Legal Resolution: ecoPayz Casino Disputes and Cashier Issues

The most expensive misunderstanding I see in reader correspondence is the assumption that an e-wallet works like a credit card when something goes wrong. A reader emailed me last autumn convinced that he could “do a chargeback” on a £600 Payz deposit to a casino that had subsequently refused his withdrawal. He had used his debit card to top up the wallet; he assumed the chargeback rights followed the money all the way through. They did not. The wallet sat between his card and the casino, and the legal mechanics of dispute resolution stopped at the wallet’s edge in each direction.

This is not a defect of the wallet. It is a structural feature of how e-money institutions are positioned in the payments network. Understanding the difference between card-network disputes and e-wallet disputes matters because the available recourse, the timing, and the likely outcome are all different. The wallet has dispute mechanisms; they are not chargebacks, and the cases where they help and the cases where they do not look meaningfully different from card-network experience.

Regulatory Factors Ruling Out Standard Chargebacks

Chargebacks are a feature of card schemes — Visa, Mastercard, and the smaller networks. When you pay a merchant by card, the card network sits between you and the merchant, and its rulebook governs disputes between the two sides. If the merchant fails to deliver, charges incorrectly, or commits fraud, you can ask your card issuer to reverse the transaction through the network’s chargeback process, and the network adjudicates the dispute between the parties.

The Payz wallet breaks this chain. When you top up the wallet from your card, that card transaction is between you and PSI-Pay Ltd as the merchant. The card network sees a payment to PSI-Pay. PSI-Pay then sends funds to the casino on its own infrastructure, which is not a Visa or Mastercard transaction. The casino sees a payment from PSI-Pay. There are now two separate transactions, neither of which involves the card network’s relationship with the casino.

This means a chargeback on the card-to-wallet leg can succeed if PSI-Pay genuinely failed to deliver the e-money service (rare). A chargeback on the wallet-to-casino leg cannot succeed because there is no card-network involvement on that leg. The transaction was a direct wallet-to-merchant push, and pushes do not have chargeback rights in the way card pulls do.

The deeper context here is that the 2020 UK credit card gambling ban deliberately reshaped this architecture. Pre-ban, 5.7% of UK online gambling deposits were funded by credit card, and 22% of credit card gamblers were classified as problem gamblers. The ban closed that funding channel partly because credit card gambling losses entered the chargeback dispute pool inappropriately — losing players were attempting to reverse losses through dispute mechanisms designed for delivery failures. The post-ban architecture, with e-wallets as common intermediaries, removes that mechanism by design. It is a feature of the regulatory landscape, not a gap.

The Disputes Payz Actually Handles

PSI-Pay does run dispute processes, just not chargeback ones. The wallet’s dispute mechanisms handle a defined set of cases: unauthorised transactions where the wallet holder denies making the transaction (typical fraud claims); transactions where the wallet executed differently from the user’s instruction (technical error); duplicate transactions resulting from system issues; transactions where the merchant has clearly failed to provide the agreed service (uncommon at gambling merchants, more relevant for non-gambling commerce).

What Payz does not handle as a dispute: losing money at the casino and wanting it back; disagreement with the operator about bonus terms or wagering requirements; dissatisfaction with game outcomes; account closures by the operator following terms-of-service violations. These are operator-side issues, and the operator’s own complaints process is the first port of call.

The regulator’s recent enforcement activity has emphasised the boundaries of dispute resolution responsibility. In 2025-26, the UKGC issued 741 cease-and-desist notices and supported the removal of around 267,000 illegal URLs from search results out of 398,000 referred. The enforcement focus is on operator licensing and market integrity, not on adjudicating individual player-operator disputes — those go through the operator’s own complaints process and then to an Alternative Dispute Resolution provider.

The Legitimate Dispute Route

When a UK player has a legitimate dispute with a licensed operator, the route is well-defined. Step one is the operator’s internal complaints process — every UKGC-licensed operator must offer this and respond within eight weeks. Step two, if internal resolution fails, is escalation to the operator’s designated Alternative Dispute Resolution provider — the UKGC public register lists each operator’s ADR partner, and the ADR provider adjudicates the dispute independently. Step three, if the ADR outcome is unsatisfactory, can involve the Financial Ombudsman Service for the financial elements or the UKGC itself for licensing-conduct concerns.

The Payz wallet sits outside this chain for casino-related disputes. PSI-Pay’s complaints process handles wallet-related issues; the casino’s complaints process handles casino-related issues; the two operate independently. A player who lost a casino dispute and asks PSI-Pay to reverse the underlying transaction will be told politely that this is not how the wallet works.

What the wallet can do is provide documentation. PSI-Pay maintains complete records of every wallet transaction with timestamp, counterparty, and amount. If a player needs to evidence to an ADR provider exactly when funds were sent to an operator, in what amount, and from what wallet, the wallet’s transaction history export is the canonical record. This is administrative support for a dispute, not adjudication of it.

The Escalation Question and the Wider Context

For escalating against an operator where standard ADR has not delivered, the UK regulatory infrastructure provides additional routes. Grainne Hurst, CEO of the Betting and Gaming Council, framed the recent rise in market concerns about black-market alternatives with a pointed observation: “These forecasts are a wake-up call. The black market is not a distant threat, it is growing fast, becoming more visible and attracting billions of pounds in stakes from British customers.” The framing matters for dispute purposes because it captures the asymmetry — regulated operators have ADR routes, FOS access, and UKGC oversight; unregulated operators have none of those, and disputes with them have no useful resolution mechanism in the UK.

This is the crucial framing for any UK player tempted to follow operators offshore because of dispute frustration with a regulated brand. The regulated brand has imperfect dispute mechanisms; the unregulated brand has effectively no dispute mechanism. The temptation to “vote with your feet” by moving to a less restrictive operator usually moves the player into territory where their actual dispute leverage is materially worse, not better.

The Financial Ombudsman Service handles complaints about FCA-regulated entities, including PSI-Pay Ltd. For wallet-side issues that PSI-Pay has not resolved satisfactorily through internal complaints, FOS is the next step and the determinations are binding on PSI-Pay. For casino-side issues, the route is ADR and UKGC rather than FOS, because the casino is not the FCA-regulated entity in the chain.

Casino-Side Refund Policies

Operators do offer refunds in specific cases. Technical errors that resulted in incorrect deposits or stake records. Bonus credit issues where the wallet activity does not match the operator’s bonus accounting. Verifiable game malfunctions that affected outcomes (rare and well-documented, but they happen). Account closure scenarios where the operator returns the unwagered balance. These are handled within the operator’s own complaints process and do not require any wallet-side dispute action.

The refund typically returns to the source of the deposit. A Payz deposit refunded by a casino lands back in the Payz wallet, not in the underlying bank account. From there, the player can move the funds onward at the wallet’s standard withdrawal timing and any applicable fees apply normally. The refund mechanism does not preserve the original payment chain for routing purposes; it just sends funds back to the wallet that paid them.

Players who deal with declined deposits — a different but related category — should consult the specific decline-categories framework I have written about for Payz casino flows. The reasons for declined ecoPayz casino transactions in the UK are distinct from dispute scenarios and resolve through different routes.

The Realistic Player Checklist

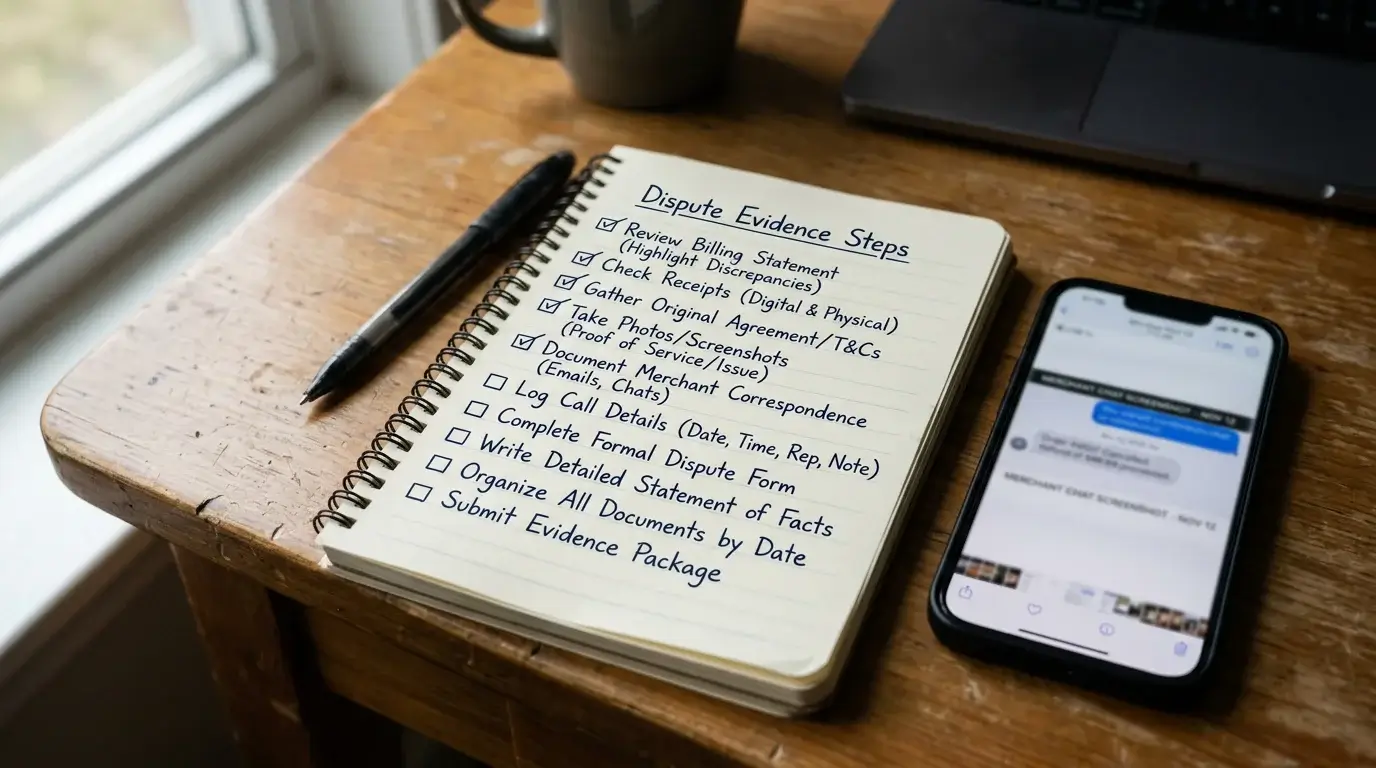

Before pursuing any dispute, several practical checks. First, document everything from the moment something goes wrong — screenshots of cashier states, copies of email exchanges with support, exports of wallet transaction history. Second, work through the operator’s complaints process formally rather than as informal support requests; some complaints processes only trigger when the player explicitly opens a complaint, and informal support tickets do not start the eight-week clock. Third, identify the operator’s ADR provider via the UKGC public register before opening the dispute, so you know where escalation goes if internal resolution fails. Fourth, do not expect speed — eight weeks for internal resolution is the regulatory maximum, and ADR can add another two to three months.

For wallet-side disputes specifically, the same approach applies to PSI-Pay’s process. Open the complaint formally, allow time, escalate to FOS if internal resolution fails. The wallet’s dispute mechanisms are real but slow, like most regulated financial dispute systems.

The Pragmatic Settled View

The wallet does not provide chargeback rights. This is a structural feature of how e-money intermediation works, not a defect of Payz specifically. Disputes with casinos go through the operator’s complaints process and the ADR system the operator is licensed to use; disputes with the wallet go through PSI-Pay’s complaints process and FOS. The two routes do not overlap, and trying to use the wrong route slows everything down without producing useful outcomes.

What the wallet provides is a documentation backbone — every transaction recorded, available for export, and usable as evidence in whichever route the player needs to pursue. That is administratively valuable. It is not legally protective in the way the chargeback expectation suggests. Internalising the difference between “the wallet keeps the records” and “the wallet adjudicates the disputes” is the single most useful framing for any reader who finds themselves needing either function.

Created by the "Paylobby" editorial team.