Micro Stakes: ecoPayz £5 Deposit Casinos for UK Players

The £5 minimum deposit feels like the natural floor for casual UK casino play, but it is far less common via Payz than via debit cards. I spend a fair share of my time explaining to readers why their favourite operator accepts £5 on Visa but enforces £10 or £20 when they switch to a Payz wallet. The answer has more to do with cashier economics than with anything Payz itself does, and once you see the maths, the £5 Payz deposit looks less attractive than the marketing pages suggest.

What people actually want from a £5 deposit is short sessions on low-volatility slots without committing real money to a brand they are still testing. That intent is legitimate, and there are operators who accommodate it through Payz. Just be aware of what the £5 buys after fees, conversion, and bonus exclusions are accounted for.

Commercial Reasons behind the Rarity of the £5 Threshold

Roughly 60% of UK online casino players still prefer debit cards over any e-wallet, and that preference drives the cashier economics. When an operator publishes a £5 minimum on debit card, the per-transaction processing cost is in pence and the cashier code is mature; the operator can afford to honour the £5 floor because the marginal cost of a small deposit is negligible. Payz transactions cost more to process per pound — there are PSI-Pay fees, occasional currency conversions, and additional KYC checks that scale with transaction count rather than amount. A £5 Payz deposit, processed twenty times in a month, is more expensive than four £25 deposits for roughly the same player value.

Operators respond to that economics by setting Payz minimums at £10, £15, or £20 even when their card minimum is £5. They are not penalising Payz users; they are pushing the per-transaction value above the breakeven point where the wallet integration pays for itself. The pattern is so consistent that I treat any operator with a £5 Payz minimum as having made a deliberate choice — usually because they value the wallet diversity in their cashier mix more than they value the per-transaction margin.

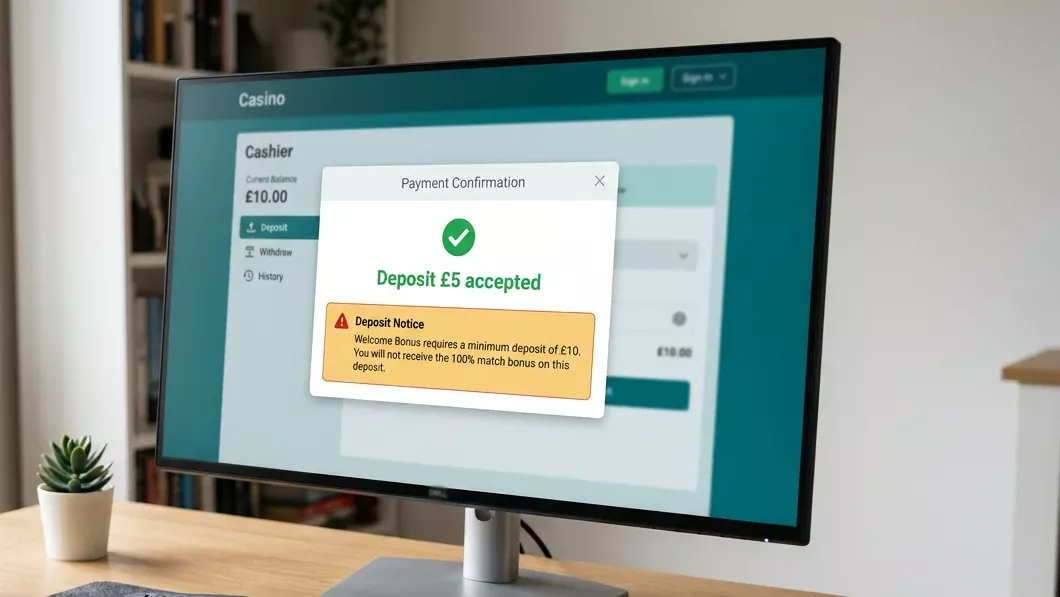

The other reason £5 Payz is rare is the bonus interaction. Many UK casinos set a minimum qualifying deposit for the welcome offer at £10 or £20, regardless of payment method. A £5 Payz deposit at such an operator buys you no bonus access, no spin pack, and no loyalty acceleration. The deposit clears, the funds land in your balance, and that is the end of the interaction. Some operators make this transparent in the cashier; others let you discover it after the fact.

The Operators That Do Accept £5 via Payz

The £5-Payz-accepting cohort tends to split into two profiles. The first is the smaller niche operator courting casual or low-stakes players — typically slot-heavy brands targeting recreational players who play a few times a month. These operators benefit from the wallet diversity in their cashier and accept the unit-economics hit on £5 deposits as a customer-acquisition cost.

The second profile is the established multi-brand group running a “casual” sub-brand alongside its main proposition. The sub-brand inherits the parent’s wallet integrations, including Payz, and sets a low minimum to differentiate from the parent. From a player perspective these brands look independent but share back-office and treasury operations with their parent, which means the £5 Payz deposit is processed on the same rails as a £500 deposit at the parent brand.

What I would caution against is treating the £5 minimum as the headline feature. Operators that lead their advertising with “£5 deposit accepted” sometimes have the lowest minimum in the market but compensate with higher transaction fees, longer withdrawal hold times, or stricter bonus exclusions. Cross-check the full cashier T&Cs before you commit, and use the smallest realistic deposit to test the cashier first. A £5 deposit is a useful diagnostic precisely because it is small enough to be expendable. Treat the first deposit as a test of the operator, not as a session bankroll.

What £5 Actually Buys After Fees

Run the maths once and the case for the £5 Payz deposit weakens. Average monthly active accounts on online slots reached 4.6 million in the quarter ending December 2025, up 5% year on year — these are players engaging regularly, not chasing a single £5 spin session. The realistic comparison is not “£5 deposit versus £20 deposit” but “what fraction of £5 is left after the operator and the wallet have taken their share”.

Let me work an example. You deposit £5 in GBP from a Payz GBP balance to a UK casino. PSI-Pay charges no deposit fee in this scenario, so £5 enters the cashier. The operator runs the deposit through its risk engine, lands the £5 in your real-money balance, and you are ready to play. If you lose the £5, the cost was £5, which is the worst-case calibration.

Now run the same deposit if your Payz balance is in EUR. The currency conversion to GBP runs at PSI-Pay’s published margin over the reference rate, typically 2.99% on a standard tier. Your £5 deposit was funded by roughly €5.90 at a recent rate, and the 2.99% margin takes about €0.18 of that. The £5 lands in the cashier intact but your wallet has paid £0.15-equivalent for the privilege. Repeated across ten £5 deposits, you have given up £1.50 to FX margin — a 3% effective tax on a session bankroll that was already small.

The other component to watch is the implicit withdrawal cost. If you win and want to extract £8 from the operator, the withdrawal fee applies regardless of deposit size. A £2 withdrawal fee on an £8 cashout is a 25% effective tax. Operators rarely scale the withdrawal fee down for small balances; the cost is a fixed component, and small balances bear it disproportionately.

A Practical Strategy for Small Payz Sessions

If your goal is short, low-stake casino sessions through Payz, the £5 deposit is the wrong unit. Two adjustments make the economics work better without inflating your real bankroll.

Adjustment one: deposit £10 to £15 instead of £5, and treat that amount as two or three sessions of play. The per-deposit overhead is the same whether the figure is £5 or £15, so spreading the cost across more spin minutes improves your effective rate. You can still walk away after a £5 loss; what you avoid is paying the overhead three times for the privilege.

Adjustment two: keep your Payz wallet in GBP if you are playing exclusively at UK casinos. Multi-currency wallets are useful when you travel or play across jurisdictions, but the FX margin on small deposits is the biggest hidden cost for casual play. A GBP-funded GBP deposit at a UK casino incurs no conversion, and the £5 reaches the cashier intact.

Adjustment three, slightly more advanced: time your sessions to align with the operator’s promotional cycle. Reload bonuses and cashback offers, when they apply to Payz, often have qualifying-deposit thresholds at £10 or £20 rather than £5. A £20 deposit that triggers a 10% cashback effectively delivers £22 of play for the same downside, where two £10 deposits would have triggered the same cashback twice. Where you find a Payz minimum genuinely set at £10, that threshold and the bonus qualifying threshold often align — for a deeper look at how operators draw that line, see my comparison of £10 minimum deposit Payz casinos in the UK.

One last note for new Payz users. Your first £5 deposit at a new operator may take longer to land than subsequent deposits, regardless of how trivial the amount looks. The first-time check runs your account against the operator’s AML and KYC processes, and a £5 deposit gets the same friction as a £500 one. Plan for it.

Prepared by the Paylobby editorial staff.