Prepaid ecoVirtualcard Use at UK Casino cashiers

The eco-Virtualcard is one of the most misunderstood features of the Payz wallet, and the misunderstanding is dangerous because it touches the UK credit card gambling ban. Half the readers who ask me about it think it is a credit card. The other half think it is a way to deposit at operators that do not list Payz directly. Neither view is quite right, and the gap between the two has caused some genuinely problematic transactions over the years.

The accurate description is technical but matters. An eco-Virtualcard is a single-use, prepaid Mastercard number generated from your Payz wallet balance. It functions exactly like a Mastercard at any merchant that accepts Mastercard, with the funds debited from your Payz wallet at the moment of use. It is not a credit card, it is not a debit card linked to a bank, and it does not extend you credit. Let me unpack what that means for UK casino play.

Eco-Virtualcard Structural Features and Purpose

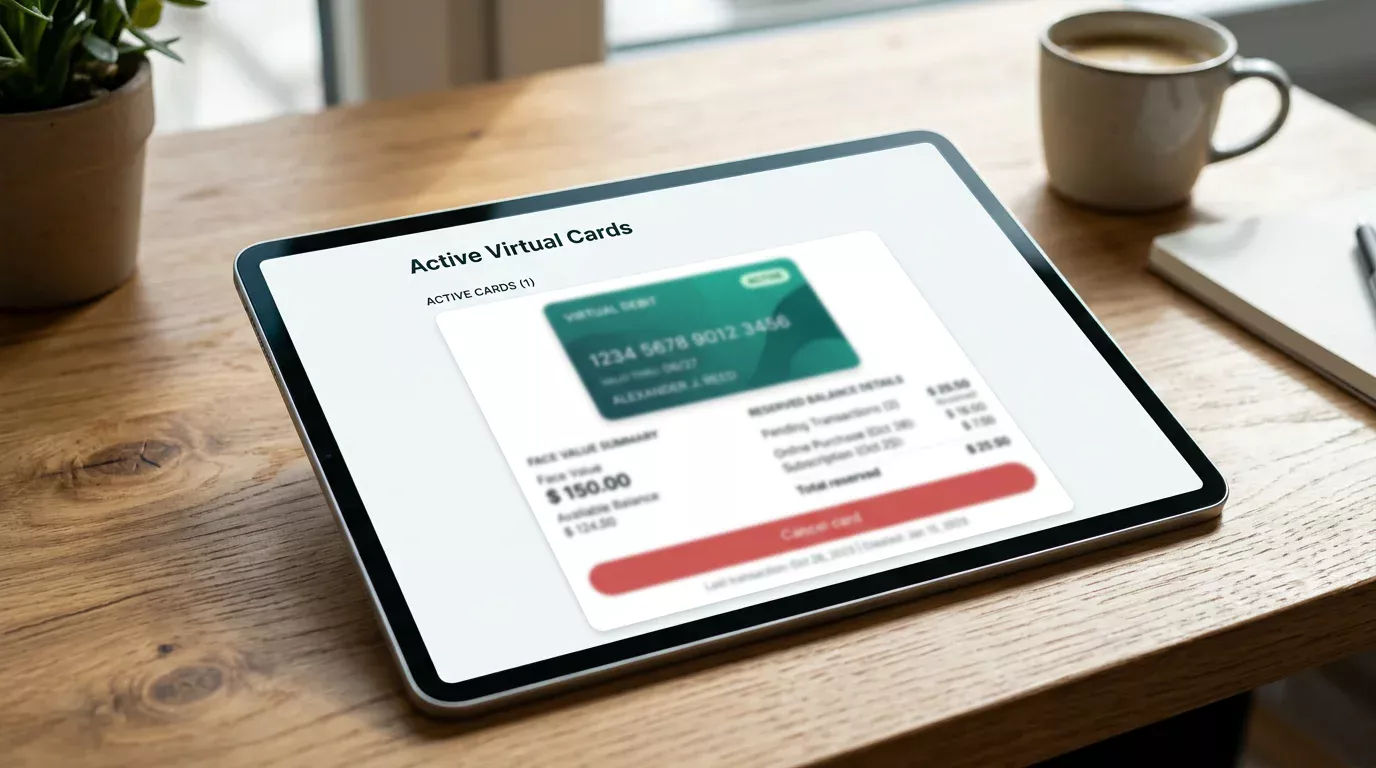

Generate an eco-Virtualcard from inside your Payz wallet and you get a 16-digit Mastercard number, a CVC2 code, an expiry date, and a cardholder name that matches your Payz registration. The card has a face value you specify at generation — say £50 — and that amount is reserved from your Payz balance and held against the card. Use the card at a merchant for £30, and £30 leaves your balance; £20 remains reserved against the card until it expires or you cancel it.

The growth in mobile and tokenised card rails frames this product. Apple Pay and Google Pay transactions at UK casinos have grown about 47% year on year as the dominant tokenised-card channels. The eco-Virtualcard predates that growth and serves a slightly different need — you generate the card number directly, copy it into a merchant’s checkout, and the transaction looks identical to any other Mastercard payment. It is not tokenised in the Apple Pay sense; it is a real, ephemeral card number tied to a specific value.

The reason the eco-Virtualcard exists is to expand merchant acceptance. Many merchants accept Mastercard but do not accept Payz directly, particularly outside the regulated gambling sector. The eco-Virtualcard turns a Payz balance into spending power at any Mastercard-accepting checkout. At UK casinos, however, the card’s utility is narrower than it first appears, and the reason is regulatory.

The Prepaid Versus Credit Distinction the UKGC Cares About

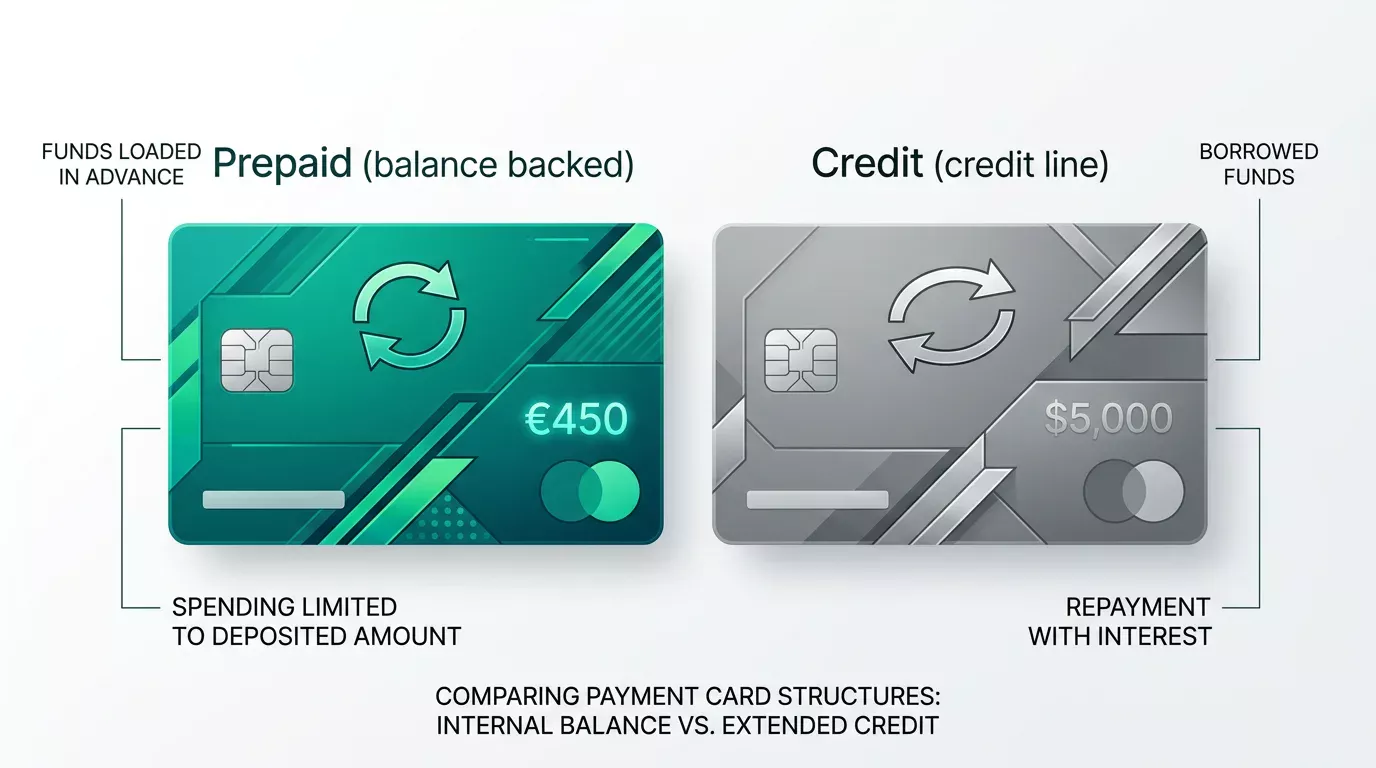

The 2020 UK credit card gambling ban prohibits operators from accepting credit card payments for gambling. The ban applies to credit cards specifically — Mastercard or Visa credit cards drawn against a credit line — and not to debit or prepaid cards. The eco-Virtualcard is a prepaid card, drawn against funds you already hold in your Payz wallet, so on its face the ban does not apply.

Before the ban took effect, 5.7% of all UK online gambling deposits were made by credit card, and 22% of those credit card gamblers were classified as problem gamblers — significantly higher than the population average. That data shaped the regulatory thinking and continues to inform how UK operators handle anything that looks even adjacent to a credit card. The eco-Virtualcard’s prepaid status protects it from the ban, but operators are still cautious about cards that route to e-wallet wrappers, because the wrapper itself could be funded from a credit source.

This is where the chain of funding matters. If your Payz wallet is funded by debit card or bank transfer, the eco-Virtualcard generated from that balance is unambiguously prepaid and the ban does not apply. If your Payz wallet has at any point been funded by credit card — even in part — the regulatory picture becomes greyer. PSI-Pay’s policies and the operator’s policies both apply, and the answer to “can I use this eco-Virtualcard at a UK casino” is not a uniform yes.

My practical guidance. Do not fund your Payz wallet from a credit card if you intend to use the wallet at UK casinos, whether via direct Payz deposits or via eco-Virtualcard generation. The regulatory and operator-side ambiguity is not worth the convenience. Use debit card or bank transfer to fund the wallet, and the eco-Virtualcard is then a clean prepaid product. The full picture on credit card funding sits in my walk-through of ecoPayz after the UK credit card gambling ban.

Using the Eco-Virtualcard at the Casino Cashier

Once you have a clean eco-Virtualcard generated from a debit- or bank-funded Payz balance, the cashier flow is identical to using any Mastercard. Select “credit/debit card” at the casino cashier, enter the 16-digit number, CVC2, expiry, and the cardholder name. The operator’s cashier processes the card as a Mastercard transaction.

What changes is the merchant descriptor seen by your wallet. The transaction posts to your Payz wallet as a card purchase rather than a wallet transfer, and the merchant descriptor is the casino’s name as it appears on Mastercard transactions. The casino’s own systems see a Mastercard transaction with the eco-Virtualcard’s BIN; some operators recognise the BIN as belonging to a prepaid card programme and adjust their risk handling accordingly.

One operational note. Casinos that do accept Payz directly almost always prefer the direct wallet integration over the eco-Virtualcard. The direct route has lower fees, faster settlement, and cleaner refund handling. If the operator lists Payz in its cashier, use Payz directly; the eco-Virtualcard is the fallback for merchants where Payz is not on the menu.

Two transactional gotchas. First, the eco-Virtualcard cannot be used for an authorisation hold that exceeds its face value — the operator’s risk hold of £100 against a £50 card will be declined at the moment of presentation. Generate the card with face value at or above the operator’s typical authorisation requirement. Second, refunds to an eco-Virtualcard land back in your Payz wallet but can take several business days because Mastercard’s refund cycle is slower than Payz’s internal transfer cycle. Plan for the delay if you are expecting a refund of any size.

Card Lifespan, Cancellation, and What to Do With Leftover Value

The eco-Virtualcard has a finite life. The expiry date set at generation is typically months out, but the practical life is shorter — most merchants will not accept a card within seven days of expiry due to authorisation hold mechanics, so plan to use the card well before the printed expiry.

Unused balance on an active eco-Virtualcard remains reserved against the card and is not available in your Payz wallet for other purposes. You can cancel an active card from inside the Payz wallet interface, which releases the reserved balance back to your wallet. Cancellation is immediate and irreversible; the card number cannot be reactivated, and any subsequent transactions attempted on the cancelled card will be declined.

What about leftover value of a few pence after the card has been used? That residual stays reserved until cancellation. The practical approach is to cancel the card once you have finished using it for the intended purpose and recover the full residual balance. If you forget, the card eventually expires and the residual returns to your wallet automatically, but the wait is measured in months rather than days.

One detail that catches people out. If the casino refunds a transaction made on an eco-Virtualcard that has since been cancelled, the refund still routes to your Payz wallet — the underlying account does not disappear when the card is cancelled, only the card number does. The refund posts to your wallet balance directly rather than against the cancelled card.

Privacy is a side benefit worth noting. The eco-Virtualcard hides your underlying funding source from the merchant. The casino sees a Mastercard transaction with a PSI-Pay-issued BIN; it does not see your bank account, debit card, or even directly that the funds came from a Payz wallet. The data point is not “I deposited with Payz” but “I deposited with a Mastercard issued by PSI-Pay” — a more anonymous descriptor on bank statements and less informative to the operator’s risk engine. For some players this is valuable; for others it is irrelevant. Worth knowing the option exists.

Prepared by the Paylobby editorial staff.