Latest UKGC Licensed New ecoPayz Casinos

People ask me to recommend “the best new Payz casino” most weeks, and I have stopped pretending the question makes sense. “New” is a moving target — a brand that holds a UKGC operating licence dated three months ago looks fresh, but the operating company behind it may have been running gambling sites for a decade under different skins. What you actually want to know about a new brand is what its licence covers, whether Payz appears as a day-one payment option, and how to tell genuine new entrants from white-label refreshes with the same back-office.

The UK regulated market is large enough that a steady trickle of new licences each year is normal — gross gambling yield reached £16.8 billion in the year to March 2025, up 7.3% on the previous twelve months. Where there is revenue, there are new entrants. The mistake is assuming “new” automatically means “better”; in payments terms, it often means “still working out which wallet rails to integrate”. Let me walk through how to read this.

Current Regulatory Shifts and Industry Compliance Trends

The forecast picture for the UK online gambling sector projects a compound annual growth rate of 12.8% between 2025 and 2030. That is the macro reason new brands keep appearing despite the well-publicised regulatory tightening — the underlying demand is still rising, and operators see room for differentiation. The micro picture is more complex.

What I see in the UKGC register week to week is a mix of three patterns. The first is a genuine new operating company — fresh corporate structure, fresh leadership, fresh tech stack — applying for a Remote Casino licence after a long pre-application review. These are rare and slow, often taking 18 to 24 months from incorporation to live cashier. The second is an existing licensed operator launching a new consumer brand under its established licence — same compliance team, same payment partners, same back-office, but a new front-end and a new promotional cycle. This is the most common pattern and the source of most “new in 2026” listings. The third is a brand transfer or change of control, where an existing operator buys a smaller licence-holder and rebrands; from a player perspective it looks new, but the engine underneath is older than it appears.

The competitive dynamic matters because the regulated sector is under pressure from rising taxes and tighter operating rules. As Grainne Hurst, the CEO of the Betting and Gaming Council, put the policy question to industry observers in May 2026: “The choice for policymakers is clear. If the regulated sector becomes harder to use or less competitive, customers will not stop betting, they will simply go elsewhere.” New brands respond to that pressure by trying to look different — more wallet options, faster payouts, lighter friction at sign-up. Payz availability is one of the early decisions a new operator faces.

What Counts as “New” for a UK Player

If you are trying to evaluate a brand, the dates that matter are not always the dates the marketing page advertises. Three timestamps tell you what you actually want to know.

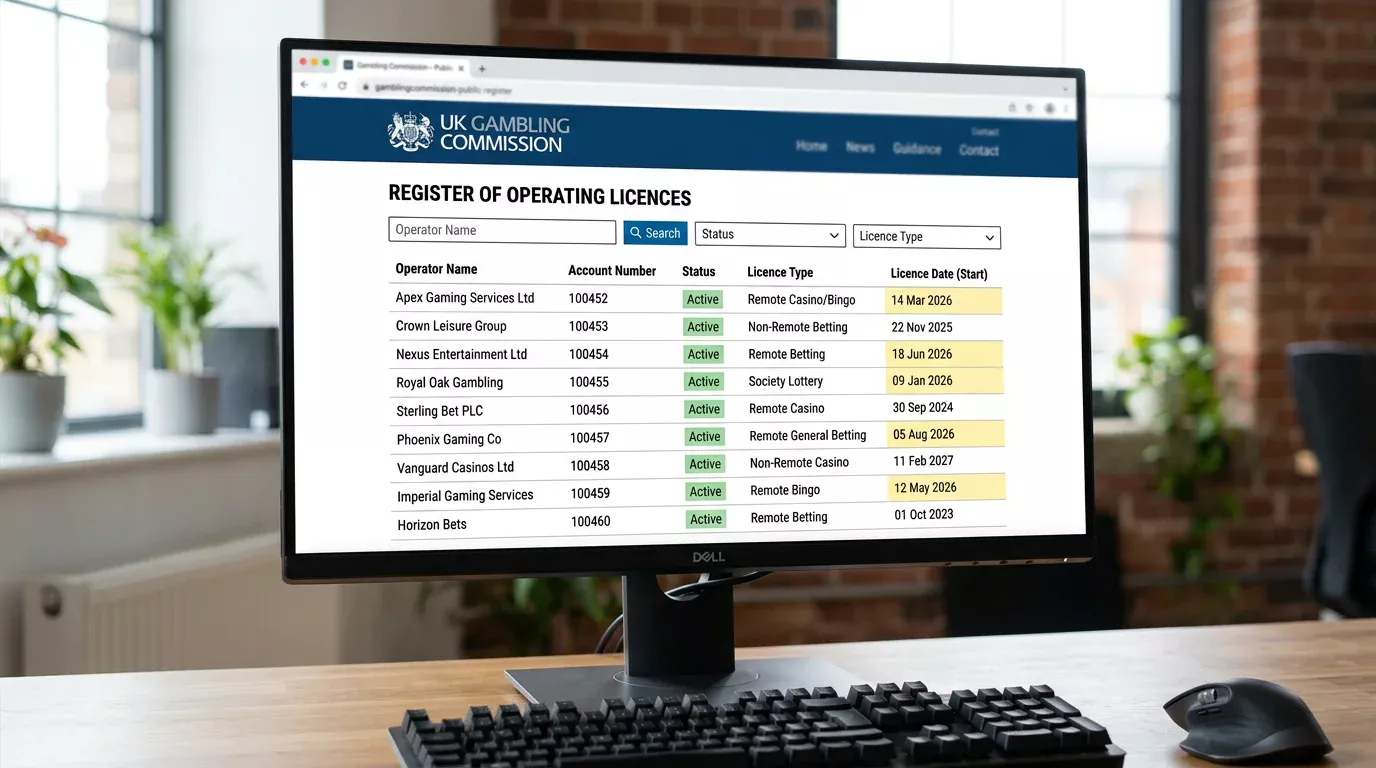

The first is the UKGC operating licence date, which you can verify on the Commission’s public register. A licence granted in 2025 or 2026 means the operating entity recently completed the Commission’s fit-and-proper checks. The second is the brand’s first transaction date, which is usually within a few weeks or months of the licence going live but can lag if the operator is still finalising payment integrations. The third is the date Payz was added to the cashier menu, which is the one that affects you most directly and is the one operators rarely publish.

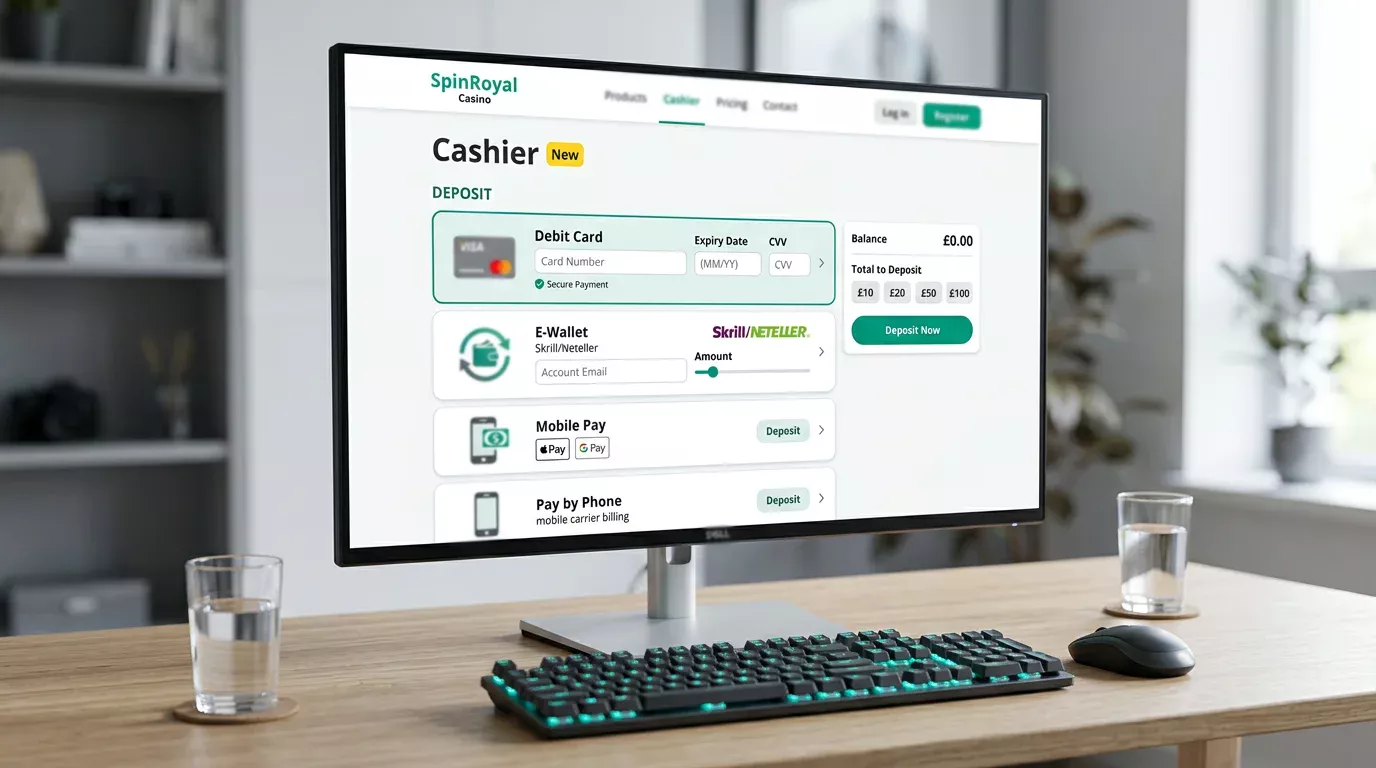

The gap between licence date and Payz integration is typically two to six months. Operators tend to launch with debit card and one or two e-wallets, then expand as cashier traffic justifies the integration cost. A newly licensed brand that lists Payz on day one usually does so because its back-office is shared with another operator already running Payz, not because it has independently negotiated the rail.

Why Some New Brands Carry Payz From Day One

The new operators that ship with Payz available on launch night fall into a specific category: subsidiaries of existing platforms or white-label clients of established B2B providers. The Payz integration in those cases is inherited, not built. From a payments-analyst perspective that is a positive signal — the cashier code has been tested at scale on sister sites, and the operational kinks of pending withdrawals, dormant tier upgrades, and currency conversion fees have been worked through elsewhere.

The newer pattern, which I have been watching since late 2025, is the operator launching with mobile-first wallets — Apple Pay and Google Pay — and treating Payz as a phase-two addition. This is partly because mobile rails are cheaper to integrate and partly because the demographic the brand is targeting may not include traditional Payz users. If you fund through Payz and a new brand only lists card rails, give it three to six months before assuming it will never add the wallet. For practical mobile-side advice, my guide to using the Payz app at UK operators covers the cashier behaviour on iOS and Android.

The third subset is the operator that explicitly markets Payz as a differentiator. These brands tend to be smaller, niche-focused, and pitched at slot-heavy players who prefer not to use debit cards. They usually offer slightly higher Payz deposit caps than the market average, and occasionally include Payz in their bonus eligibility — which, as I have written elsewhere, is the exception rather than the rule across the UK market.

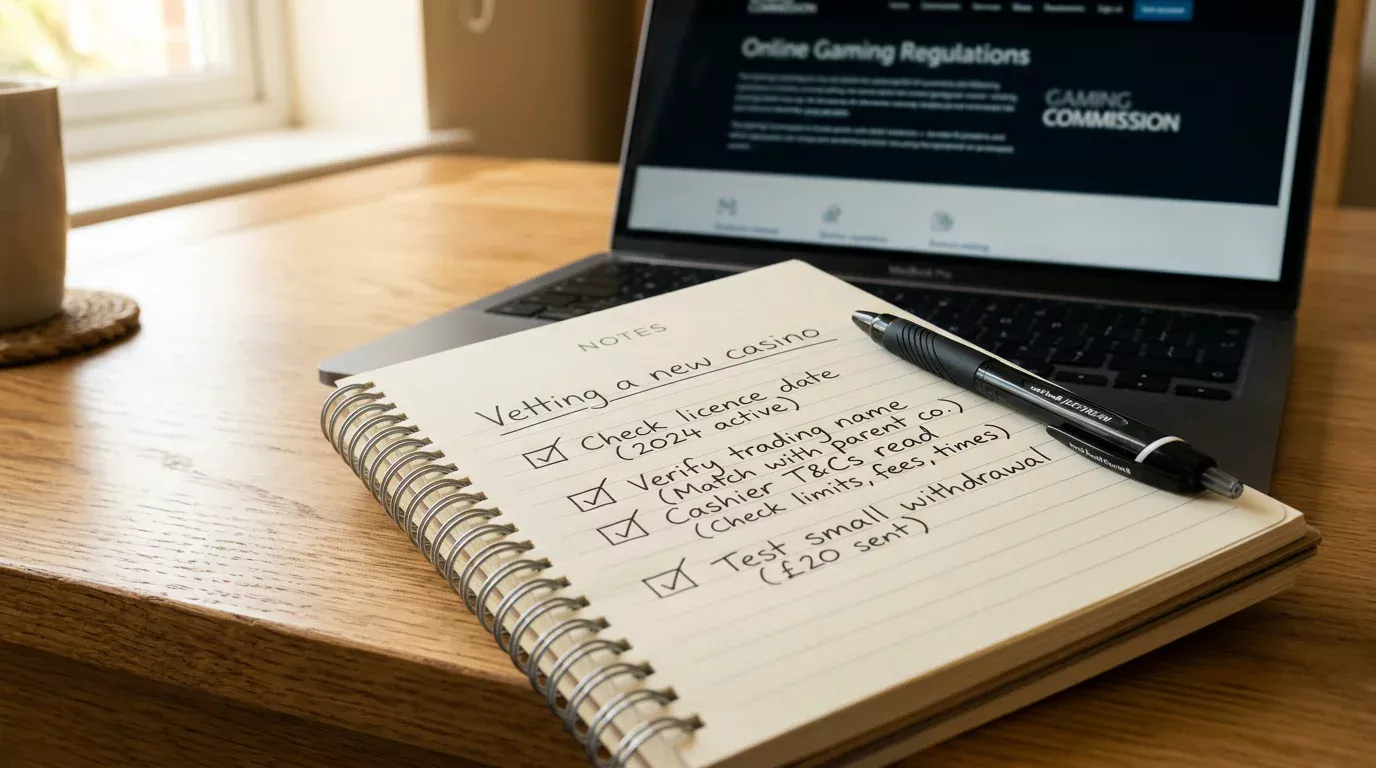

Vetting a New Brand Before You Fund It

My checklist for any new UK casino claiming to accept Payz is short and unforgiving. Skip any step and you risk a slow first withdrawal at best, an unrecoverable balance at worst.

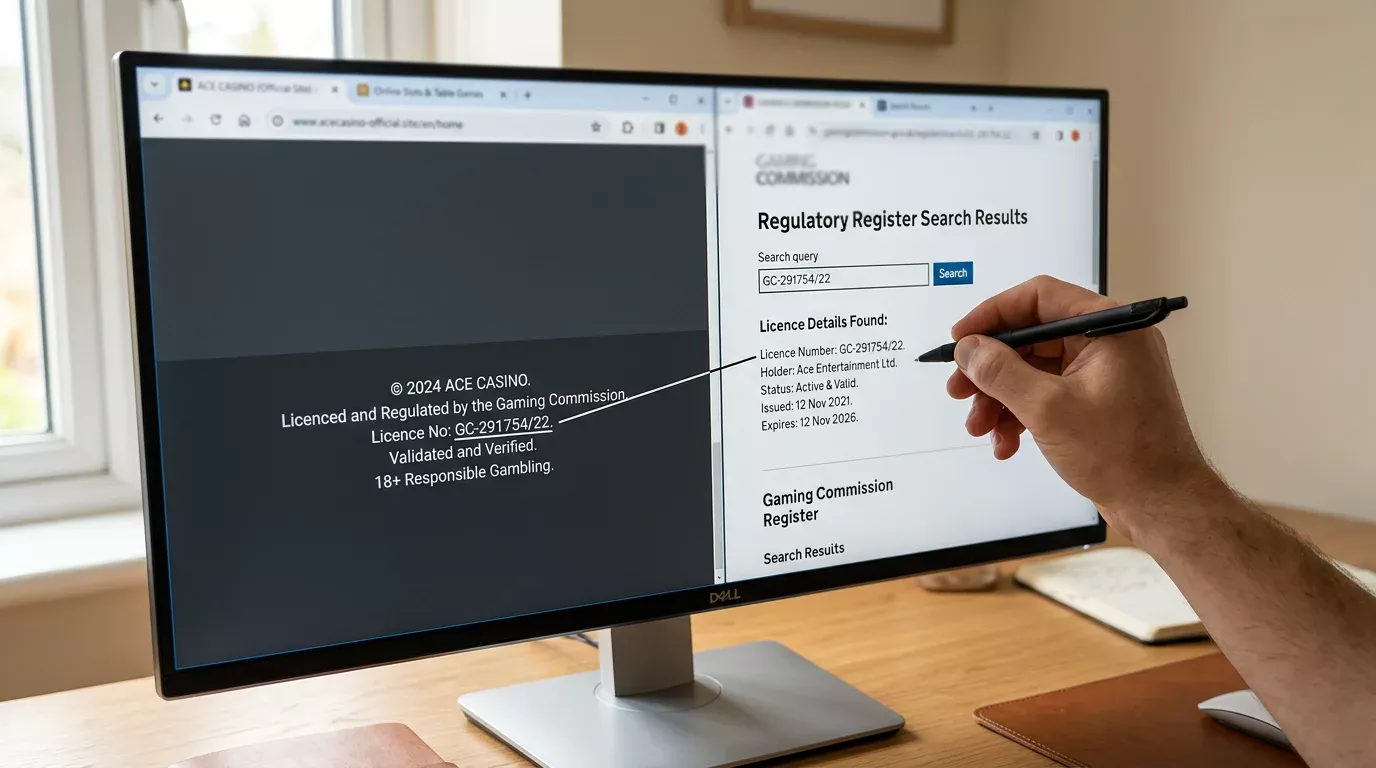

Check the UKGC licence on the Commission’s public register. The brand should appear with an account number, an operator name, and a current “Active” status. Domains that route to operators not on the register are unregulated, full stop. Verify the trading name on the cashier matches the licensee on the register; some operators run multiple brands, and a mismatch is a sign of either careless drafting or a more serious problem.

Read the cashier T&Cs for Payz-specific clauses before you deposit. New brands sometimes carry over withdrawal limits or fee schedules from a sister site without updating them, which can create surprises at first payout. Check the responsible-gambling page for the standard tools — deposit limits, time limits, GAMSTOP integration, self-exclusion options. Their presence is a UKGC condition; their depth varies, and a shallow implementation is usually a sign of a hurried launch rather than malicious intent.

One discipline I would urge: do not chase the welcome bonus on a brand-new operator. The bonus T&Cs are where new brands cut corners most often, and a clause that looks ambiguous on day one may be enforced harshly on day thirty. Make a small qualifying deposit by Payz, play a modest session, request a small withdrawal, and observe how the cashier handles it before you commit a larger bankroll. The first withdrawal is the only honest test of an operator’s payments operations.

A final note on the broader risk picture. The growth of new UK-licensed brands is happening alongside the growth of unregulated offshore operators that often borrow legitimate-sounding names and copy UKGC-style trust signals. If you arrive at a new “Payz casino” via a search ad or social media link, the burden of proof is on the operator. Cross-check the licence yourself; do not rely on a badge on the website. The badges are easy to fake. The register is not.

Prepared by the Paylobby editorial staff.