casino is protected only by the wallet’s own layer, which does not include any of the gambling-specific protections. The wallet brand on the cashier means very little if the cashier itself is outside the regulated estate.

The Black-Market Risk: Why a Payz Casino Off UKGC Is Not Safe at All

This is the section that the standard “is Payz safe?” review skips, and it is the one that matters most in 2026. The wallet does not protect you from playing at the wrong cashier. The wrong cashier is increasingly easy to find.

The UK offshore unregulated gambling market reached £16.6 billion in 2025, up from around £5 billion in 2019 — a rise of more than 230% in six years. Channelisation, the share of UK gambling activity occurring on regulated operators, has dropped from 97% in 2019 to 92% in 2025. The trend line is in one direction.

Yield Sec, the integrity-monitoring firm operating as Gaming Compliance International, has tracked the illegal-operator share of UK online gambling rising from 0.43% in 2020 to around 9% in the first half of 2025, with the addressable value put at £379 million. Ismail Vali, the GCI president, has not minced words about who the illegal operators are targeting — illegal online gambling in Great Britain, he has said, is now knocking on the door of 10% market share, and it has achieved this through the cynical exploitation of two vulnerable audiences, children and self-excluded gamblers on the GAMSTOP scheme.

What this means for Payz users specifically is that some operators outside the UKGC regulated estate accept Payz, or claim to. The wallet brand at the cashier does not validate the operator. An illegal site can display the Payz logo, accept a deposit through the wallet’s standard API, and operate entirely outside UK gambling regulation. The wallet’s transaction will succeed; the wallet’s safeguarding obligations will continue to apply to your balance; but the gambling-side protections — the affordability gate, the GAMSTOP integration, the dispute route through ADR providers, the assurance of game integrity — none of those exist at an unlicensed site.

The check that matters is simple and free: any UK-licensed casino displays its UKGC operating licence number in the footer, and the Commission’s public register lets you verify it. If the licence number is missing, unverifiable, or for a different entity than the cashier you are using, you are outside the regulated estate. The wallet is safe; the cashier is not.

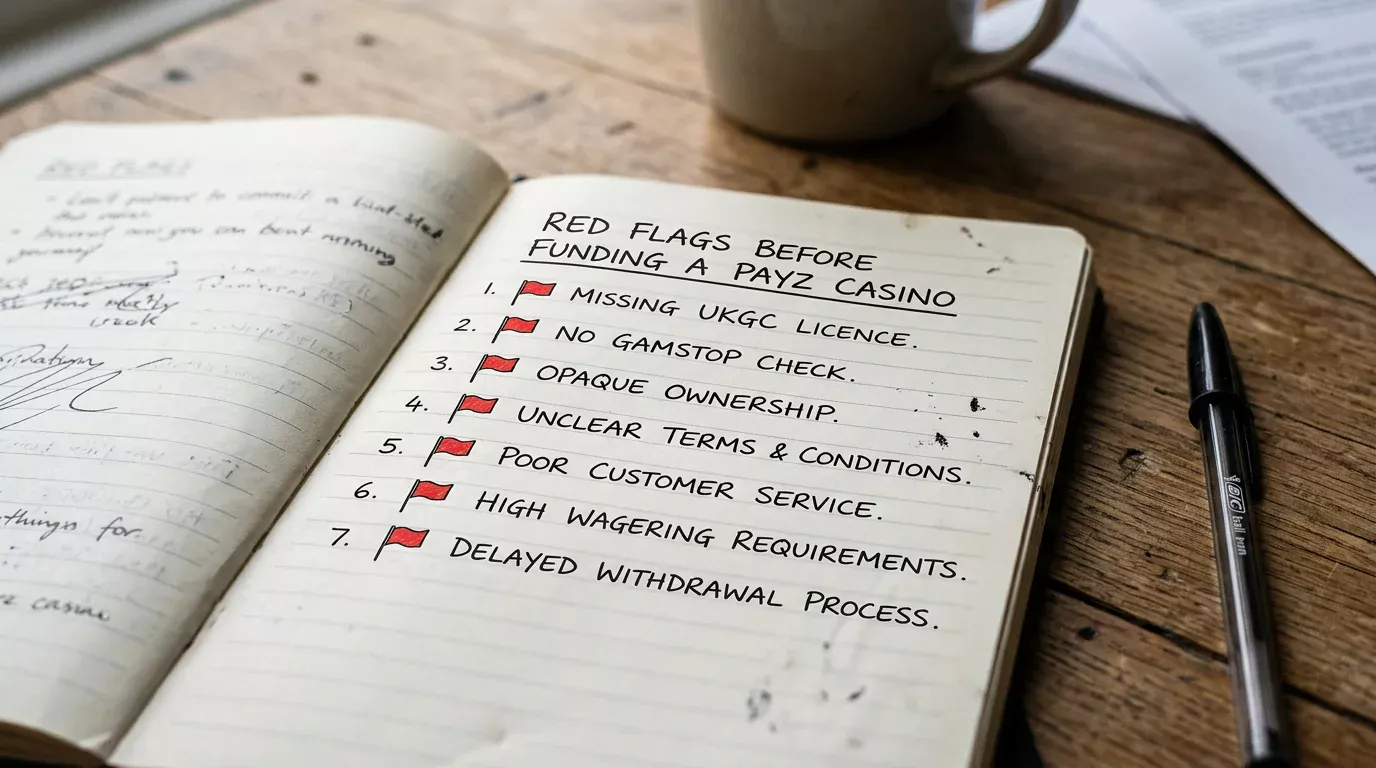

Seven Red Flags Before You Fund a Payz Casino Account

The pattern of unsafe Payz casino interactions repeats itself. After working through enough of them, the warning signs have become almost mechanical to spot. Seven flags catch most of the bad outcomes before they happen.

The first flag is a missing or unverifiable UKGC licence number. The footer of any legitimate UK casino names the operating licensee and shows the licence reference. If the number is absent, or it traces back to a different company than the one running the cashier, the site is not properly licensed for UK customers.

The second flag is aggressive bonus claims that contradict UKGC advertising rules. Welcome offers above what the regulated estate typically permits, vague wagering terms, or “no verification needed” claims are markers of an operator deliberately positioning outside the regulated framework.

The third flag is missing GAMSTOP integration. Every UKGC-licensed remote operator must integrate with GAMSTOP. A casino that does not check your GAMSTOP status during registration is, definitionally, not UKGC-licensed for remote operations.

The fourth flag is a Payz logo without other UK-recognised methods. Legitimate UK operators offer debit cards, bank transfers and one or two of the major e-wallets. A cashier that lists only e-wallets and cryptocurrency is structured to avoid mainstream regulatory scrutiny.

The fifth flag is opaque ownership. UK operators publish the operating entity, the corporate group, and the licence holder. A site that hides this information in footer fine print or refuses to disclose it is concealing something material.

The sixth flag is no published complaints route through an ADR provider. UKGC-licensed operators must name an accredited dispute-resolution body in their terms. Its absence is a tell.

The seventh flag is the unsolicited approach. Cold emails, social-media direct messages, and influencer-driven referrals to obscure casinos accepting Payz are overwhelmingly leads for illegal operators.

Spotting one flag in isolation is not always conclusive. Spotting two or more is.

Safe Under Conditions: A Balanced Verdict

Pulling all four layers together, the honest verdict on Payz safety at UK casinos is conditional rather than absolute. The wallet itself, sitting under PSI-Pay’s FCA authorisation with 256-bit SSL, PCI DSS compliance and proper safeguarding of customer funds, is solidly built. The technical floor is good. The regulatory floor is real. The 174-country operating footprint and the fifteen-plus years of continuous authorisation give PSI-Pay a track record that compares well against any specialist e-wallet on the UK iGaming circuit.

Your funds remain protected as long as you choose fully licensed and secure Payz gambling platforms regulated by the UKGC.

What conditions the verdict is everything that sits outside the wallet’s own perimeter. Your balance is safeguarded but not FSCS-covered, which means the wallet is the wrong place to hold standby cash. Your transaction is encrypted and authenticated but the protection depends on your own 2FA setup and device hygiene. And — most importantly — the regulatory framework that makes the casino half of the transaction safe is UKGC-licensed operation, not Payz. The wallet brand at the cashier is not a substitute for the operator’s licence.

The frame I would give any UK player is to think about safety as a chain rather than a property. The chain is: regulated wallet, encrypted handshake, authenticated transaction, licensed operator, supervised conduct. Each link is necessary. Payz contributes three of the five — the wallet, the encryption, the authentication. The operator and the regulator have to provide the other two. Get all five, and the protection is genuine. Miss any one, and the strength of the others is irrelevant.

Written by the editors at Paylobby.