Fast ecoPayz Casino KYC Audits and Required Documents

Identity verification gets a bad rap in UK gambling circles, mostly because players encounter it at the worst possible moment — usually when a withdrawal is sitting paused and the operator is asking for documents the player thought they had already supplied. Reframed as a one-off setup task done at registration, the same process is twenty minutes of admin that saves you a week of friction later. The work is identical; the timing transforms the experience.

UK operators are required to verify identity, age, and address before allowing material gambling activity, with affordability checks layered on top at higher thresholds. Payz, as an FCA-supervised e-money service operating through PSI-Pay Ltd, runs its own parallel verification at the wallet level. Two verification chains, two sets of documents, two timelines that have to align before a payout actually flows. Knowing what each one wants and when avoids the most common cause of payment friction in this market.

Keep in mind that reaching the £150 vulnerability check threshold will automatically trigger additional affordability reviews by the operator.

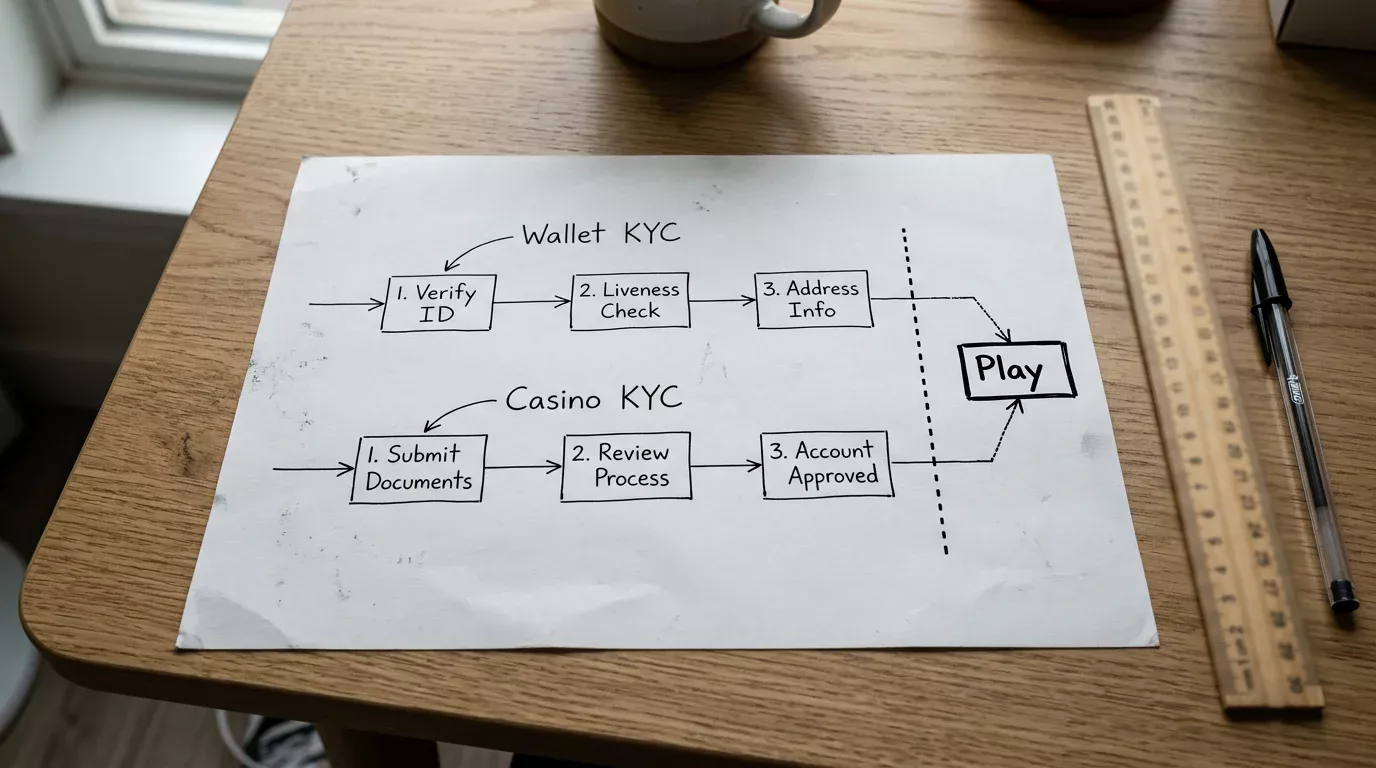

The Dual-Track Identity Verification Framework

Picture verification as two checkpoints on the same road. The wallet wants to confirm you are who you say you are before letting you fund the account and move money around. The casino wants to confirm the same thing before letting you gamble and, more strictly, before letting you withdraw. The two checkpoints do not share documents. You complete each independently, with your own paperwork, on your own timeline.

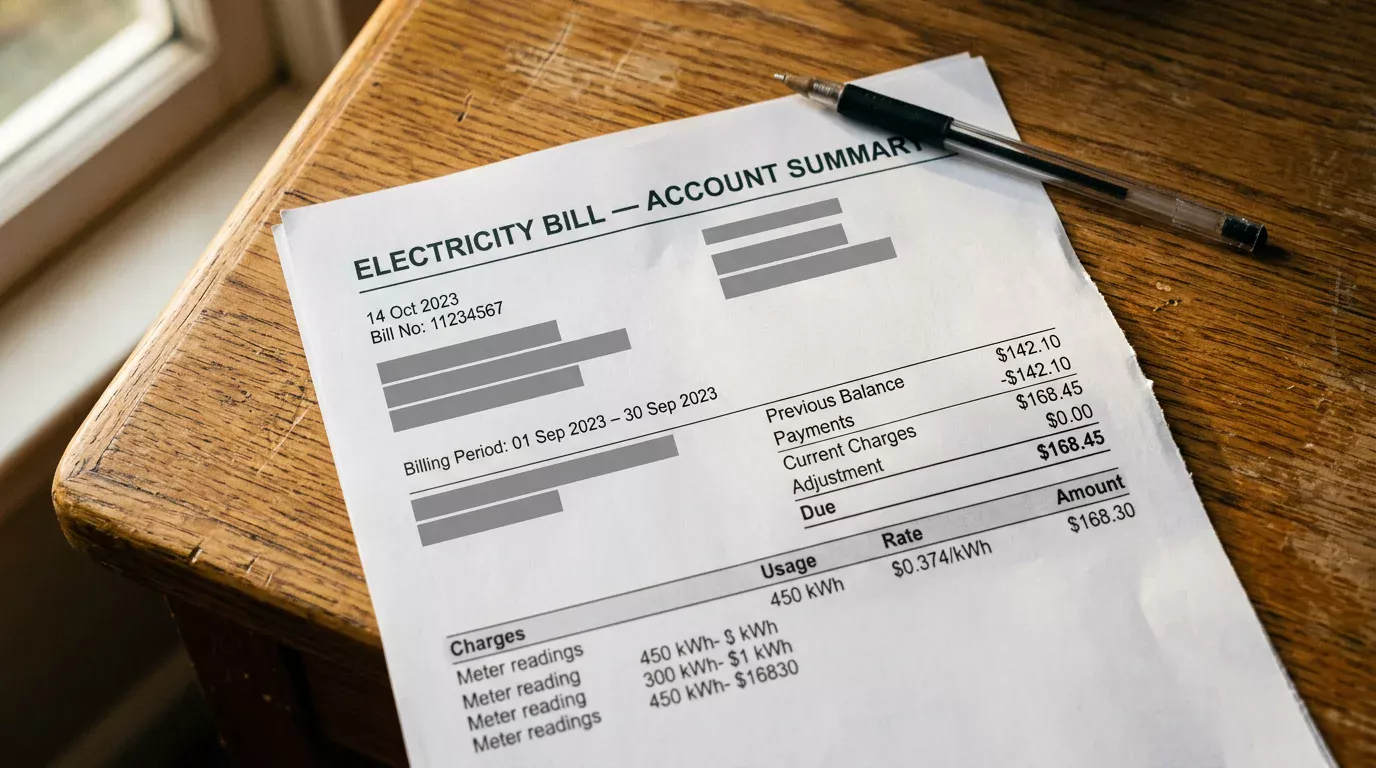

Track one is the Payz wallet itself. The standard ask is identity (passport, driving licence, or national ID), address (utility bill, bank statement, or council tax bill from the last three months), and sometimes a selfie or live-capture liveness check. The verification unlocks higher tiers — moving you from Classic up through Silver, Gold, Platinum, and VIP — each with progressively higher transaction limits and lower fees. PSI-Pay’s authorisation covers operations in 174 countries, and the wallet’s verification standards reflect that international compliance footprint rather than purely UK requirements.

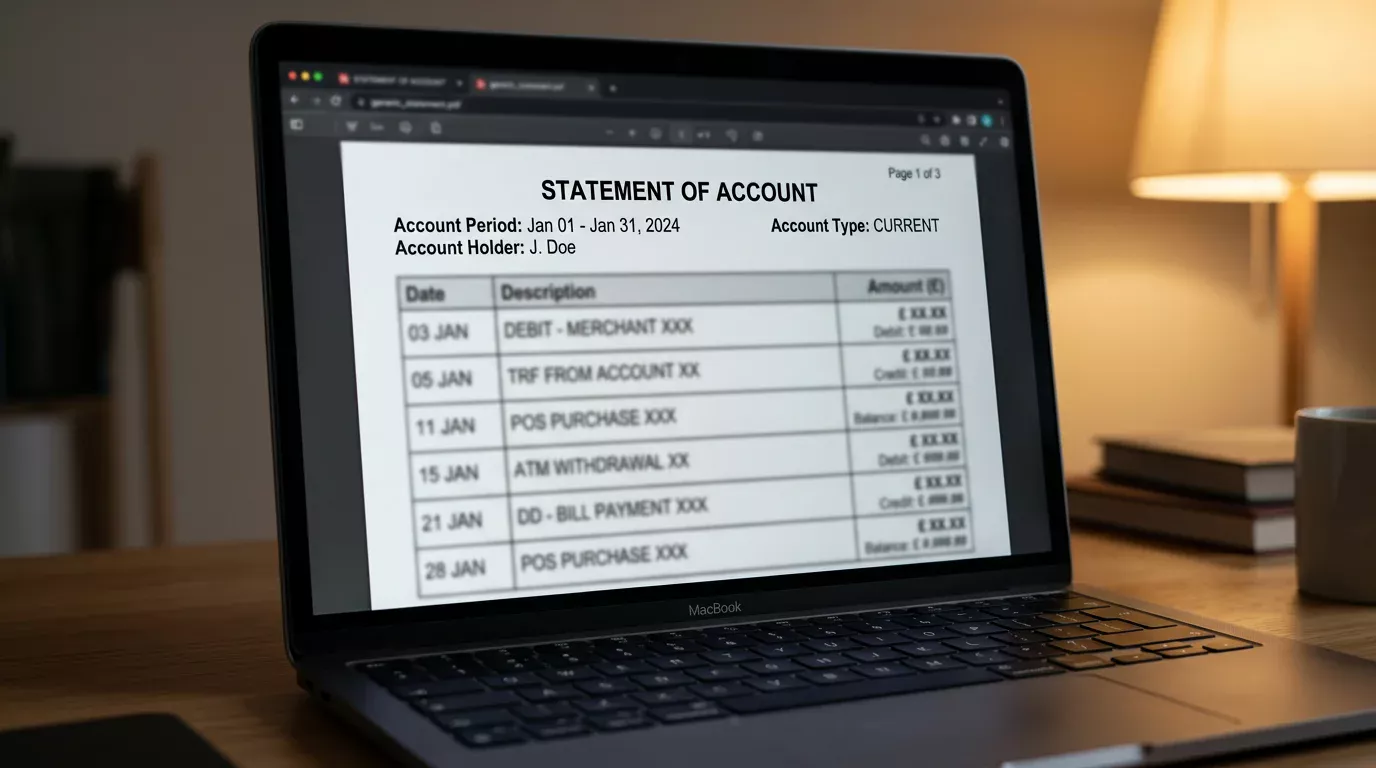

Track two is the casino. The same ID, the same proof of address, often a recent bank statement or card statement to confirm funding source. UK operators have moved heavily toward automated verification — 97% of affordability checks now run frictionlessly through open banking and credit-reference data — but the documentary side of identity verification is still primarily document-based. Some operators verify at registration, some at first deposit, some at the threshold where regulated affordability rules kick in. The pattern varies; the eventual ask does not.

The Documents That Work and the Documents That Do Not

Reader emails about rejected documents follow a small set of themes. The passport scan was readable but the corners were cropped — rejected because the machine-readable strip at the bottom was incomplete. The driving licence photo was clear but the back was missing — rejected because the address has to match the front in some cases and operators want both sides. The utility bill was eight weeks old — rejected because most operators require the last three months and “recent” gets interpreted strictly. The bank statement was a redacted PDF — rejected because the redactions sometimes cover the very fields the verification team needs to see.

The pattern is consistent. Verification teams want documents that are unambiguous, current, and complete. Cropping anything off the page makes the document worse, not better. Privacy redactions undermine the document’s purpose. Phone screenshots of physical documents are usually fine if the lighting is reasonable and the document is flat; angled shots with shadow across half the page typically fail. The standard that works: lay the document flat on a plain surface, photograph it under even light with all four corners and any reverse side included, save as JPG or PDF, upload at full resolution.

For digital documents — online bank statements, e-bills — download the original PDF from the issuer rather than screenshotting it. The metadata in the original PDF is part of what verification teams use to confirm it has not been altered. Screenshots strip that metadata and often trigger rejection even when the visible content is correct.

Source-Of-Funds Requests

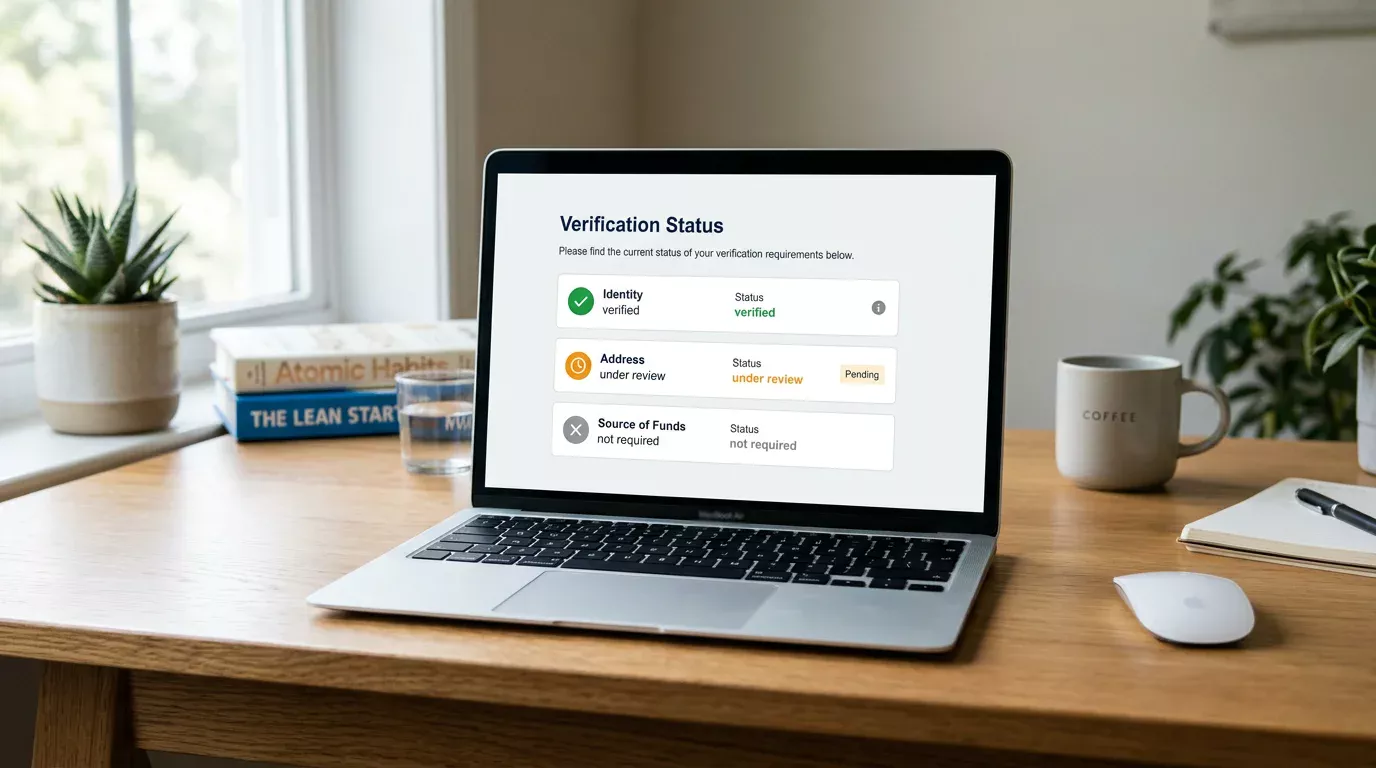

The most uncomfortable verification step for many players is source-of-funds documentation, which sits above basic identity verification and applies at higher activity thresholds. The operator is required to be satisfied that the funds being gambled have a legitimate origin. The trigger thresholds vary by operator and risk model, but cumulative activity in the low thousands of pounds will increasingly produce a request.

The documents that satisfy source of funds are pay stubs, employer letters, recent tax returns, business accounts, or evidence of legitimate windfall (inheritance documentation, property sale completion, redundancy payment, gift declaration with a clear paper trail). The frame to use mentally is “if a bank’s compliance officer were reviewing this account, what would convince them?” The same documents largely apply.

The deeper structural context matters here. The UK gambling market has been moving toward more proactive affordability checks at lower thresholds since the 2023 white paper, with the financial vulnerability threshold dropping to £150 from 28 February 2025 — meaning operators now run vulnerability checks at far lower amounts than the source-of-funds documentary threshold. For more on that specific change and what it means in practice, I have written about the £150 vulnerability check and how it changes routine play. The two are related but distinct: vulnerability checks are largely frictionless and algorithmic; source-of-funds requests are documentary and human-reviewed.

The Verification Timeline You Can Actually Expect

A complete document set, uploaded at registration to a major UK operator, typically clears within 24 hours for identity and address verification. Source-of-funds requests, when triggered, run on a slower timeline — often two to five working days because they involve human review. The wallet verification at Payz runs broadly on the same schedule, with tier upgrades taking 24 to 72 hours on average from document submission.

The variable is whether documents are complete and unambiguous on first submission. Rejected documents reset the clock. I have seen players cycle through three rounds of rejected uploads over a fortnight when one well-prepared submission would have cleared everything in a day. Each rejection feels arbitrary in isolation; the pattern across them is usually that the original documents were marginal and any single reviewer’s threshold was the deciding factor.

Pre-emptive verification — completing both wallet and casino verification at registration before any meaningful gambling activity — converts the entire timeline from a withdrawal-blocking inconvenience into a registration-day chore. The 24 to 72 hour window happens, but it happens at a moment when nothing depends on its outcome. By the time you actually want to withdraw, the verification is closed and the payout flows on its own clock.

When Verification Stalls

Stalled verifications are usually one of three things. The operator’s team has not yet picked up the submission — particularly common on weekends or holiday periods when staffing is reduced. The submission was insufficient in some way and a rejection or further-information notice has been issued that landed in account notifications rather than your inbox. Or the case has been escalated to enhanced due diligence, which the operator may or may not flag visibly while it is in progress.

The first two are resolved by checking your account notifications and resubmitting. The third is more delicate — enhanced due diligence cases can take longer, and pushing for status updates rarely accelerates them. The right move is to confirm receipt of all documents, ask whether anything else is needed, and then wait. The UK gambling market processed activity for 24.4 million active accounts in the year to March 2025, and verification queues at scale are simply not as fast as customer-service messaging tries to suggest.

The Privacy and Data Side

One question I get often is what happens to the documents after verification. UK operators are required to retain verification documents under anti-money-laundering rules for at least five years after the customer relationship ends. Payz retains documents under its own AML obligations on broadly similar timelines. The documents sit in compliance archives, not in customer-service queues. They are not, in any operator I know, shared with marketing systems or visible to general support staff.

What changes if you close an account is that you lose access to the documents but the operator retains its copies. If you re-register later with the same operator, you may need to re-submit documents because retrieval from compliance archives is not usually wired into the account-creation flow. Plan around this — keep your own copies of what you upload, in a folder with a sensible naming scheme, and you can re-submit later in five minutes rather than reassembling everything from scratch.

The Pragmatic Summary

Verification is the single largest source of friction in UK casino-Payz flows and the single most controllable variable for the player. Operators verify because they must; players resist because verification arrives at the worst moment. The fix is timing, not avoidance.

For more insights on navigating compliance and payment rules, return to the main hub at Paylobby.

Treat verification as the first task on the first day of using any wallet-and-casino combination. Submit complete, high-resolution, original-format documents. Verify both the wallet and the casino on the same day if possible. Keep a personal copy of everything you upload. Expect 24 to 72 hours for routine clearance and longer for source-of-funds requests if they arise. Done this way, verification becomes a one-time cost paid before any money is at stake, rather than a recurring blocker that ambushes withdrawals. I have seen the difference between players who verify early and players who verify reactively measured in weeks of cumulative delay across a year. The work is identical either way; the schedule decides whether it costs you anything.

Created by the "Paylobby" editorial team.