UKGC Regulations: ecoPayz Casino £150 Thresholds

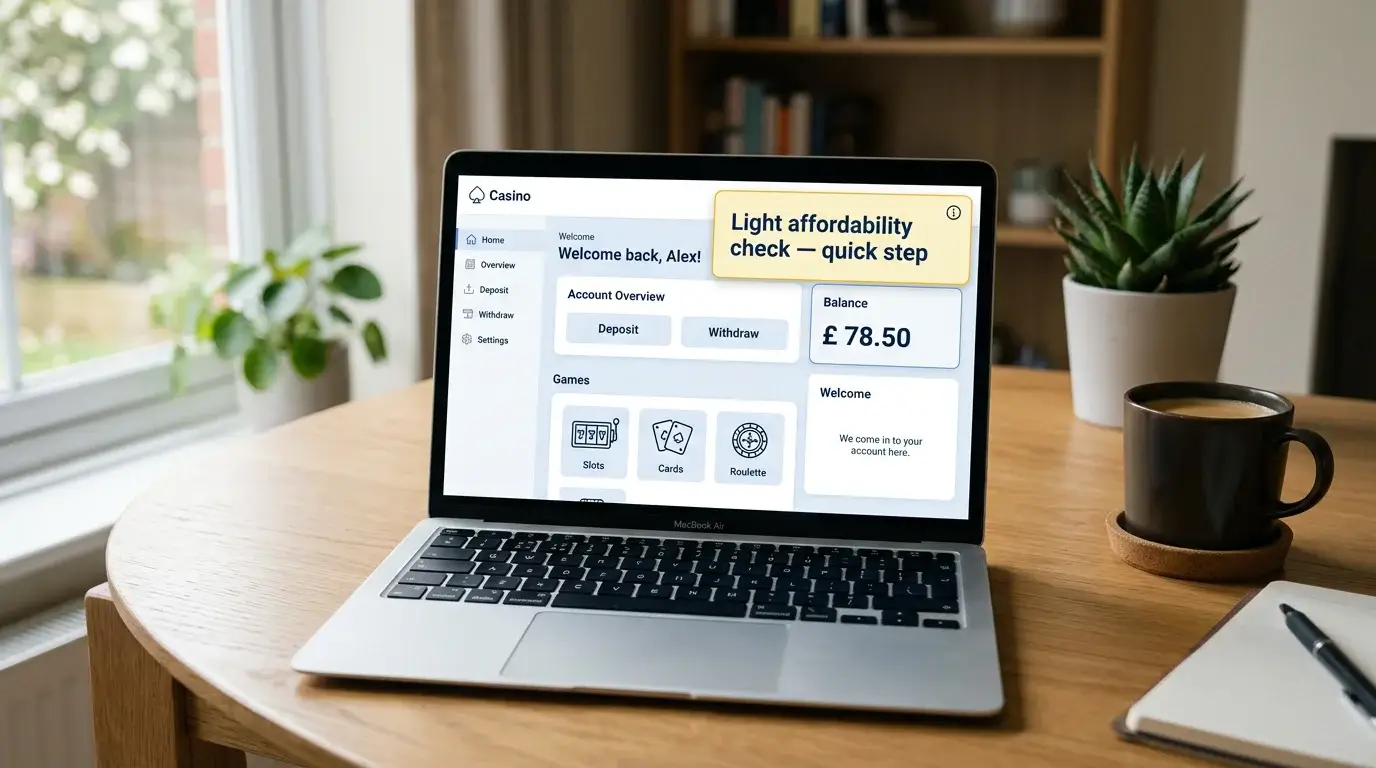

A reader sent me a screenshot in March 2025 of an unexpected prompt from his casino account, asking him to confirm a recent change of address and acknowledge a brief financial-vulnerability notice. He had not made an unusual deposit. He had not even logged in for two weeks. The prompt seemed to come from nowhere. It had not — it was the new £150 vulnerability threshold biting, and the way it surfaced was deliberately low-friction. Three months on, those prompts had become routine across every UK operator I track.

The financial vulnerability check threshold dropped from £500 to £150 over a 30-day rolling period on 28 February 2025, and the change reshaped what counts as a normal interaction between a UK player and their casino. The Payz wallet does not see any of this directly — the checks run at the operator-account level, on net deposit activity — but the wallet is the funding instrument that pushes a player across the threshold, and understanding how the check works helps explain why your casino experience changed even when nothing about your spending pattern did.

Specific System Actions Triggered by the Threshold

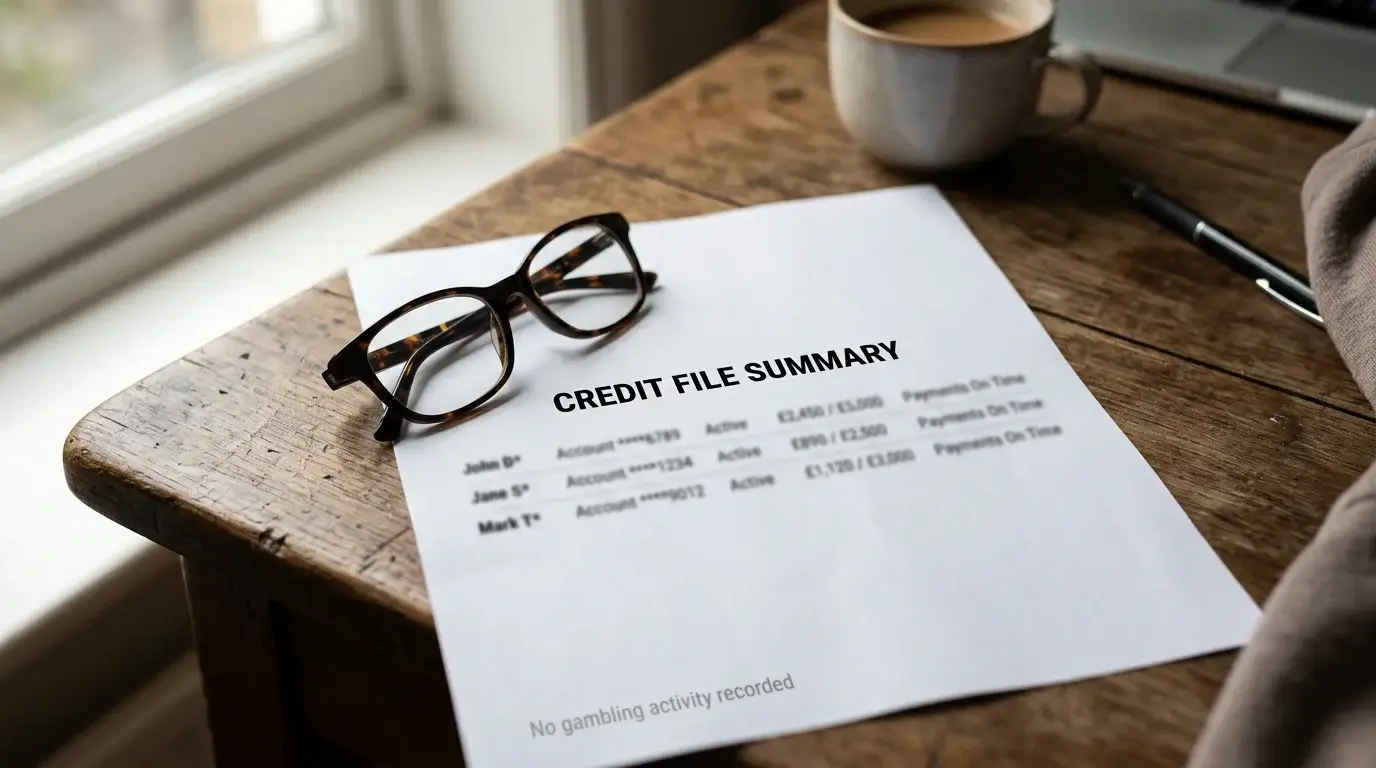

The £150 figure refers to a rolling 30-day net deposit total. Once you cross it at a single operator, that operator is required to apply a financial vulnerability screen against publicly available data — credit-reference indicators, electoral roll data, county court judgments, registered insolvencies. The screen is designed to flag accounts where there is a public record of recent financial distress, and the standard regulatory response is to apply additional friction (lower deposit limits, additional messaging, account review) rather than to block the account.

The UKGC CEO Andrew Rhodes laid out the framework in his BGC AGM speech the day before the change took effect: “Tomorrow (28 February 2025) financial vulnerability thresholds fall to £150 per 30-day rolling period and as others have mentioned today, we are still piloting Financial Risk Assessments and that pilot is well advanced.” The framing matters. The check is a screen, not an adjudication. It runs against external data, not against the player’s bank statements. The player’s primary experience should be a brief notice, not a forensic interview.

Crucially, the £150 threshold applies per operator, not across operators. If you deposit £100 at one casino and £100 at another in the same month, neither has individually crossed £150 and neither runs the check. Most active casino-Payz flows cross the threshold at a single operator quickly though, often within a single deposit. The threshold sounds high until you remember that £150 is one decent night’s session for many regular players.

The Data That Drives the Check

The vast majority of these checks run frictionlessly. The number to internalise is that 97% of financial vulnerability checks now complete using open banking and credit-reference data without the player even noticing — a figure that exceeds the original White Paper 2023 target of 80%. For routine accounts with no adverse data on file, the check fires, returns clean, and the player sees nothing or sees a brief disclosure notice they can dismiss in a click.

The 3% of cases that do not clear frictionlessly are the ones where something on the screen warrants further attention — a recent CCJ, an insolvency record, a debt-management plan flagged on the credit file, or a mismatch between the registered address on the casino account and the address on the credit file. The follow-up is usually a request for confirmation of the address or a brief documentary check, not an account freeze. The casino is required to act on the signal proportionately, and proportionate usually means “ask for clarification” rather than “lock the account”.

This is where the practical experience of UK casino play diverges between players. The 97% have noticed almost nothing. The 3% have wondered what went wrong. Both groups went through the same check; the difference is the data on file rather than the player’s recent behaviour.

How Wallet Flows Interact With the Threshold

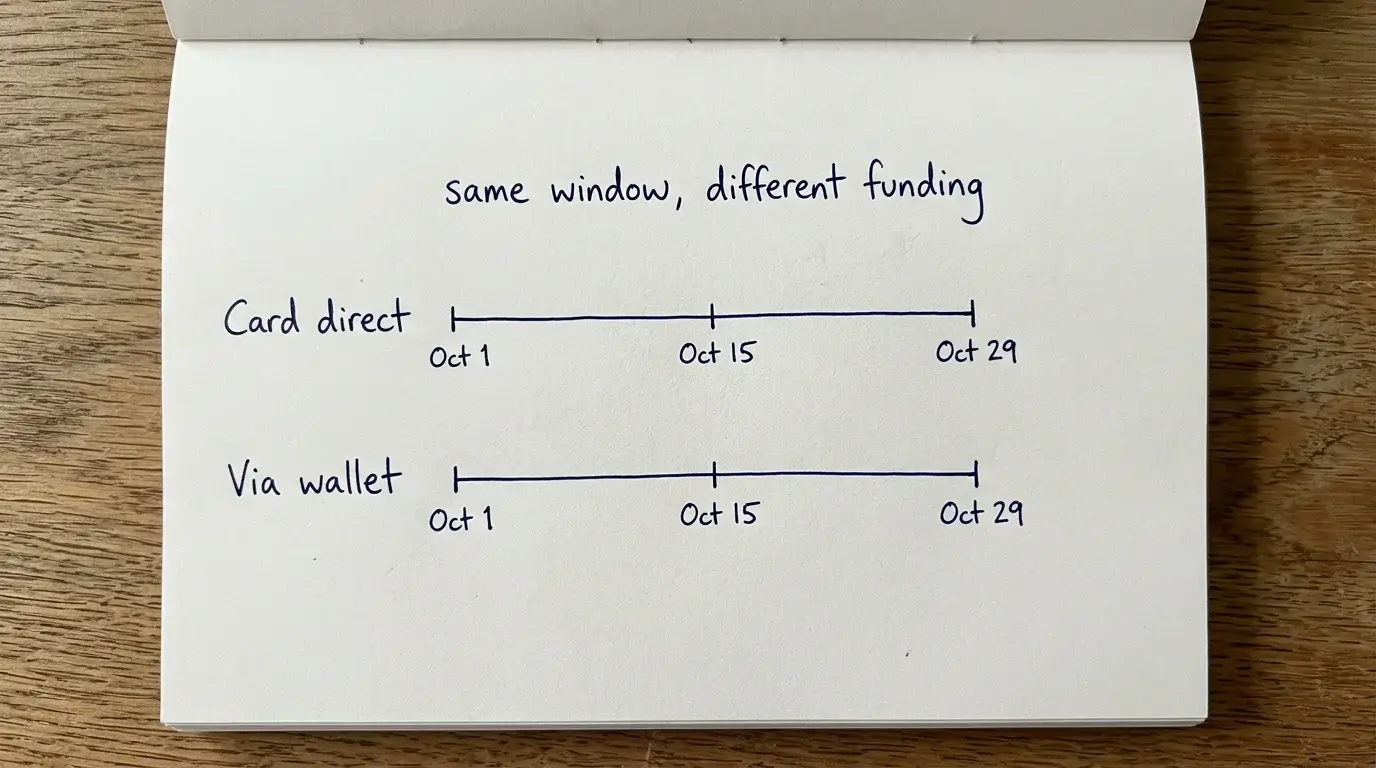

A Payz wallet does not show up directly in the financial vulnerability check. The check screens the registered account-holder against external data sources; the funding instrument is incidental. What the wallet does affect is the timing — wallet flows compress deposit activity into more frequent, smaller cycles, which means a player might cross £150 in net deposits in the first week of a month without realising they have done so.

I have seen reader emails describing accounts that “suddenly” got a verification notice mid-month. The reader has not changed anything. What has happened is that their deposit pattern, smoothed across more frequent small cycles via the wallet, has crossed the threshold earlier in the month than it would have under a card-funded pattern. Same total spend, earlier trigger.

A useful pattern to understand: under card-funded play, a player might deposit £100 in week one, do nothing for a fortnight, then deposit £200 in week three — crossing £150 in week three, triggering the check around the third week of the month. Under wallet-funded play, the same player might deposit £50 four times across the first ten days — crossing £150 in week two. The check fires earlier. The total spend across the month is unchanged. Nothing about the player’s risk profile has changed. The system is doing exactly what it is designed to do, but the earlier trigger time can feel like the operator has become “more aggressive” with checks.

The Friction-Free Flow You Should Actually See

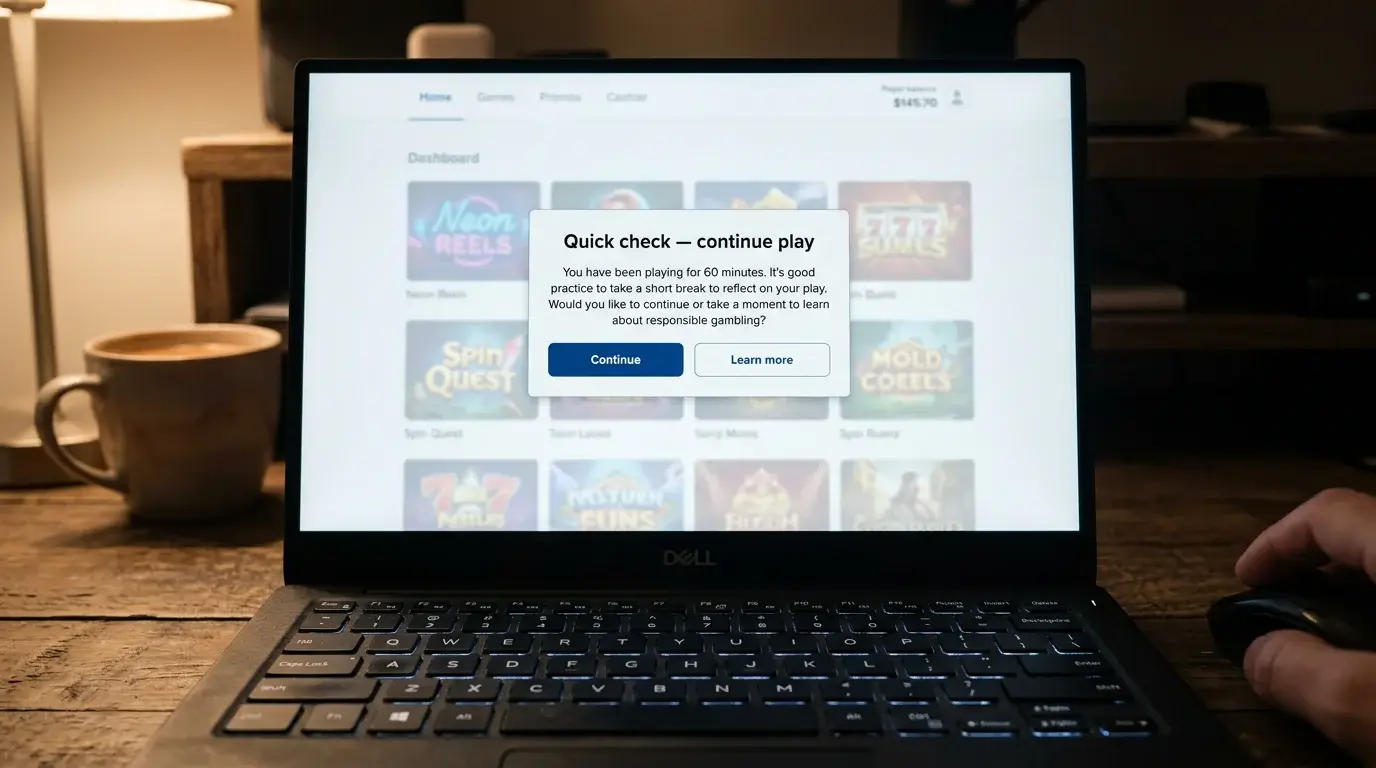

For a fully verified Payz wallet at a UK casino with the player’s identity and address on file and no adverse data on their public credit profile, the £150 vulnerability check is functionally invisible. You will see no extra screens. Deposits continue to work. Withdrawals continue to flow on their usual schedule. The check has run; it returned clean; nothing changed.

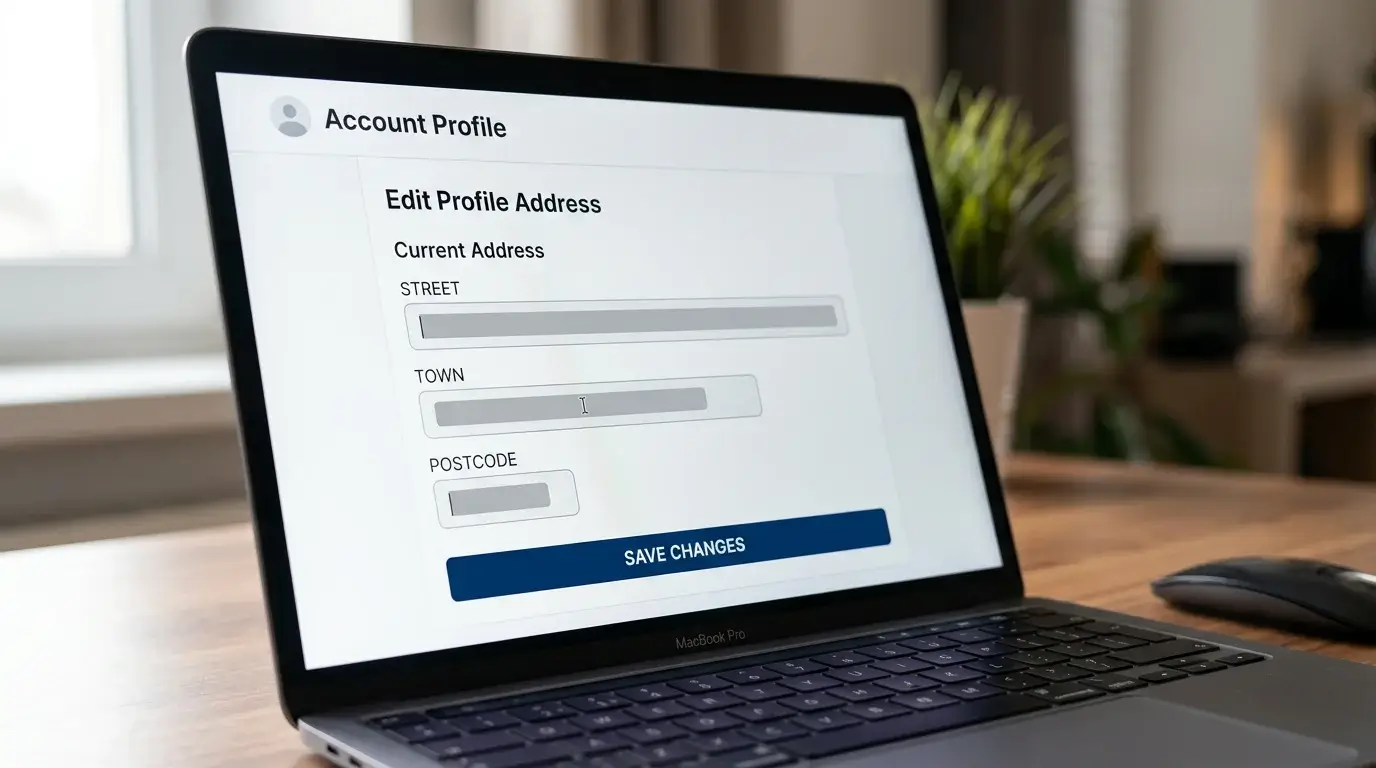

The signal that something has come up is a notice at next login asking you to confirm a piece of information (usually current address) or acknowledge a brief responsible-gambling message. Acknowledge it, confirm the data, move on. This is not a flag against your account in any meaningful sense — it is the system using the lightest available touch to confirm the screen’s reading. The 1-2 minute additional friction is the entire customer-side cost of compliance in most cases.

If the operator asks for actual documents — an updated proof of address, a recent bank statement — the check has surfaced something that needs human review. That is rarer but should be treated promptly. Detail matters here: the relevant verification flows for ecoPayz casino use are documented separately, and treating any documentary request promptly avoids the slow-burn frustration of an account that quietly stops processing larger transactions while support waits for paperwork.

What the Threshold Does Not Do

A few common misunderstandings worth clearing up. The check does not adjudicate what you “can afford” to gamble. It does not look at your salary, your savings, or your day-to-day bank activity. It is a screen against public data only. Players who hit the threshold and pass the check are not subjected to any additional discretionary review — they continue under their normal account terms.

The check does not record your gambling activity on your credit file. The data flow is one-way: the operator pulls indicators from credit-reference sources; nothing about your casino account flows back. Worrying about a “gambling mark” on your credit file from triggering a £150 vulnerability check is a common reader concern and a misconceived one.

And the check is not a precursor to source-of-funds documentation. SOF requests sit at much higher activity thresholds and follow a separate documentary process. The £150 screen and the SOF process are different mechanisms operating at different scales of activity.

The Broader Policy Direction

The threshold drop sat inside a wider regulatory package that has reshaped the UK market over 2025 and into 2026. The £5 per-spin stake limit (and £2 for 18-24 year olds) took effect over April and May 2025. The Remote Gaming Duty is rising from 21% to 40% in April 2026. The cumulative effect has been a market with more friction in places where the regulator’s harm data pointed sharpest, and broadly stable consumer experience elsewhere.

The 97% frictionless figure suggests the policy is calibrating roughly where its designers intended. A check that catches 3% for further review and runs invisibly for the rest is doing the work of risk-targeting without becoming a routine barrier to casino activity. Player advocacy groups and operator bodies will debate whether the threshold sits at the right level — some argue £150 is too low, some argue it does not bite hard enough — but the implementation has worked as a technical matter.

What This All Means for Routine Wallet Flows

The honest answer is: not very much, for most players, most of the time. The threshold exists. The check runs. The 97% never notice. The 3% see a brief follow-up that resolves with a routine confirmation step.

For Payz-funded UK casino play specifically, the practical adjustments are minor. Keep your registered address up to date on both the wallet and the casino accounts so that the screen does not flag an address mismatch as the only anomaly. Verify your identity documents proactively rather than after a trigger. Be aware that wallet flows compress deposits into earlier-month timing, so the check fires sooner in your monthly cycle than it would have under card play. None of these adjustments require any change to how much or how often you play; they just smooth the experience of the regulatory machinery doing its work in the background.

What has changed since February 2025 is not what UK players are allowed to do but the texture of the friction around moderate spend. The reader who emailed me about the unexpected address-confirmation prompt was experiencing the new normal. A year on, it is normal enough that most players have stopped noticing.

Created by the "Paylobby" editorial team.